I have been thinking about SIGN a lot lately, and honestly, I feel like most people are looking at it the wrong way.

A lot of tokens launch first and then spend years trying to prove they are useful. SIGN feels like the opposite. The business was already making money before the token really mattered, and that changes the whole story.

That part is important.

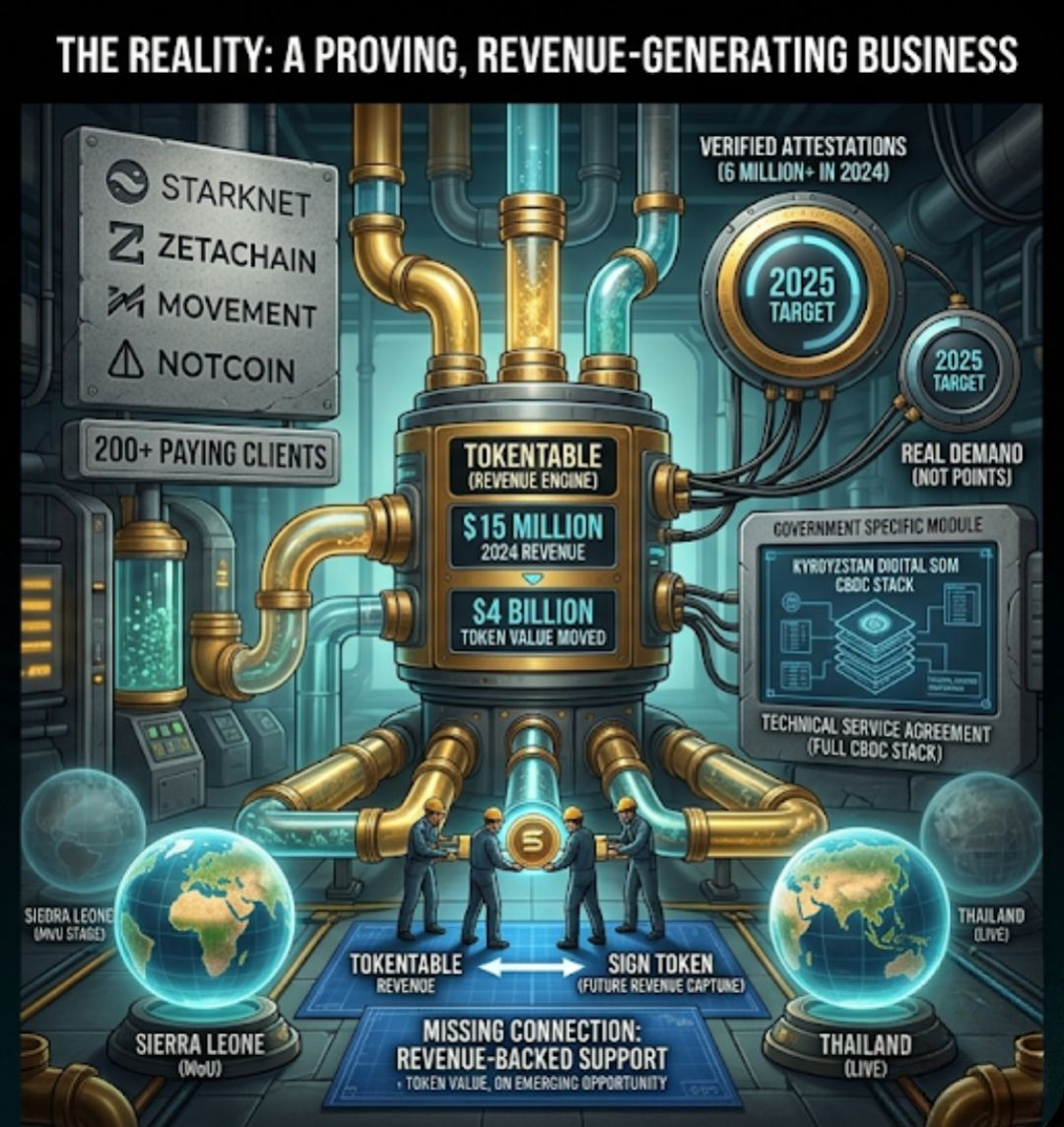

TokenTable, which is part of SIGN, reportedly made about $15 million in 2024. That was real revenue. Not a prediction. Not a hopeful estimate. Real money from real clients. Projects like Starknet, ZetaChain, Movement, and Notcoin used the service. More than 200 projects paid for token distributions, vesting support, and airdrop setup through the platform.

On top of that, about $4 billion in token value moved through the system, reaching more than 40 million wallets.

That is not a small number. That is real usage.

And what makes it even more interesting is that the SIGN token did not exist for most of that time.

So the business was already working before the token came into the picture. That is rare in crypto. Usually it goes the other way around. A token launches first, then the team tries to build a business later. Here, the business came first.

That is why I think SIGN deserves more attention.

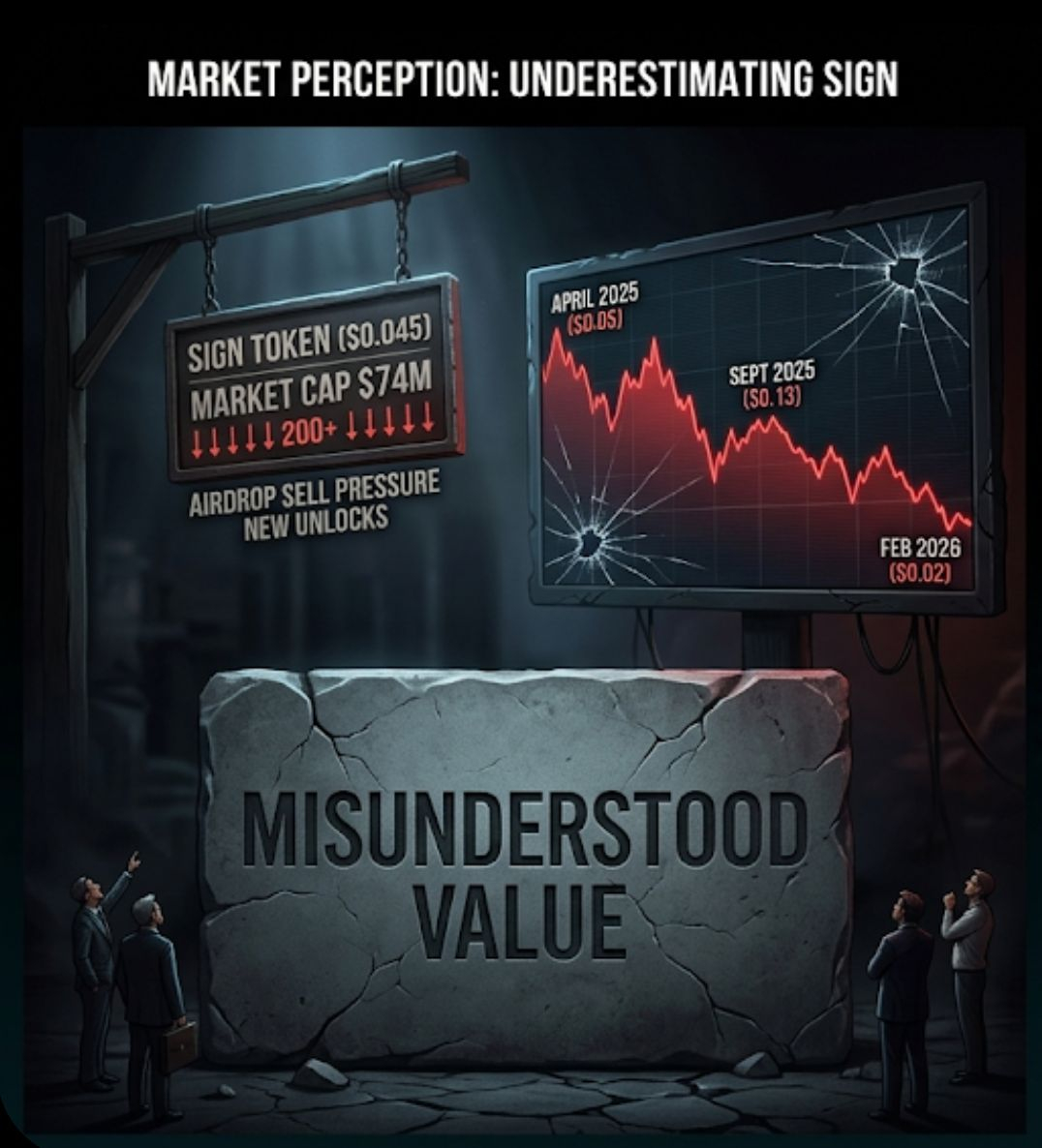

At around $0.045 and a market cap near $74 million, the token looks cheap compared with what is behind it. You are looking at a project with more than 200 paying clients, real infrastructure use, and government related work in multiple places.

If this were just a normal company outside of crypto, a lot of people would probably call that a strong business.

But because it is a token, the market seems to be treating it like a weak one.

I do not think that makes sense.

Yes, the price has had a rough run.

The token launched in late April 2025. It started with strong volume, then climbed from around $0.05 to about $0.13 by late September 2025. After that, it fell hard and dropped to around $0.02 in February 2026.

That is a painful move. No point pretending otherwise.

But when I looked at what caused the drop, I did not see a business breakdown.

The clients were still there. The activity was still there. The government work was still there. What looked broken was the supply side, not the actual product.

New tokens kept unlocking every month. Some people who got airdrops probably never planned to hold for long. Some of the early excitement faded when the Kyrgyzstan CBDC timeline turned out to be slower than people expected.

So the token price got hit hard while the business kept moving.

That is where I think many people got confused.

They treated token price and business health like they were the same thing. They are not.

One of the strongest things about SIGN is the attestation activity.

In 2024, Sign Protocol handled more than 6 million on chain attestations. The target for 2025 is 12 million.

In simple words, an attestation is a verified proof of something. It could be a government checking a credential, a KYC result linked to a wallet, or a signed record that needs to be trusted later.

That matters because it is real usage. It is not random noise. It is not just people clicking around for points. It is actual demand for the system.

And this happened before the token existed, which makes it even more meaningful. There was no token reward pushing activity. The usage was coming from real need.

That is rare in this space.

A lot of on chain activity can be fake or easy to inflate. But verified attestations tied to real institutions are much harder to fake. That is one reason I think the market is still underestimating what SIGN has already built.

The government side is also real, but it needs to be talked about honestly.

The Kyrgyzstan Digital Som deal is legitimate. There is a technical service agreement with the National Bank. It was signed publicly, with the country’s leadership present, and it covers the full CBDC stack, including settlement, treasury payments, and offline features.

That is a serious partnership.

Still, the timeline is what it is. The full issuance decision is not immediate, and people should not expect a fast payoff from that story. If someone is buying SIGN today just because they think Kyrgyzstan is going to turn into a huge price move in the next few months, they may be disappointed.

Sierra Leone is still early too. It is at the MoU stage, which is not the same thing as a finished rollout. That does not mean it is meaningless, but it does mean it is too early to price it like a done deal.

At the same time, there is something the market seems to ignore.

SIGN is already live in the UAE and Thailand.

Not rumored. Not planned. Live.

That is important. It means the project is not just about future promises. It is already being used in the real world right now.

That is why I think people are focusing too much on the loud headlines and not enough on the quiet proof that adoption is already happening.

The biggest issue, though, is the gap between the business and the token.

Right now, the $15 million in revenue does not automatically translate into support for the token. When TokenTable earns money, that does not directly create demand for SIGN. The team did do a buyback in August 2025, which was a good sign. It showed they understand the problem. But one buyback is not the same as a system where revenue naturally flows back into the token.

That missing connection matters a lot.

A project can have a strong business and still have a weak token if the token design is not tied closely enough to the business. I think that is where SIGN is right now. The business looks strong. The token structure still feels unfinished.

That is the main thing I am watching.

If they ever announce a clear system where TokenTable revenue is used for scheduled buybacks or a protocol burn, that would change the conversation fast. At that point, the revenue would not just prove the business is real. It would also give the token a direct support structure.

That would matter a lot.

I should also be honest that I hold SIGN. I bought below $0.03 after the February low because the numbers made sense to me and the valuation looked too low for what the business had already proven. So I am not pretending to be neutral here.

I have skin in the game.

My view is simple.

This is a project with real revenue, real clients, millions of attestations, and live government use. It was already working before the token was even part of the story. Yet the token still got crushed while the business kept going.

To me, that looks more like supply pressure than a real failure in the business.

Maybe the token stays weak for longer than people expect. Maybe the next catalyst takes time. That is possible. But even if that happens, it does not change what the underlying business already is.

That is why I think SIGN is being misunderstood.

A lot of people are treating it like just another token. I think the real story is the business underneath it.

And eventually, I think the market will have to notice that.