Most blockchain projects announce ambitious roadmaps then spend years attempting to attract initial liquidity and community participation. Plasma experienced opposite problem on June twelfth twenty twenty-five when reopening deposits after reaching initial five hundred million dollar target. The revised one billion dollar cap filled in under thirty minutes with participation from twenty-nine hundred wallets and median deposit of twelve thousand dollars. This wasn’t blind speculation but calculated bet by sophisticated participants who studied months of preparation involving novel token sale infrastructure, strategic hiring across payments and security, and deepening relationship with entities controlling majority of global stablecoin supply. The story reveals how modern blockchain projects must simultaneously build technical infrastructure, regulatory frameworks, community trust, and institutional relationships long before any code executes on mainnet.

The relationship between Plasma and Tether ecosystem extends beyond typical investor-project dynamic into structural interdependence rarely acknowledged publicly. Paolo Ardoino serves simultaneously as Tether CEO and Bitfinex chief technology officer while appearing on Plasma’s cap table as individual investor. Bitfinex led both seed round in October twenty twenty-four providing three point five million dollars and Series A in February twenty twenty-five contributing portion of twenty-four million alongside Framework Ventures and Founders Fund. The corporate entities exist under iFinex umbrella where Giancarlo Devasini holds chairman position and roughly forty to forty-seven percent ownership stake valued in tens of billions given Tether’s extraordinary profitability. These aren’t arm’s length business relationships but tightly integrated network where key principals share corporate governance, investment decisions, and strategic direction across multiple legal entities.

The USDT0 involvement adds additional complexity. This cross-chain version of Tether managed by Everdawn Labs based in British Virgin Islands same location that housed Tether until recent El Salvador relocation shares not just geographic registration but reported family connections. Investigative reporting traced Everdawn director Lorenzo Romagnoli as likely nephew of Devasini through family relationships verified via social media and Italian media sources. The corporate addresses match precisely between Everdawn and historical Tether locations suggesting operational proximity beyond coincidental similarity. When Plasma announces zero-fee USDT transfers and integrates USDT0 as core asset, they’re building on infrastructure controlled by closely related entities where strategic alignment matters more than typical third-party partnerships. If it becomes necessary to prioritize one stablecoin over others, the relationship structure practically guarantees that choice favors Tether products.

The Echo Platform Debut Creating Fair Launch Infrastructure

The decision to conduct first public sale using Echo’s newly launched Sonar platform represented conscious choice about market positioning and community building. Echo founded by influential trader Cobie who invested in Plasma’s seed round had established reputation for private investment infrastructure enabling early-stage projects to raise capital from sophisticated investors. The Sonar product launch marked expansion into public token sales with emphasis on compliance and fair allocation rather than maximizing capital raised. Plasma’s ten percent supply allocation priced at five cents per token with five hundred million fully diluted valuation offered same terms as Founders Fund received in private investment round, explicitly designed to avoid typical venture capital dynamic where insiders receive massive discounts unavailable to public participants.

The mechanics required depositing stablecoins including USDT, USDC, USDS, or DAI into Plasma vault built using Veda contracts already securing two point six billion dollars across other projects. Time-weighted deposits determined allocation meaning participants who deposited early and maintained positions throughout campaign earned proportionally more units than those arriving late or withdrawing before close. The system created incentive for conviction rather than speculation because removing funds reduced final allocation. Once deposit period closed on July fourteenth, all positions locked for minimum forty days until mainnet beta launch when vault positions would bridge to Plasma blockchain and become withdrawable alongside XPL token distribution. The extended lockup addressed regulatory compliance particularly for US participants requiring twelve-month restriction until July twenty-eighth twenty twenty-six while non-US buyers received tokens immediately upon mainnet launch.

The campaign targeting fifty million dollar raise received three hundred seventy-three million in commitments requiring refunds for excess amounts. The overwhelming demand validated thesis that stablecoin infrastructure represented underserved market segment despite skepticism from those noting five hundred million valuation for project without launched mainnet. The distribution analysis showed seventy percent of deposits concentrated in top one hundred addresses with fifty-eight percent denominated in USDC and forty percent in USDT, suggesting institutional and high net worth individuals formed core participant base rather than broad retail enthusiasm. The median twelve thousand dollar deposit indicated barrier to entry excluded casual speculators while attracting participants treating allocation as meaningful portfolio position. They’re committing capital not based on hype but calculated assessment that purpose-built stablecoin blockchain addresses genuine friction points in existing infrastructure.

Building Team Capable Of Executing Payments At Global Scale

The strategic hiring announcements in September twenty twenty-five weeks before mainnet launch signaled organizational maturity beyond typical crypto project assembling anonymous developers. Murat Firat joining as head of product brought experience founding BiLira, Turkey’s largest cryptocurrency exchange and Turkish Lira-pegged stablecoin issuer. His background navigating regulatory requirements for fiat-pegged stablecoins in emerging market with volatile currency and complex compliance environment provided precisely relevant expertise for Plasma’s mission targeting global stablecoin adoption. Turkey represents microcosm of markets where citizens desperately need access to stable value but face regulatory uncertainty and infrastructure limitations, exactly the problems Plasma claims to solve at protocol level.

Adam Jacobs appointment as head of global payments carried both valuable expertise and reputational complexity. His role as global head of payments at FTX before exchange’s catastrophic collapse meant direct experience building payment infrastructure at scale serving millions of users, but also association with industry’s most spectacular fraud. The subsequent position at Canadian fintech firm Nuvei demonstrated ability to rebuild career in legitimate payments space, suggesting Plasma viewed technical competence as outweighing reputational baggage. The willingness to hire someone from FTX wreckage indicated confidence that Jacobs possessed genuine skills rather than just benefiting from unsustainable business model, or perhaps recognition that crypto industry’s limited talent pool means accepting candidates with complicated histories. We’re seeing pattern where projects prioritize demonstrated capability over pristine backgrounds when building operations teams rather than public-facing roles.

Usmann Khan’s appointment as head of protocol security brought credibility from ranking sixth on ImmuneFi’s cryptocurrency bug bounty leaderboard. The platform rewards security researchers for identifying vulnerabilities in smart contracts and blockchain protocols, creating reputation system where rankings correlate with technical sophistication and track record finding critical issues before malicious actors exploit them. The specialized expertise in smart contract security matters enormously for project handling billions in stablecoin transfers where single vulnerability could enable catastrophic theft. Jacob Wittman joining as general counsel provided blockchain legal and compliance experience essential for navigating regulatory uncertainty as governments worldwide implement stablecoin frameworks. The anonymous contributors river0x as DeFi lead and murf as senior product designer maintained crypto tradition of pseudonymous development while presumably bringing technical capabilities justifying inclusion despite lack of public credentials.

The Token Economics Designed Around Controlled Distribution

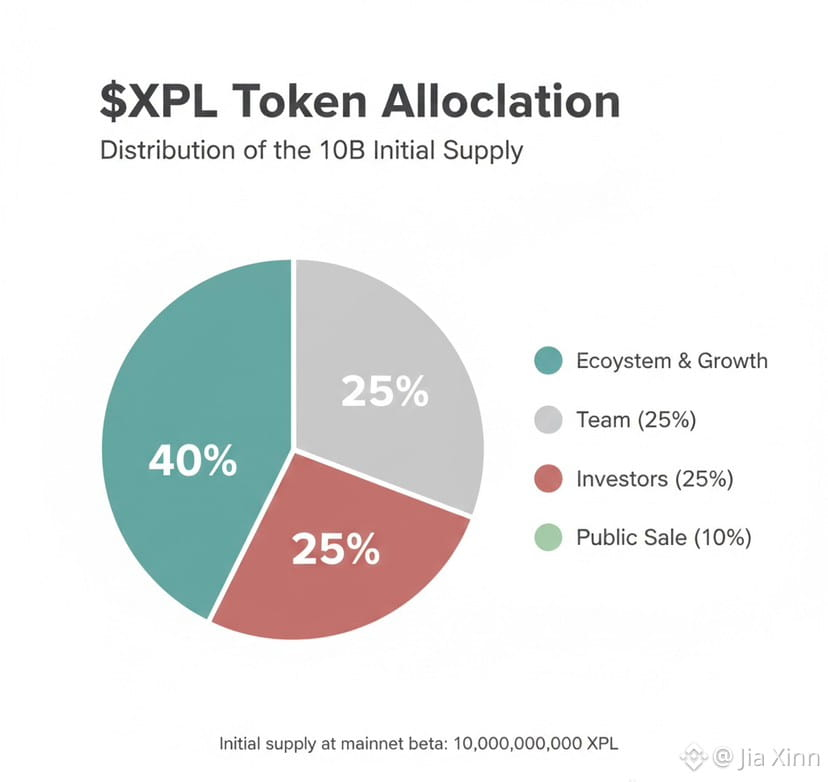

The ten billion genesis supply with eighteen percent circulating at launch reflected deliberate approach to managing sell pressure while ensuring sufficient liquidity for functional market. The allocation reserved forty percent for ecosystem and growth initiatives with eight percent unlocked at mainnet providing eight hundred million tokens for initial activities including liquidity provision and partnership incentives. The remaining thirty-two percent vests monthly over thirty-six months creating predictable supply schedule where approximately one hundred six million XPL enters circulation each month starting mid twenty twenty-six. Team and investor allocations of twenty-five percent each face three-year vesting with one-year cliff meaning no tokens unlock during first twelve months then release proportionally over following twenty-four months. This structure ensures founding team and early investors maintain aligned incentives rather than immediately selling positions after successful launch.

The inflation mechanism starting at five percent annually and decreasing half percentage point each year until reaching three percent floor balances need to compensate validators securing network against dilution concerns from token holders. Critically, inflation only activates when external validators and stake delegation launches, meaning controlled initial period prevents compounding supply increase during vulnerable early phase. The EIP-1559 inspired burn mechanism where base fees paid for transactions permanently remove XPL from circulation creates deflationary counter-force. If network usage grows sufficiently, fee burns could exceed inflation making net supply deflationary despite validator rewards. The mathematics only work if transaction volume justifies infrastructure costs, creating natural alignment where token value correlates with actual utilization rather than speculative narratives.

The community distributions demonstrated attention to avoiding concentration while rewarding participation. Twenty-five million XPL allocated to smaller depositors who completed Sonar verification and participated in public sale ensured even modest contributors received meaningful amounts. Additional two point five million XPL reserved for Stablecoin Collective members and contributors created ongoing incentive for community engagement beyond one-time token purchase. The Collective began as educational forum for building familiarity with stablecoins but evolved into community driving adoption and supporting broader ecosystem. Members could verify wallets through Discord to receive allocations recognizing that community-building work contributes value beyond capital investment. The philosophy treats token distribution as tool for aligning incentives across diverse stakeholder groups rather than purely extracting maximum capital from market.

The Day One DeFi Partnerships Creating Immediate Utility

The announcement that two billion dollars in stablecoins would be active on Plasma from mainnet beta launch with deployment across one hundred plus DeFi partners including Aave, Ethena, Fluid, and Euler represented months of coordination executed before any public blockchain operation. These weren’t vague partnership announcements but concrete integrations where protocols deployed smart contracts, provided liquidity, and prepared user interfaces for day one functionality. The strategic logic recognized that blockchain without applications remains technical demonstration rather than useful infrastructure. By ensuring immediate access to savings products preserving value, deep USDT markets enabling efficient trading, and lowest USDT borrow rates in industry supporting leverage and yield strategies, Plasma addressed cold start problem plaguing most new chains.

The Maple Finance partnership announced in September establishing institutional credit layer through syrupUSDT pre-deposit vault demonstrated sophistication beyond typical DeFi protocols. Maple’s focus on institutional-grade asset management and onchain credit markets meant sophisticated capital allocators treating Plasma as serious infrastructure rather than speculative playground. The collaboration strengthened onchain credit capabilities while seeding initial liquidity through structured products appealing to risk-conscious institutions rather than degenerate yield farmers. Yellow Card integration as leading stablecoin on-ramp and off-ramp in Africa alongside BiLira providing Turkish Lira-pegged stablecoin access established immediate geographic reach into key emerging markets where stablecoin adoption solves urgent problems rather than providing marginal improvements over existing banking.

The zero-fee USDT transfers enabled through app.plasma.to dashboard at launch provided immediate proof point that technical promises translated into actual user experience. The protocol-level paymaster sponsoring transactions meant users didn’t need hold native XPL tokens to move USDT, removing adoption friction where new users must first acquire unfamiliar asset before accessing desired functionality. The feature only works because close relationship with Tether ecosystem makes subsidizing USDT transfers strategically valuable for all parties. Tether benefits from infrastructure optimized for their stablecoin gaining adoption, Bitfinex profits from increased USDT usage flowing through their exchange, and Plasma attracts users by offering superior economics compared to alternatives charging fees. If it becomes standard that stablecoin transfers cost nothing on Plasma while competing chains charge even modest amounts, the cumulative advantage compounds over time as users optimize for lowest-cost rails.

The Regulatory Expansion Demonstrating Long-Term Commitment

The October twenty twenty-five announcement acquiring VASP-licensed entity in Italy and establishing Amsterdam office with compliance leadership signaled recognition that sustainable stablecoin infrastructure requires regulatory integration rather than offshore evasion. The Virtual Asset Service Provider license allows legally handling crypto transactions and custody assets in region under regulatory supervision. The Netherlands location choice reflected country’s established position as European payments hub where financial infrastructure benefits from sophisticated regulatory framework and deep talent pool. Adam Jacobs statement that growing team and regulatory presence provides path to own more of payments stack from stablecoin settlement to licensed financial infrastructure articulated vision where Plasma operates as regulated financial services provider rather than purely decentralized protocol.

The planned applications for Crypto Asset Service Provider status under EU’s MiCA regulation and Electronic Money Institution license represented substantial commitments requiring ongoing compliance costs, operational overhead, and regulatory scrutiny. These licenses enable exchanging assets, issuing cards, and holding customer funds under regulatory safeguards, functions that transform blockchain protocol into comprehensive financial services platform. Jacob Wittman’s emphasis on setting high standard for blockchain-native stablecoin infrastructure by securing right licenses and owning regulated stack end to end acknowledged that mainstream adoption requires meeting traditional finance expectations around consumer protection, operational transparency, and regulatory accountability. We’re seeing blockchain projects mature from libertarian ideals about regulatory resistance toward pragmatic recognition that operating at scale demands working within legal frameworks.

The strategy of owning fully licensed payments stack rather than relying on third-party providers addressed reliability and access concerns. When payment processor decides to terminate relationship with crypto company, the disruption can destroy months of progress building merchant relationships and user adoption. By controlling infrastructure from protocol layer through licensed payment rails, Plasma insulates itself from external dependencies that historically caused catastrophic failures for crypto businesses unable to maintain banking relationships. The approach requires substantially more capital, longer development timelines, and accepting regulatory constraints that purely decentralized protocols avoid, but potentially creates more defensible competitive position against both crypto alternatives and traditional payment networks.

Reflecting On Infrastructure Bets That Define Industry Evolution

The Plasma story illustrates how modern blockchain projects succeed or fail based on factors extending far beyond technical capabilities. The sophisticated token sale mechanics using Echo’s Sonar platform, the strategic team assembly bringing diverse expertise across payments and security, the structural integration with Tether ecosystem controlling majority of stablecoin market share, and the regulatory expansion into licensed European operations collectively represent infrastructure project rather than speculative token launch. The one billion dollars arriving in thirty minutes validated that sophisticated capital recognized distinction between genuine infrastructure plays addressing real friction and countless projects recycling existing ideas with marginal improvements.

The fundamental question remains whether stablecoins actually need purpose-built blockchain or whether existing infrastructure improves sufficiently that specialized optimization becomes unnecessary. Ethereum’s continued dominance with majority of stablecoin supply, TRON’s established position despite technical limitations, and Solana’s rapid adoption across DeFi applications suggest that general-purpose chains with network effects and developer ecosystems might maintain advantages outweighing Plasma’s focused optimization. The counter-argument holds that as stablecoin volumes grow from hundreds of billions toward trillions of dollars annually, even marginal efficiency improvements multiply into enormous value capture for infrastructure enabling cost savings.

The success metrics will emerge over years rather than months as network effects compound or fail to materialize. If it becomes reality that major financial institutions, payment processors, and emerging market users adopt Plasma as preferred stablecoin settlement layer, the early infrastructure investments and regulatory positioning create defensible moat. Alternative trajectory involves discovering that specialized blockchain for stablecoins solves problem nobody actually needed solved because existing solutions prove adequate with incremental improvements. The thirty-minute billion-dollar moment demonstrated market enthusiasm, but translating enthusiasm into sustained adoption requires executing flawlessly across technical infrastructure, regulatory compliance, partnership development, and community building simultaneously over extended period. The hardest part begins after mainnet launches when promises must transform into measurable results justifying extraordinary valuations and expectations.