Validators typically are exchangeable providers of compute, according to blockchains. Plasma solves them as systemically relevant operators. This difference almost fills all idiosyncratic choices in its consensus, incentive structure, and XPL economics.

Stablecoin infrastructure does not collapse as speculative networks do. Resistance to censorship and liquidity of memes are not the main threat, but stress liveness. Settlement uncertainty can cascade around missed blocks in market dislocations, exitors in volatility, or correlated slashing. The validator architecture of Plasma is constructed so as to reduce these failure modes as opposed to maximizing such adversarial punishment.

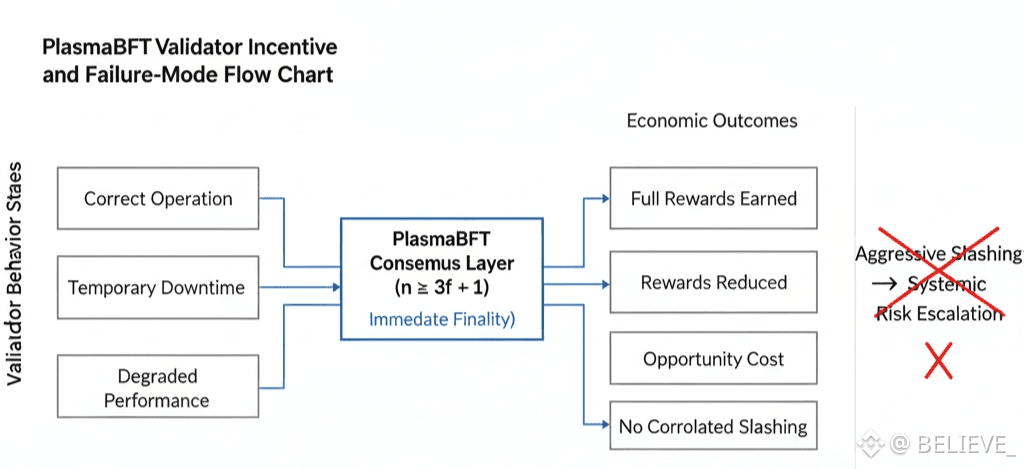

PlasmaBFT is running on classical Byzantine assumptions (n [?] 3f + 1), but the economic layer is not what is taught in mainstream Proof-of-Stake. Plasma does not concentrate on aggressive downtime-cutting, but rather, it focuses on reward-based incentives. Theerson and Stidi of the losing-practical kind of validator do not lose principal; they lose opportunity. It is not an ideological decision, but an operation one. Network congestion would increase systemic risk instead of limit it in the case of correlated slashing in stablecoin-heavy environments.

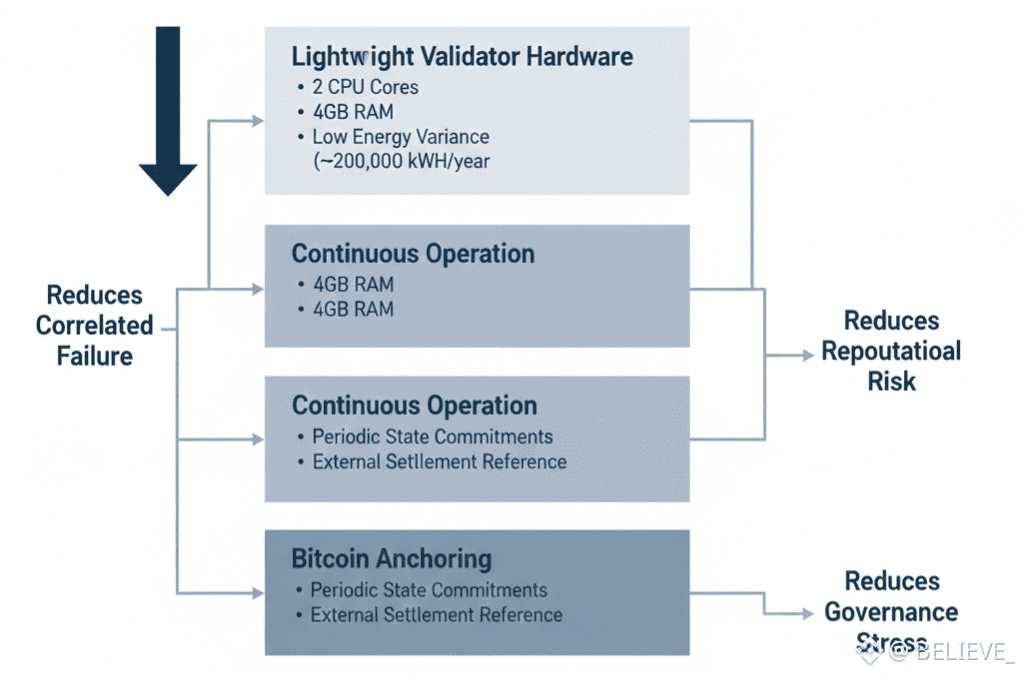

This reasoning is augmented in the hardware requirements. A validator may run with minimal CPU cores and memory, 2 and 4GB, respectively, which reduces the fragility of its operation to a considerable extent. Reduced requisites, minimize the likelihood of coordinated cataclysmic failures due to cloud failures, equipment shortages, or expedited cost increases. The 150-300 operators promised by Plasma in year one are deliberately not large enough to make plasma too decentralized, but at the same time are not too big to allow efficient coordination instead of pursuing vanity measures.

The role played by XPL in this system is limited. It is staked with validator participation, which is executed at the price, and subsequent governance- but does not motivate to rent on transaction volume. XPL will not allow adjustments to be used to weaponize monetary policy during market stress because it is fixed and has no adjustment mechanism. This stability is important when the institution has to model long term security costs without being subject to discretionary dilution.

The validator is another thesis that is established through energy data. The annual consumption of Plasma is estimated to be approximately 200,000 kWh, and is more aligned with the traditional financial infrastructure, as opposed to general-purpose blockchains. This efficiency does not happen by chance. Validators are supposed to work 24 hours as opposed to on-command. The reduction in energy variance decreases variability in its operations and makes engagement an option of regulated parties that are required to publish sustainability indicators.

The last constraint is provided by the Bitcoin anchoring layer. Plasma by making state biperiodic commitments to Bitcoin, without burdening day-to-day operations of Bitcoin with its execution latency, presents an external settlement reference. In the case of validators, this decreases reputational risk. Conflicts are no longer resolved just inside the social layer of Plasma; those acquire a cryptographic audit trail pegged to a neutral base layer.

Establishment of governance is purposely procrastinated. Although the voting on protocol parameters will be done by the XPL holders in the long term, governance is not front-loaded to the early lifecycle. This is in lieu of a frequent failure mode in which insufficiently tested networks are compelled to prematurely ossify under pressure of token-holders. Plasma puts stability of operation over political expressiveness.

The validator economics also has a direct interaction with the sale design of Plasma. Since the deposits of the vaults allocated to are bridged to Mainnet Beta, early network liquidity is not speculative: it is functional. With Stablecoins already on-chain, validators do not need to be dependent on mercenary capital or incentive programs to operate.

Conclusion

The validator model of plasma is not a competitive approach that is optimized around crypto-native competition; it is a competitive approach that is optimized around institutional tolerance. Plasma creates a network in which degradation occurs in a predictable and not catastrophic manner by reducing slashing reflexivity, reducing hardware fragility, correcting XPL supply, and forcibly stapling settlement to the outside.

The resilience in the infrastructure of stable coins is not quantified by the behaviour of a system when everything is doing well- but when nothing is doing well. The selections made in the design of Plasma indicate that it is cognizant of that difference.