The on-chain trading infrastructure competition is being fought on the wrong battlefield by almost every participant except one. Most Layer 1 projects approach the problem by asking how to make their general-purpose blockchain fast enough and cheap enough that trading applications can be built on top of it without creating a terrible user experience. This is the wrong question, because it assumes that trading is one application category among many and that the optimal architecture for a blockchain is one that serves all use cases reasonably well rather than one use case exceptionally well. asked @Fogo Official a different question from the beginning, which is what a blockchain would look like if it was designed exclusively for trading and everything else was treated as secondary or irrelevant, and that difference in framing produces architectural choices that cannot be replicated by chains that made different foundational decisions years ago.

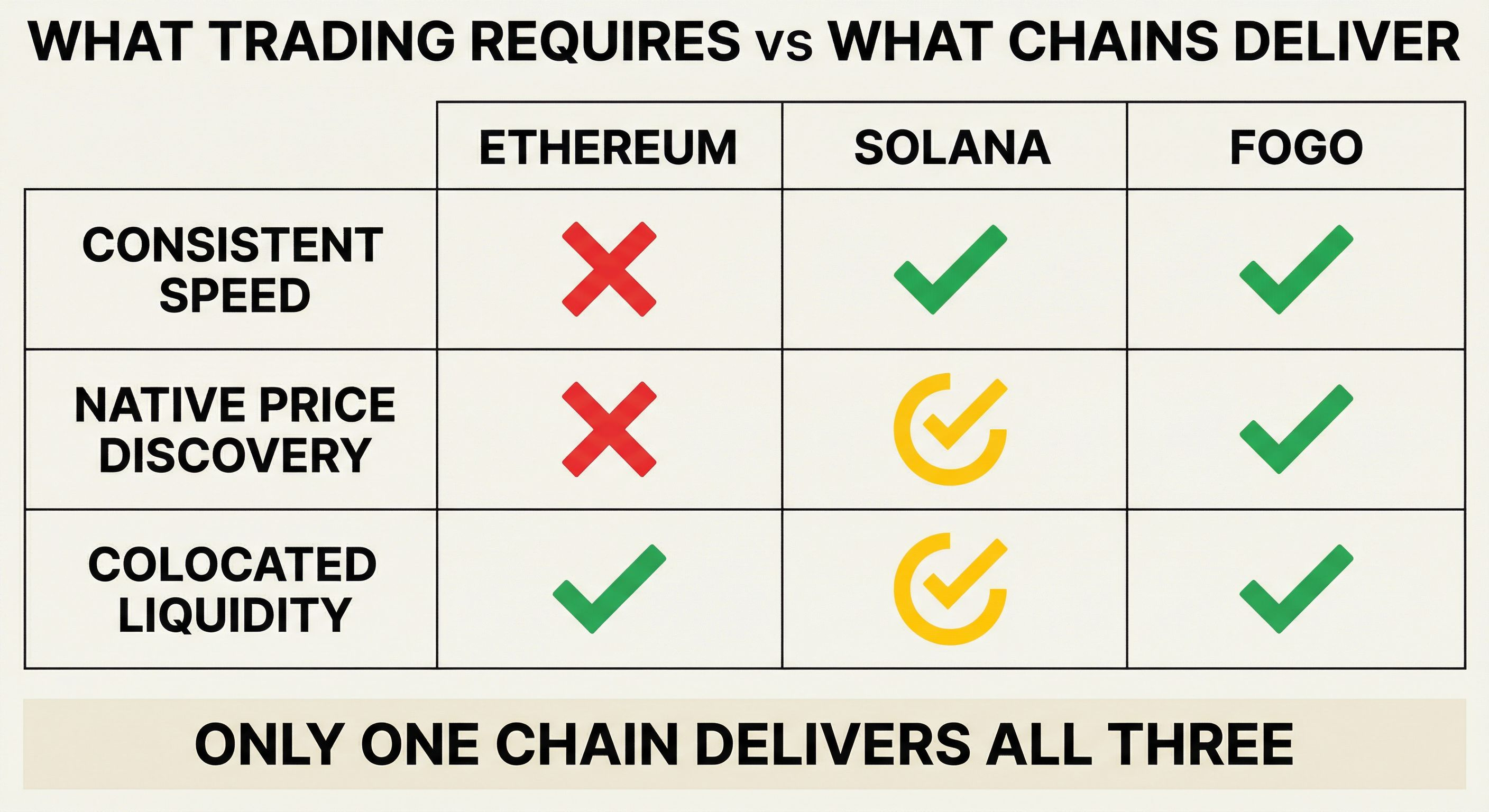

The clearest way to understand why this matters is to examine what trading actually requires from infrastructure and then evaluate which chains deliver those requirements and which chains merely claim to. Trading requires three things that sound simple but are structurally difficult to provide simultaneously. It requires speed that is consistent rather than merely high in ideal conditions, because a chain that processes 50,000 transactions per second when nobody is using it but degrades to 500 transactions per second under load is not a trading venue, it is a demonstration environment that fails when it matters most. It requires price discovery mechanisms that operate at chain speed rather than at oracle speed, because every millisecond of lag between real market conditions and the price feed that applications rely on is a millisecond of exploitable arbitrage that costs traders money. It requires liquidity that is deep and colocated rather than fragmented across independent pools, because fragmented liquidity means worse execution quality even when the underlying chain is fast.

Most chains deliver one of these requirements reasonably well and fail at the other two. Ethereum delivers deep liquidity and robust price discovery through mature DeFi applications, but it does not deliver consistent speed because the base layer was never designed to prioritize low latency execution and every scaling solution built on top of it inherits that limitation. Solana delivers impressive speed in ideal conditions and has made meaningful progress on application ecosystem development, but it does not deliver the kind of deterministic performance under stress that institutional market makers require before committing serious capital, and the distinction between peak performance and reliable performance is the distinction between a chain that hosts trading activity and a chain that becomes essential trading infrastructure.

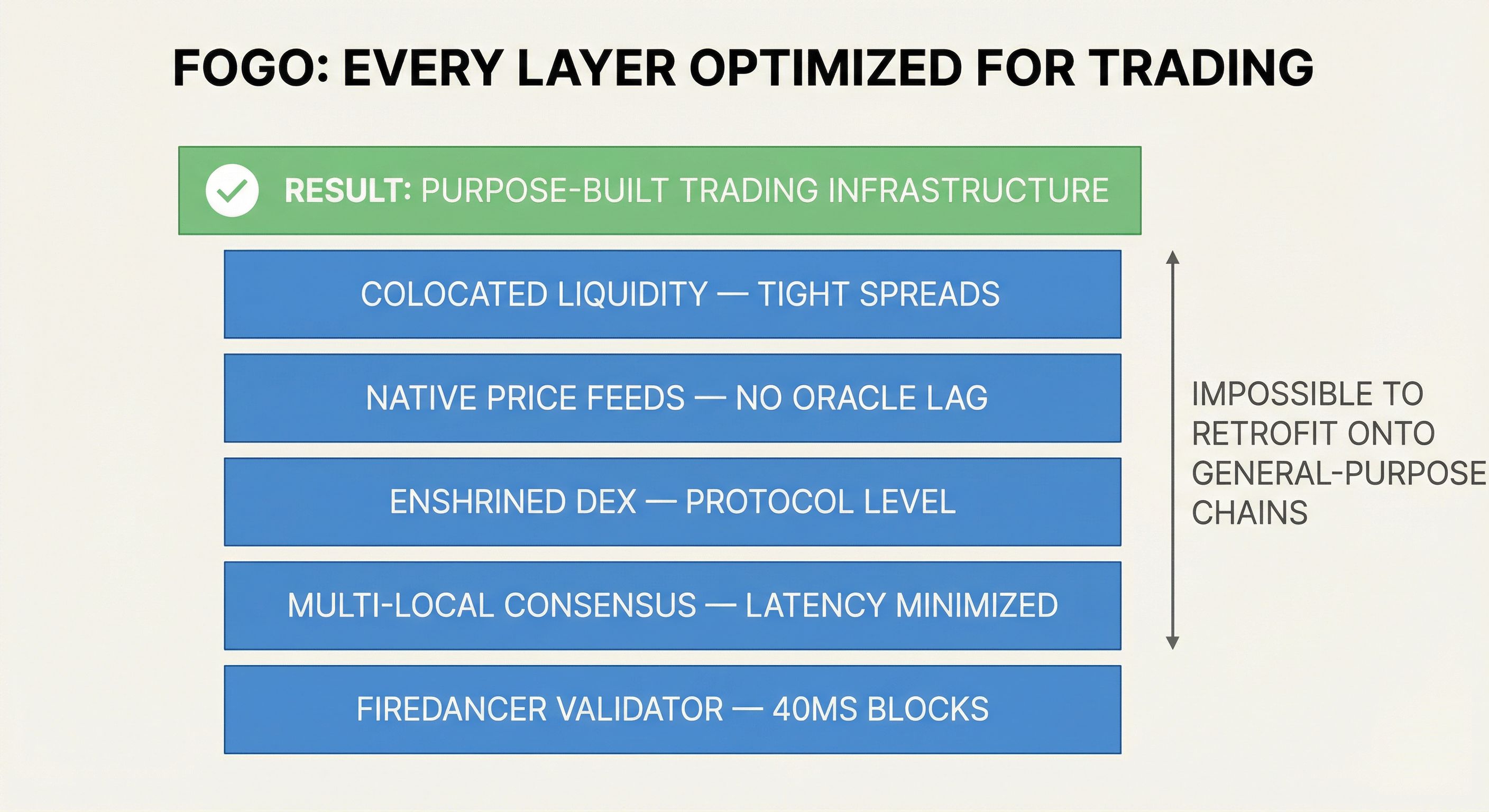

The architectural choices that $FOGO made are visible in every layer of the system and they are choices that competing chains cannot replicate without starting over. The decision to target 40 millisecond blocks rather than optimizing for maximum theoretical throughput is a bet that predictable cadence matters more than peak numbers, and that bet is correct for trading workloads even though it sounds conservative compared to projects claiming 100,000 transactions per second in controlled benchmarks. A 40 millisecond block time with near-zero variance in block production is more valuable to a market maker updating quotes than a 10 millisecond average block time that occasionally spikes to 500 milliseconds when network conditions deteriorate, because the variance is what makes reliable quoting impossible and forces market makers to quote wider spreads to protect against execution uncertainty.

The decision to enshrine the DEX at the protocol level rather than treating it as an application that lives on top of the chain is a bet that eliminating the gap between price discovery and execution matters more than maintaining clean separation of concerns in the architecture, and that bet is correct for the same reason. When the DEX is part of the protocol, price feeds are native to the chain state rather than being imported from external oracles with their own latency characteristics and their own potential points of failure. This means the price that an application sees when it queries the chain is the price that reflects the actual state of the order book at that moment rather than the price that an oracle happened to report 200 milliseconds ago, and in fast-moving markets that 200 millisecond difference is the difference between fair liquidations and unfair liquidations, between tight spreads and wide spreads, between a venue that traders trust and a venue that traders use reluctantly because better options do not exist yet.

The decision to build on Firedancer and to colocate validators in zones rather than distributing them globally for the sake of decentralization theater is a bet that removing network latency at the infrastructure layer matters more than optimizing for a perfect decentralization checklist, and that bet is correct because decentralization that comes at the cost of execution quality produces a system that is decentralized in theory but unused in practice. Collocating validators does not mean the chain is centralized. It means the validators are physically positioned to minimize the speed-of-light latency that cannot be eliminated through software optimization, and when the goal is to build the fastest possible execution environment for trading, every millisecond of latency that can be removed through operational discipline should be removed even if it requires making coordination decisions that sound less philosophically pure than a perfectly distributed validator set.

The competitive moat that these choices create is not the kind of moat that shows up in a feature comparison chart, because a feature comparison chart evaluates chains based on whether they have smart contracts, whether they support popular wallets, whether they have a bridge to Ethereum, and a dozen other dimensions that are necessary but not sufficient for building serious trading infrastructure. The moat appears when you evaluate chains based on whether a market maker can reliably update their quotes every 40 milliseconds without worrying about missed blocks, whether an arbitrageur can trust that the price they see is the price they will receive when the transaction confirms 1.3 seconds later, whether a leveraged trader can trust that their liquidation will be triggered at the price the market actually traded at rather than at a stale oracle price that lagged reality by several seconds.

The honest acknowledgment that prevents this analysis from being purely celebratory is that having the best architecture for trading does not guarantee market dominance, because markets are not won purely on technical merit. Network effects matter. Liquidity attracts liquidity, and overcoming existing liquidity moats requires either a substantial technical advantage that traders notice immediately or a long period of consistent execution quality that gradually builds trust and shifts behavior. @Fogo Official has the technical advantage. Whether that advantage is substantial enough to shift behavior at the scale required to challenge chains with years of accumulated liquidity and ecosystem development is the variable that will determine whether the project succeeds in capturing meaningful trading volume or remains a well-architected chain with a small but loyal user base that understands what they have but cannot convince the broader market to move.

What differentiates Fogo from the many other projects that have launched with bold claims and strong technical foundations is the specificity of the choices and the coherence of the overall design. This is not a chain that added a high-speed trading mode as an afterthought to a general-purpose architecture. This is not a chain that launched fast and will figure out the trading-specific optimizations later if demand materializes. This is a chain where every architectural decision from the validator client selection to the consensus mechanism to the liquidity layer design was made through the lens of what trading infrastructure actually requires, and the result is a system where the parts fit together in a way that produces advantages that cannot be replicated by bolting trading features onto a chain that was designed for a different purpose.

The comparison that matters is not between Fogo and Ethereum or between Fogo and Solana in the abstract. The comparison that matters is between the experience of executing a trade on @Fogo Official and the experience of executing the same trade on any other chain under real market conditions with real capital at risk. Does the transaction confirm at the price you expected. Does the confirmation happen quickly enough that the market has not moved meaningfully between submission and execution. Does the liquidity depth support the size of the trade you want to make without causing unacceptable slippage. Does the system remain stable and predictable when volatility spikes and every trader is trying to execute simultaneously.

These are the questions that determine whether a chain becomes essential infrastructure for trading or remains an interesting technical experiment, and these are the questions where $FOGO's architectural choices produce answers that other chains cannot match without rebuilding from the foundation. The battle for on-chain trading dominance will not be won by the chain with the highest theoretical throughput or the most impressive decentralization score on a governance checklist. It will be won by the chain that traders choose to trust with their capital because the execution quality is better, the reliability is higher, and the structural advantages compound with every trade in ways that make switching back to slower infrastructure feel like an unacceptable downgrade.

That chain is being built right now. The architecture is live. The choices have been made. What remains to be determined is whether the market recognizes what has been built before the window of opportunity closes and whether the traders who understand the difference arrive in numbers large enough to create the network effects that make the technical advantage permanent rather than temporary.