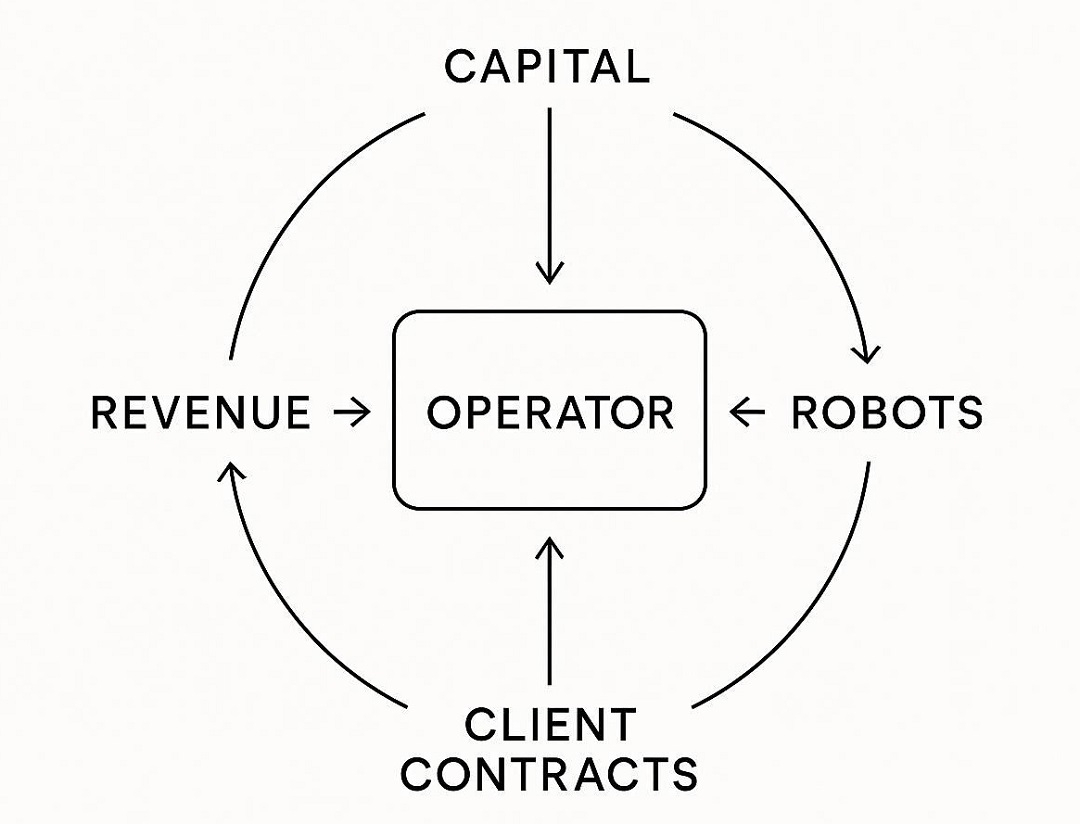

Most robotic fleets today operate inside closed financial loops.

A single operator raises capital.

That capital purchases hardware.

Operations — charging, maintenance, routing, compliance — are handled internally.

Contracts are signed bilaterally with customers.

Revenue flows back to the same centralized entity.

CAPEX in. Cash flow out. Everything contained.

At first glance, this seems efficient. It mirrors traditional asset-heavy industries. But structurally, it creates fragmentation.

Each fleet becomes its own software stack.

Each operator negotiates independently.

Each deployment is capital-constrained by institutional underwriting capacity.

There is no shared coordination layer.

This model worked when robotics was experimental. It becomes inefficient when automation demand is global.

Labor shortages in logistics, healthcare, manufacturing, and environmental services are not isolated phenomena. They are systemic. Demand for robotic labor is geographically distributed. Capital access is not.

When participation requires raising private equity and managing full-stack operations internally, access narrows to a small group of well-capitalized institutions.

Automation scales. Ownership concentrates.

Contrast this with coordination markets like ride-sharing networks. Drivers do not raise venture funds to purchase infrastructure stacks. They plug into shared systems that handle routing, payment settlement, and demand matching. The coordination layer abstracts complexity.

Robotics lacks that abstraction.

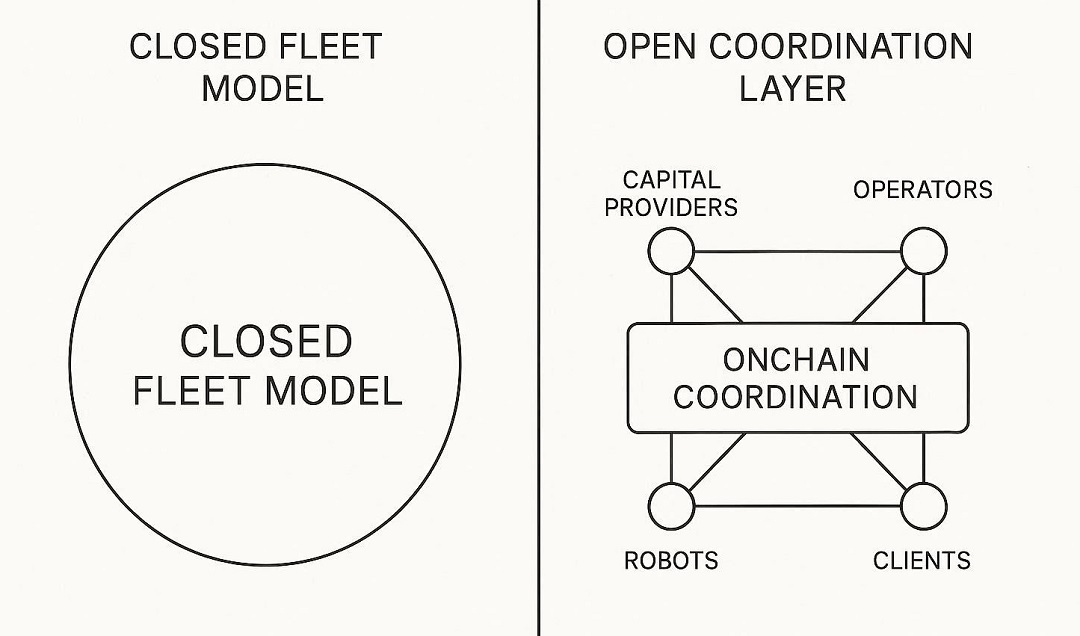

Fabric positions itself precisely at this structural gap.

Instead of closed-loop fleet ownership, Fabric proposes an open coordination and capital allocation layer where robot deployment, task verification, and settlement occur onchain. The objective is not to replace hardware operators, but to standardize how participation is coordinated.

In this model, capital contribution, operational support, and task execution are modularized rather than vertically integrated. User-deposited stable assets can support deployment. Verified task completion triggers settlement in $ROBO. Participation does not represent equity in hardware, but access to network coordination primitives.

The difference is subtle but structural.

Closed fleets internalize everything: capital, operations, revenue.

Open coordination layers separate roles:

Capital provision.

Operational maintenance.

Task demand.

Settlement.

This separation increases composability.

$ROBO functions as the required network asset within this architecture — facilitating identity registration, coordination staking, and payment settlement. Not as speculative exposure to hardware, but as infrastructure for participation.

The current fleet model optimizes for control.

An open coordination model optimizes for scale.

If global automation demand continues to outpace institutional capacity to deploy fleets independently, the bottleneck will not be hardware. It will be coordination.

The question is not whether robots can work.

The question is whether we will continue organizing them inside financial silos — or build shared infrastructure capable of matching global demand with distributed participation.

Structural inefficiencies do not disappear. They get abstracted.

The fleet model solved the first phase of robotics.

It may not solve the next one.

@Fabric Foundation $ROBO #ROBO #robo