If you have ever tried to trade something that is perfectly real in the physical world but annoyingly abstract in the market, you already know why tokenization is more than a buzzword. A bond is real, a warehouse invoice is real, a title deed is real, but the way those rights move is slow, fragmented, and full of manual checks. When people talk about RWAs, what they usually mean is taking that messy reality and turning it into something that can move with the speed and composability of crypto, without pretending the legal and compliance parts do not exist.

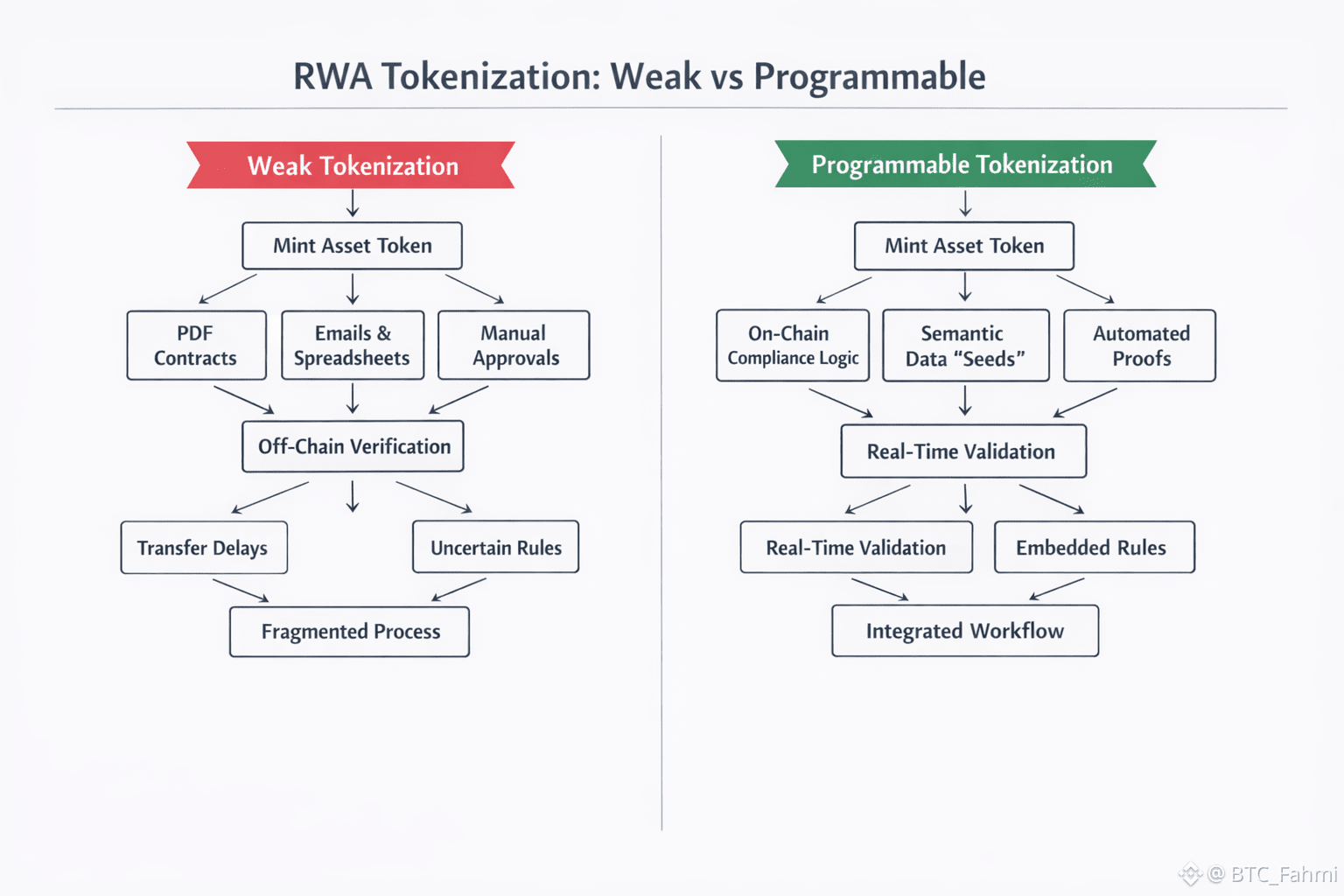

That last part is where most RWA projects quietly break. They tokenize the wrapper, but the real logic still lives off chain in PDFs, email threads, compliance spreadsheets, and human approvals. The token becomes a badge that points to the “real rules” somewhere else. Traders might tolerate that for a short while if the yield is attractive, but markets hate uncertainty. If the true transfer rules depend on a phone call or a delayed attestation, liquidity stays thin, spreads widen, and participation never becomes habitual.

Programmable RWA infrastructure is a different promise. Instead of just representing an asset, the token carries the logic that governs the asset. Not only “who owns it,” but “what can happen to it,” “under what conditions,” and “what must be proven before it moves.” In plain terms, it is the difference between a digital receipt and a digital instrument.

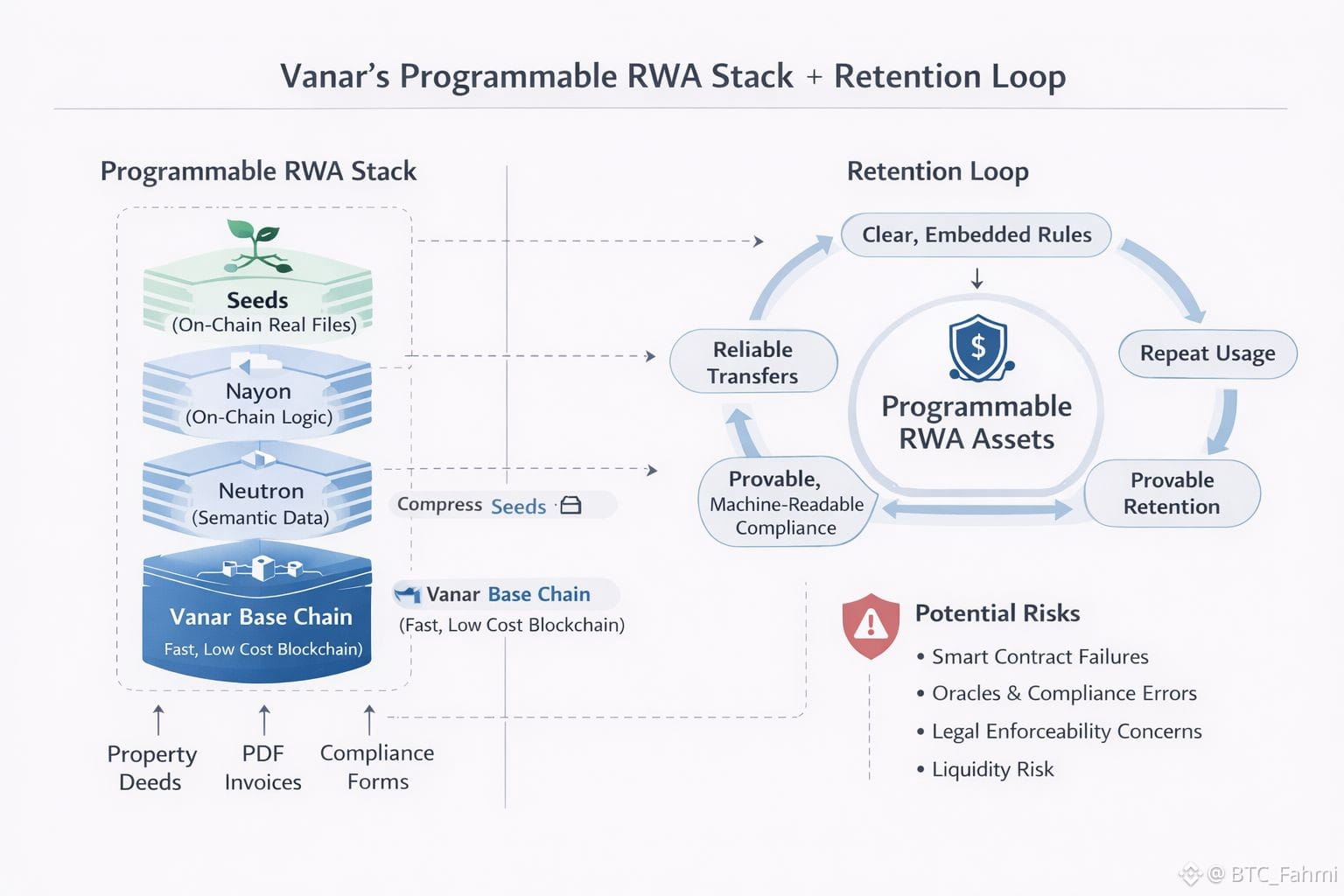

Vanar’s positioning is built around that difference. It describes itself as an integrated stack aimed at payments and tokenized real world assets, combining a base chain with components designed to make data and compliance machine readable on chain. On its site, Vanar frames the stack as a fast, low cost chain layer, a semantic data layer called Neutron that compresses real files into on chain “Seeds,” and an on chain reasoning layer called Kayon that can query and apply real time compliance logic. It also gives concrete examples of what that means in practice, like turning a property deed into a searchable proof, turning a PDF invoice into agent readable memory, and turning a compliance document into a programmable trigger.

It is worth pausing on why those examples matter. Tokenization always runs into the same bottleneck: the asset is not just a number. It is a bundle of rights, obligations, and constraints. A tokenized invoice is tied to a real counterparty, a real shipment, and a real dispute process. A tokenized deed is tied to local property law and registration. A tokenized treasury product is tied to issuance, custody, eligibility, and who is allowed to hold it. If those constraints are not legible to the system that transfers the token, then the transfer layer is blind, and you end up reintroducing intermediaries to compensate for that blindness.

The broader market is now big enough that this question is not academic anymore. RWA.xyz, an analytics dashboard for tokenized real world assets, currently shows distributed asset value around $24.02B and represented asset value around $356.53B, with total asset holders around 810,271, and stablecoin value around $296.04B at the time of viewing on January 29, 2026. Those numbers tell two stories at once. One is obvious growth. The other is structural: represented value can be far larger than what is actively distributed on public chains, because many tokenized programs still behave like controlled experiments, not like open market instruments.

You can see the institutional direction in policy signals too. On January 29, 2026, Reuters reported that the Bank of England is considering expanding the range of assets it could accept as collateral in tokenized form, and it referenced the European Central Bank’s plan to permit banks to use tokenized assets as collateral in Eurosystem credit operations from March 2026. That is a real incentive for the market to care about assets whose rules can be evaluated quickly and consistently, because collateral is not just about ownership, it is about enforceability under stress.

A practical example makes this less abstract. Imagine a mid size exporter that issues invoices to a large buyer with 60 day payment terms. The exporter wants liquidity today, a trader wants yield, and the buyer wants assurance that the invoice is genuine and not double pledged. In a weak tokenization model, you mint an “invoice token” and then everyone still asks for the PDF, the shipping proof, and a manual verification from a factoring desk. In a stronger model, the invoice token is linked to machine readable proofs that can be checked on chain, and it carries embedded constraints such as transfer eligibility, dispute windows, and payout waterfalls. If the buyer disputes within a defined period, the token’s cashflow path can pause. If the invoice is paid, the token can automatically redeem into stablecoins to the current holder. Neutron’s stated goal of compressing documents into provable, queryable on chain objects, paired with an on chain logic layer that can apply compliance checks, is aimed directly at making this kind of workflow less dependent on off chain glue.

This is also where the retention problem shows up, and it matters more than people admit. A lot of RWA platforms get a spike of attention when a new product launches, then usage fades because the day to day experience is not reliable. Users do not return to systems that feel like exceptions and workarounds. They return to systems that behave the same way every time, with rules that are clear, consistent, and verifiable. Embedding logic into the asset itself can reduce the number of “surprises” a user faces after they have already committed capital, and that predictability is what turns a one time experiment into repeat behavior.

None of this removes risk, and traders should treat “programmable” as a double edged word. If the logic is wrong, an error can scale instantly. Smart contract vulnerabilities, bad oracle assumptions, or flawed compliance rule sets can freeze liquidity or misroute funds. Legal enforceability still depends on how off chain rights are structured and in which jurisdiction the asset lives. Even if the on chain proofs are elegant, the real world still has disputes, fraud attempts, and regulatory changes. And liquidity risk is real: a token can be technically transferable and still have no natural bid during market stress, especially if the holder base is narrow or eligibility rules are restrictive.

So the useful investor question is not “will RWAs grow,” because the direction of travel is already clear. The better question is “which stacks make RWAs behave like instruments instead of souvenirs.” When you evaluate projects in this space, look for evidence that the rules are actually encoded and enforced at the token level, look for transparency about what is on chain versus what still relies on private attestations, and look for whether the user experience is built for repeat use instead of one time novelty. Vanar’s architecture claims to push in that direction by making data and compliance logic more native to the chain environment rather than bolted on later.

If you trade or invest in this category, do one simple thing this week: pick one tokenized asset product you understand, trace what really controls transfers and redemptions, and write down where the human approvals still hide. The projects that shrink that hidden surface area are the ones most likely to earn trust, liquidity, and the kind of retention that turns infrastructure into a market.