A central bank should be able to prove what happened the moment it happens. Not weeks later, after engineers reconstruct logs. SIGN makes that possible.

Last week, I spoke with a regulator at a regional central bank. He was excited about CBDC. The technical pilot was progressing. The vendor was capable. The timeline was aggressive.

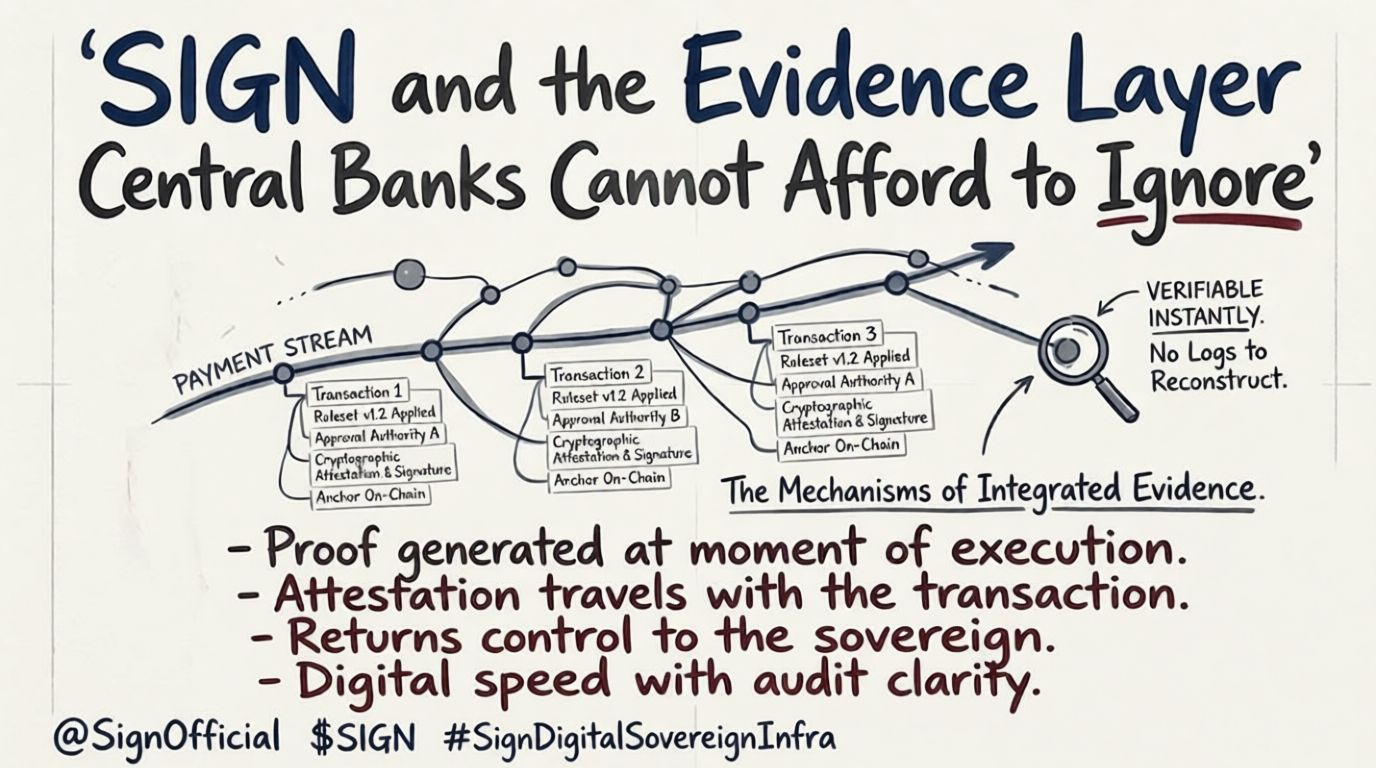

Then I asked him a question: when a payment executes, how do you prove cryptographically, instantly, without reconstructing logs what ruleset version applied at the moment of execution?

He paused. "We are still designing that part", he said.

This is the evidence gap. And it is the most overlooked vulnerability in the region's rush to digital money. For the regulator, the gap means delayed audits and blind spots. For the citizen using digital currency, it means disputes take weeks to resolve. For the economy, it means trust in the new money system is built on promises, not cryptographic proof.

SIGN closes this gap. It provides the evidence layer that turns digital money from a technical experiment into an accountable system.

Central banks across the Middle East are exploring CBDC and regulated stablecoins. The technical rails are being built. The policy frameworks are being drafted. But the evidence layer proving what payment executed under which authority, what ruleset applied, who approved is often treated as a compliance add-on rather than core infrastructure.

SIGN treats evidence as infrastructure. Every payment carries an attestation: ruleset version, approval authority, timestamp, cryptographic signature. The attestation is not a receipt stored separately. It is the evidence layer integrated into the transaction itself.

I examined the difference. In traditional systems, evidence is an archive. You execute, then you store records for later. In SIGN, evidence is operational. It is generated at the moment of execution and travels with the transaction. Verification happens in seconds, not weeks.

For Middle Eastern central banks, this matters beyond compliance. It matters for credibility. The region aims to establish itself as a center for digital finance. Worldwide investors, foreign partners, and domestic stakeholders will require transparency regarding the operation of these systems. A central bank capable of generating cryptographic proof of payment integrity in a matter of seconds demonstrates a level of operational maturity that conventional systems are unable to reach.

The requirements for a sovereign digital money system are clear: real-time settlement, policy controls, supervisory visibility, optional confidentiality for retail flows, interoperability across rails and networks. SIGN delivers these through its evidence layer. Every approval becomes an attestation. Every limit override is recorded. Every emergency action is cryptographically signed. Supervisors gain real-time visibility without disrupting privacy where required. The sovereign maintains control. The evidence remains inspectable.

I observed that the region's central banks are moving fast. Speed without accountability is not progress. It is risk. A digital currency without a verifiable evidence layer is just speed without accountability. SIGN gives central banks both.

Here is the mechanism. A central bank deploys a CBDC rail. Every transaction is processed through smart contracts. Before execution, the system checks the active ruleset. At execution, it generates an attestation cryptographically signed, anchored on-chain, containing the ruleset version, the approval authority, the timestamp. The payment settles. The attestation is verifiable instantly by supervisors, auditors, or counterparties with appropriate permissions.

No logs to reconstruct. No fragmented evidence. No weeks of delay.

For a sovereign nation, this is not a technical preference. It is a sovereignty requirement. When a payment system lacks an integrated evidence layer, the nation becomes dependent on vendors and third parties to reconstruct records after the fact. SIGN returns control to the sovereign. The evidence is cryptographic, not contractual.

I believe this is where the Middle East's digital money journey must go next. The first phase is building the rails. The second phase must be building the evidence layer those rails require. Without it, central banks gain digital speed but lose audit clarity. With it, they gain both.

SIGN provides the evidence layer that makes digital money inspectable without being interruptible. Every payment carries its own proof. Every approval is recorded. Every ruleset version is verifiable.

And the next time I ask a regulator how they prove what happened, they will not pause. They will point to the attestation.