🚨 COPPER IS ENTERING A STRUCTURAL SUPERCYCLE

Copper Is Quietly Setting Up One Of The Most Important Long-Term Supply Shocks Of This Generation.

This Is Not A Short-Term Trade Narrative — It Is A Multi-Decade Macro Shift Driven By Math, Physics, And Infrastructure Reality.

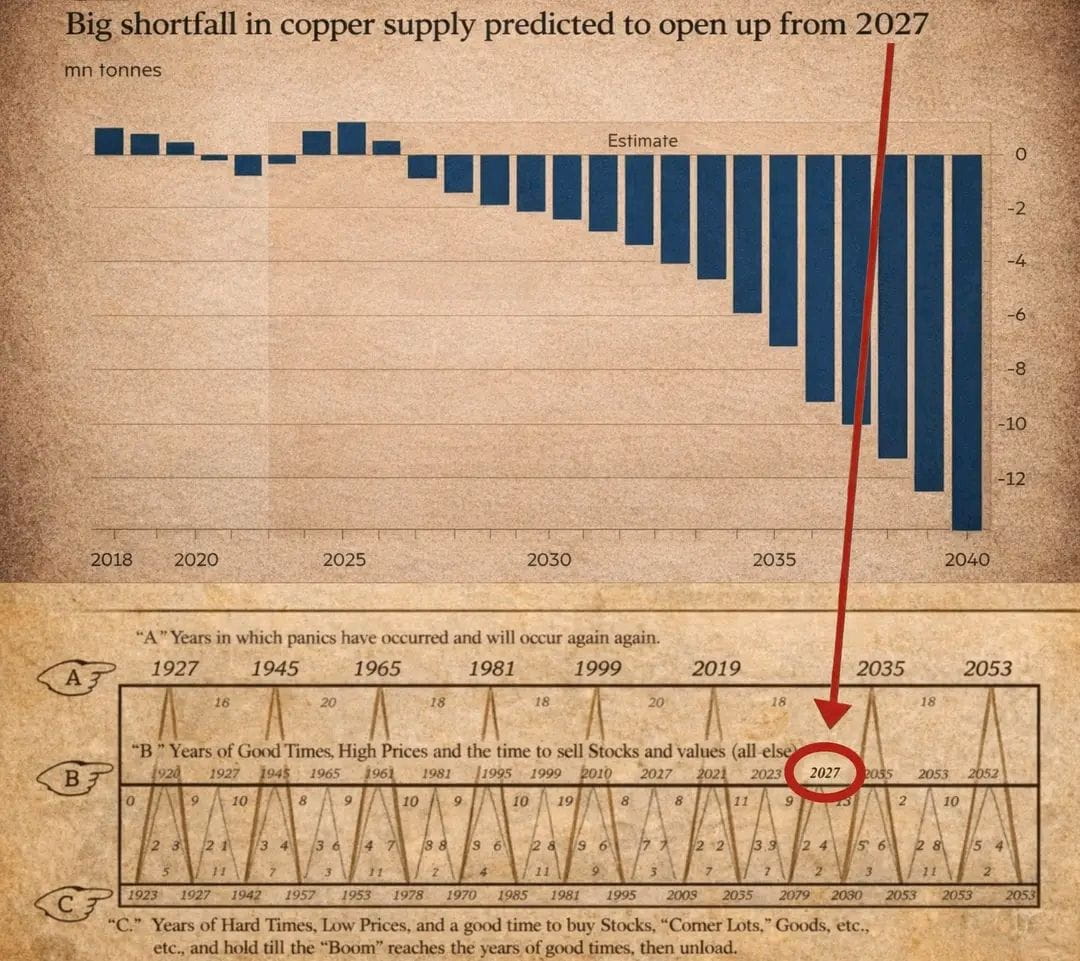

Multiple Institutional Forecasts, Including Bernstein, Indicate That A Structural Copper Shortage Could Begin Around 2027 And Intensify Through 2050.

Here’s Why This Matters.

→ DEMAND IS ACCELERATING

→ SUPPLY IS STRUCTURALLY CONSTRAINED

→ THE GAP IS MATHEMATICALLY UNSUSTAINABLE

Below Is The Framework Explaining Why Copper Is Entering A New Supercycle.

1) THE SUPPLY CLIFF — THE CORE PROBLEM

Copper Supply Is Facing A Severe Structural Bottleneck.

• There Are Virtually No Major New Copper Mines Coming Online

• Permitting And Development Takes 17–20 Years On Average

• Even If A Large Deposit Were Discovered Today, Meaningful Production Would Likely Not Begin Until The 2040s

At The Same Time:

• Ore Grades Are Declining

• The Highest-Quality Deposits Have Already Been Extracted

• Mining Is Becoming Deeper, More Expensive, And Less Efficient

According To S&P Global, The World Could Face An Annual Copper Deficit Of Approximately 10 Million Tonnes By 2040 — Roughly 25% Of Projected Demand At Current Price Levels.

This Is Not A Cyclical Issue.

It Is A Structural Supply Constraint.

2) THE AI AND ENERGY INFRASTRUCTURE SHOCK

Copper Demand Is No Longer Driven Only By Traditional Industrial Use.

Artificial Intelligence Is A Major New Demand Driver.

• Data Center Capacity Is Projected To Increase Dramatically By 2040

• AI Systems Require Enormous Electrical Power And Advanced Cooling

• Liquid Cooling Infrastructure Relies Heavily On Copper Plates, Tubing, And Piping

The Existing Power Grid Cannot Support This Load Without Massive Upgrades.

• Millions Of Miles Of New Transmission Lines Are Required

• Substations, Transformers, And Distribution Networks Are Copper-Intensive

• Grid Expansion Is Capital-Heavy And Time-Consuming

This Demand Is Structural, Not Optional.

3) ELECTRIFICATION AND THE ENERGY TRANSITION

Even Without AI, Copper Demand Was Already Rising Rapidly.

• Electric Vehicles Use Approximately Three Times More Copper Than Internal Combustion Vehicles

• Wind And Solar Installations Are Highly Copper-Intensive

• Battery Storage, Charging Infrastructure, And Grid Stabilization All Increase Copper Consumption

The World Is Attempting To Rebuild Global Energy Infrastructure Over The Next 25 Years Using A Metal That Is Already In Short Supply.

This Is A Physical Constraint, Not A Policy Debate.

4) COPPER AS A STRATEGIC ASSET

When Supply Tightness Becomes Acute, Copper Will No Longer Trade Like A Typical Industrial Commodity.

• Manufacturers Will Compete Aggressively For Inventory

• Securing Supply Will Matter More Than Spot Pricing

• Strategic Stockpiling Will Increase

In Such Environments, Pricing Becomes Non-Linear.

Copper Transitions From An Industrial Input To A Strategic Resource.

5) THE BIG PICTURE

This Setup Does Not Depend On Speculation Or Sentiment.

It Is Driven By:

• Long Lead Times

• Declining Supply Quality

• Infrastructure Reality

• Energy Demand Growth

Markets Tend To Underprice These Dynamics Until Shortages Become Visible — At Which Point Repricing Happens Quickly.

FINAL THOUGHT

Copper Does Not Need Hype.

It Needs Time.

The Structural Forces Are Already In Motion.

Those Who Study Long-Term Supply-Demand Dynamics Understand Why This Market Deserves Attention.

Macro Cycles Reward Preparation — Not Reaction.

Sometimes The Market Moves Quietly For Years Before The Adjustment Becomes Impossible To Ignore ⚠️