It didn’t feel like a typical crypto headline

At first, the news sounded familiar — another crackdown, another frozen wallet, another number attached to a geopolitical story.

But this one lingered a little longer.

The United States freezing $344 million in crypto tied to Iran wasn’t just about stopping money. It quietly exposed how the system actually works beneath the surface — not how we imagine it, but how it behaves when pressure is applied.

And once you see it that way, it stops being just a crypto story.

What really happened

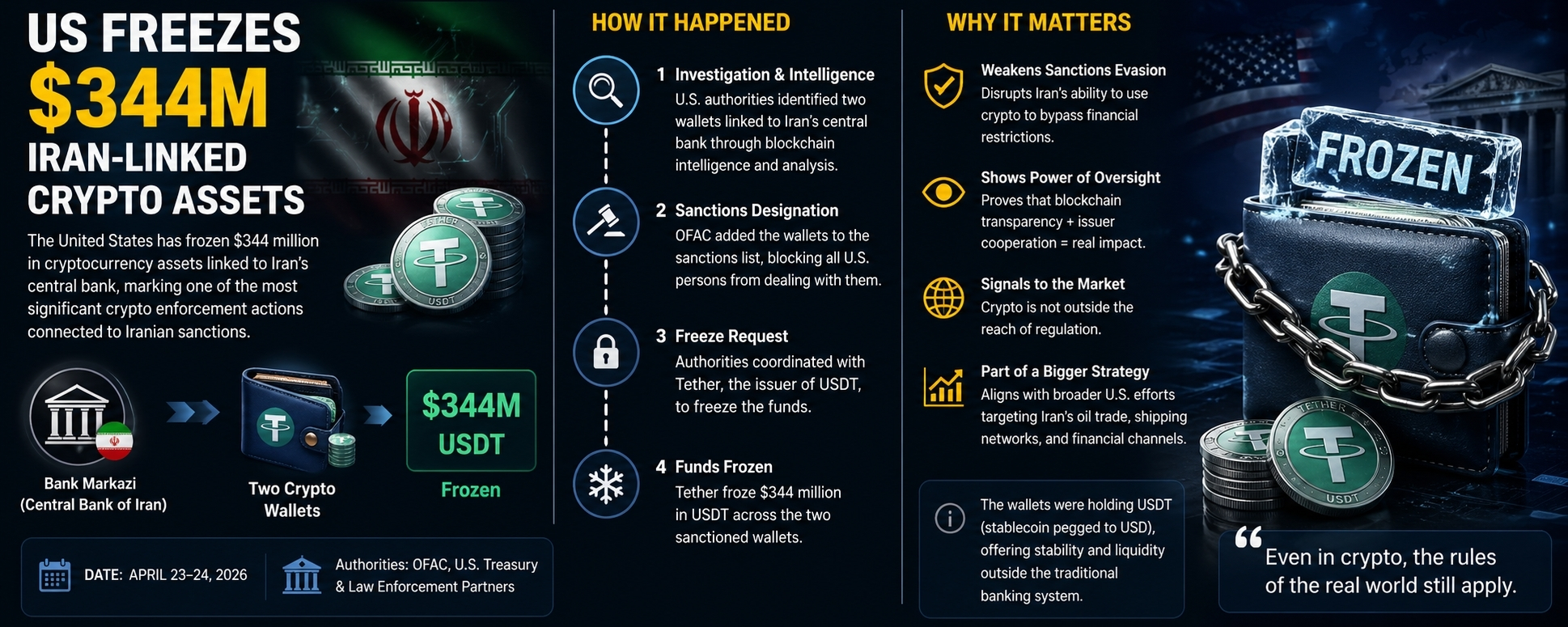

In April 2026, U.S. authorities identified two crypto wallets believed to be connected to Bank Markazi.

These wallets held a large amount of USDT — a digital version of the dollar issued by Tether.

Soon after:

The wallets were added to the sanctions list by Office of Foreign Assets Control

The funds inside them — about $344 million — were frozen

The freeze happened with direct coordination between authorities and the issuer

Nothing dramatic unfolded on-chain.

The money didn’t disappear.

It didn’t get stolen.

It simply became unusable.

On the surface, it looks simple

From a policy perspective, this is straightforward.

Iran has been cut off from much of the global financial system for years. Crypto offered an alternative path — a way to hold and move value without relying on banks.

So when authorities identified wallets linked to that system, they acted.

In that sense, the story is easy to understand:

A sanctioned entity used crypto → it got identified → the funds were frozen.

Clean. Efficient. Predictable.

But the details tell a different story

What makes this case interesting isn’t just the freeze — it’s how those wallets were behaving before it happened.

They weren’t actively sending money around.

They weren’t constantly interacting with exchanges or new addresses.

Instead, they looked… quiet.

Funds had been flowing in over time, but very little was going out.

It didn’t look like a payment system.

It didn’t look like laundering in motion.

It looked more like storage.

Almost like a digital reserve sitting patiently in the background.

Why stablecoins were the obvious choice

If you step into that situation — cut off from global banking — the logic becomes clear.

You need something that:

Holds stable value

Moves across borders easily

Doesn’t rely on traditional institutions

That’s exactly what stablecoins offer.

They act like digital dollars without needing a bank account.

So it makes sense that they became part of the strategy.

But there’s a catch that doesn’t show up at first glance.

The part most people overlook

Stablecoins feel like crypto — fast, global, borderless.

But they’re not entirely free.

Behind them is a company.

And that company can intervene.

In this case,Tether had the ability to freeze those funds once authorities flagged the wallets.

That’s the trade-off built into the system:

You get stability and convenience

—but you give up full control

Most of the time, that trade-off stays invisible.

Until something like this happens.

When the system shows its real shape

This is the moment where perception and reality separate.

Crypto is often described as decentralized, unstoppable, outside of control.

And in many ways, parts of it are.

But not all of it.

When stablecoins are involved, there’s always a point where control can re-enter the system.

And when it does, it’s decisive.

No chase.

No delay.

No negotiation.

Just a switch being flipped.

What this means for Iran

For Iran, the impact goes beyond the number itself.

Losing access to $344 million is significant, but the deeper issue is what it reveals.

It shows that even alternative financial strategies have limits.

That even outside the traditional banking system, there are still points of vulnerability.

And it forces a difficult question:

If not stablecoins, then what?

Other options exist, but none offer the same balance of stability, liquidity, and usability.

Every alternative introduces new problems — volatility, complexity, or reduced access.

What this means for crypto as a whole

This is where the conversation gets uncomfortable.

Because the takeaway isn’t just about one country or one enforcement action.

It’s about the nature of the system itself.

Crypto isn’t purely decentralized anymore.

It’s becoming something more layered:

Decentralized at the base

Controlled at key entry and exit points

Stablecoins, issuers, infrastructure providers — these are the new control layers.

They don’t stop the system from functioning.

They shape how it behaves under pressure.

A shift in how enforcement works

There’s also a subtle but important shift happening here.

In the past, financial enforcement often came after the fact.

Money moved first.

Authorities reacted later.

Now it’s different.

Funds can be stopped before they move again.

That changes the dynamic entirely.

It turns crypto from just a record of transactions

into a system where intervention can happen in real time.

The bigger picture

This wasn’t just about freezing money.

It was about showing that even in a system designed to reduce reliance on centralized power,

that power still exists — just in new forms.

The tools have changed.

The structure has evolved.

But the underlying reality hasn’t disappeared.

Final thought

The $344 million is still there.

You can see it on-chain.

You can trace its history.

But it can’t move.

And that’s the part that matters.

Because in the end, this story isn’t about how fast money can travel.

It’s about something simpler —

who gets to decide when it stops.