#USJobsData

⸻

MODEL OBJECTIVE

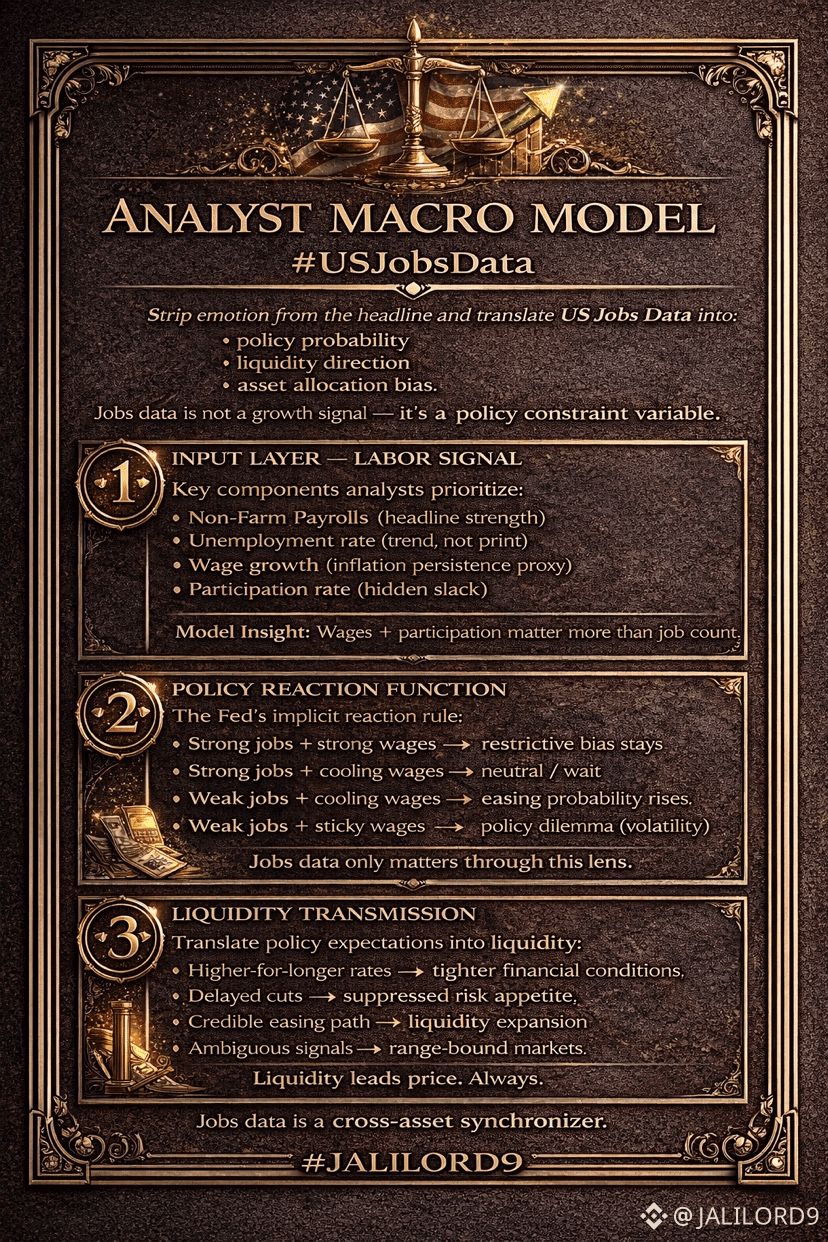

Strip emotion from the headline and translate US Jobs Data into:

• policy probability

• liquidity direction

• asset allocation bias

Jobs data is not a growth signal — it’s a policy constraint variable.

⸻

🧠 1️⃣ INPUT LAYER — LABOR SIGNAL

Key components analysts prioritize:

• Non-Farm Payrolls (headline strength)

• Unemployment rate (trend, not print)

• Wage growth (inflation persistence proxy)

• Participation rate (hidden slack)

Model Insight:

Wages + participation matter more than job count.

⸻

⚖️ 2️⃣ POLICY REACTION FUNCTION

The Fed’s implicit reaction rule:

• Strong jobs + strong wages → restrictive bias stays

• Strong jobs + cooling wages → neutral / wait

• Weak jobs + cooling wages → easing probability rises

• Weak jobs + sticky wages → policy dilemma (volatility)

Jobs data only matters through this lens.

⸻

💵 3️⃣ LIQUIDITY TRANSMISSION

Translate policy expectations into liquidity:

• Higher-for-longer rates → tighter financial conditions

• Delayed cuts → suppressed risk appetite

• Credible easing path → liquidity expansion

• Ambiguous signals → range-bound markets

Liquidity leads price. Always.

⸻

📉 4️⃣ ASSET CLASS RESPONSE MATRIX

• Equities: Sensitive to wage-driven rate expectations

• Bonds: React first, confirm later

• USD: Strengthens with restrictive bias

• Crypto: Trades liquidity expectations, not jobs

• Gold: Benefits from policy credibility loss

Jobs data is a cross-asset synchronizer.

⸻

🧩 5️⃣ VOLATILITY FILTER

High volatility conditions emerge when:

• headline beats but revisions disappoint

• wages surprise while payrolls miss

• participation shifts suddenly

These are false-confidence zones where positioning gets punished.

⸻

📊 MODEL OUTPUT

Bullish risk regime:

✔ Cooling wages

✔ Stable employment

✔ Rising easing probability

Bearish risk regime:

✖ Hot wages

✖ Policy delay

✖ Tight liquidity

Neutral/chop regime:

➖ Mixed labor signals

➖ Fed ambiguity

➖ Range-bound positioning

⸻

🧠 ANALYST CONCLUSION

#USJobsData is not a directional trade by itself.

It is a macro input that:

• shapes policy probabilities

• dictates liquidity expectations

• filters risk-on vs risk-off regimes

Analysts don’t trade the number.

They trade the second-order effects.

⸻

🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎🌎