We are always asking: When will Crypto be widely adopted?

But when real adoption happens, many people turn a blind eye.

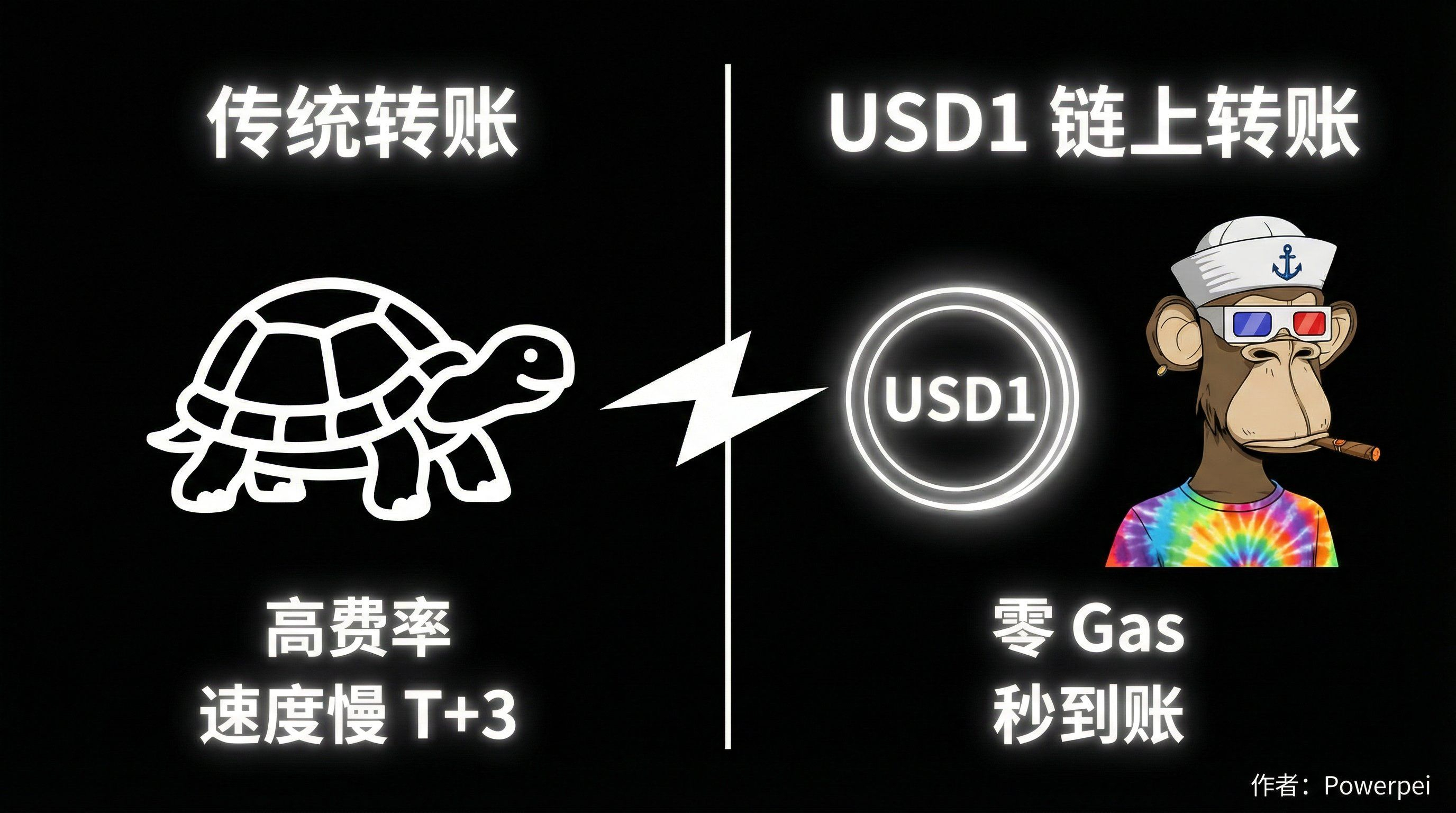

Last week, a friend who helps with Amazon e-commerce remitted money to Southeast Asia and was charged an 8% fee by the bank, which also delayed the transfer for three days. At that moment, I realized: the blood vessels of traditional finance have hardened.

That's why when you look at USD1, don't just see it as another stablecoin.

It is digitalizing the hegemony of the dollar, extending this grand proposition, combining real pain points, and pushing it to a critical point.

▰▰▰

1. Cognitive upgrade: This is not just about issuing coins; it's about building tracks.

Looking back over the past decade, stablecoins have mostly been the fuel for DeFi or a safe haven parking lot.

But USD1 is different. It was born in 2025, backed by the Trump family, making it from the start a blend of geopolitics + fintech.

The core disagreement it seeks to resolve is:

Should it continue to be a purely decentralized utopia? Or should it create a compliant + transparent + politically endorsed parallel payment system?

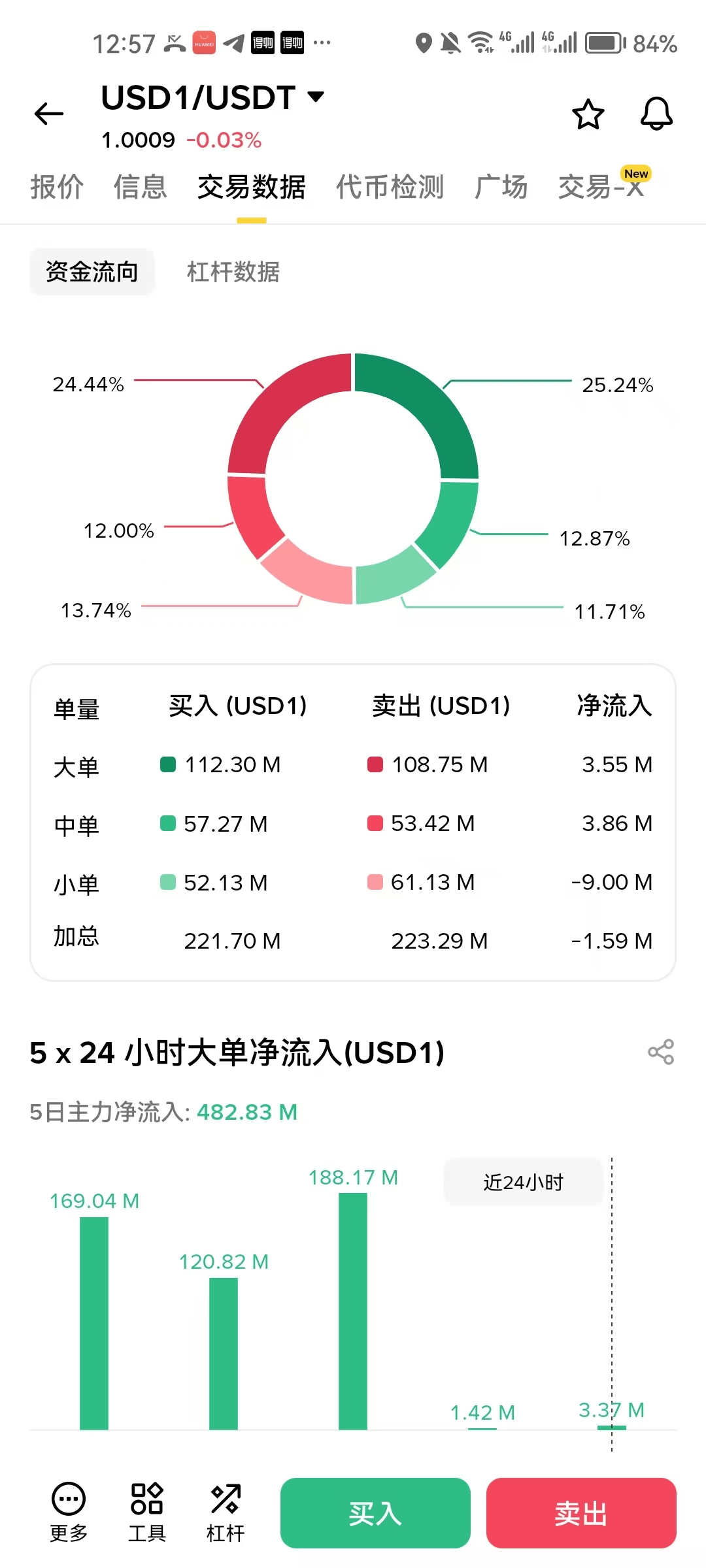

The market has already voted with its feet.

Circulation surged to 4.9 billion, entering the top five. This is not a coincidence; it's the result of narrative resonance.

When freelancers and supply chain merchants in developing countries have had enough of bank exploitation, the 'free transfer, 24/7 arrival' offered by USD1 is a dimensional strike.

Two main lines: how to revive 'dead money'?

If Polymarket proved the value of prediction markets, then USD1 is proving the 'capital efficiency' of stablecoins.

1. Payments and Real Adoption

Nearly 90% circulation on BNB Chain + zero gas fees.

This means small transfers are finally as simple as sending a WeChat red envelope. The upcoming Debit Card will bring on-chain dollars offline.

This turns 'crypto dollars' into a 'retail killer'.

2. DeFi and Institutional-level Credit

World Liberty Markets has launched.

It’s not just Yield Farming; it transforms stablecoins into programmable credit tools.

Once the banking license is issued, USD1 will become the standard asset bridging TradFi and the on-chain world.

3. Incentive Flywheel

This is the part we care about the most.

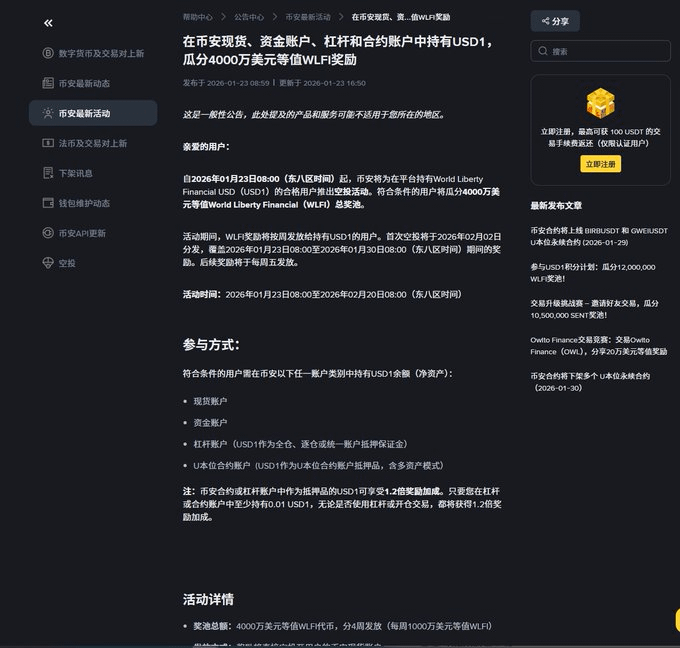

Binance's $40 million airdrop event essentially turns early adopters into ecological co-builders.

Holders of USD1 also gain governance rights (WLFI) and economic incentives, creating a positive cycle.

3. Practical checklist from Powerpei: How to benefit from this wave of dividends?

For retail investors, grand narratives are too distant; we only look at the current Alpha.

Binance × USD1 event (1.23 - 2.20), I summarized a guide to avoid pitfalls:

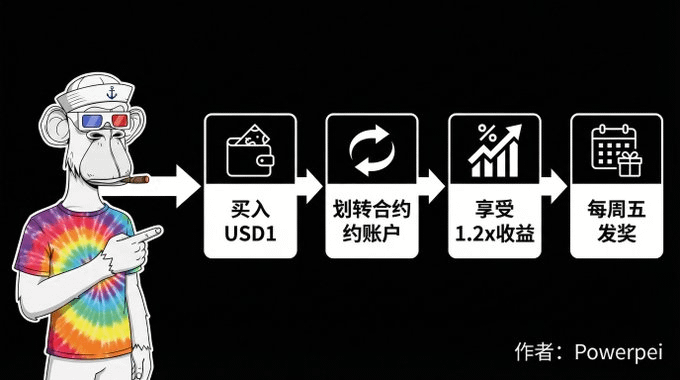

Core action: Transfer USD1 to contract/leverage accounts. Even without opening a position, you can enjoy 1.2 times the reward weight. This is the compliant backdoor left by the official.

Fatal Risk Control:

1⃣ Don't move around: The system takes a snapshot every hour, taking the lowest balance of the day. Withdrawing midway = all efforts wasted.

2⃣ Check the region: You must confirm that your KYC is not in restricted areas (I mentioned this in my previous article, and you can also check the announcement). Don't work hard for nothing in the end.

3⃣ Calculate earnings: Annualized 15%-24%. In a volatile market, this is almostrisk-free gains..

▰▰▰

Final thoughts

For crypto to move from 'casino' to 'infrastructure', stablecoins must first address the underlying needs for payment + value storage.

USD1 is realistically seizing this track.

For the industry, it reminds everyone: the real revolution often hides in the most ordinary free transfers.

For us, this might be the next cycle's opportunity, where we don't need to gamble on direction but can quietly enjoy a certainty of earnings.

Will you continue to observe memes, or will you move some of your positions to this parallel dollar track?

Let me know your choice in the comments.