Grok-4 Heavy scored 0.5 on Humanity's Last Exam in late 2025, a benchmark created to be "the final closed-ended academic test for non-biological computers." Ten months earlier, similar AI systems were scoring barely 0.1. Performance improved five-fold in less than a year, and this capability jump is not slowing down. When you combine AI cognition that improves this rapidly with robots that can share skills instantaneously across unlimited hardware, you create economic dynamics that do not exist in traditional industries where capabilities scale gradually and where geographic and human resource constraints create natural limits on how fast any single competitor can expand. @Fabric Foundation published their whitepaper in December 2025 with a section titled "Risk of Winner Takes All" that most readers probably skimmed past because it sounds like generic startup concern-mongering about competitive moats. It is not. It is a description of the structural economic forces that make robotics fundamentally different from every other technology wave, and understanding why those forces push toward extreme concentration unless architecture specifically prevents it is necessary for evaluating whether open protocols like $ROBO matter or whether they are just philosophical preferences about governance models that do not affect actual outcomes.

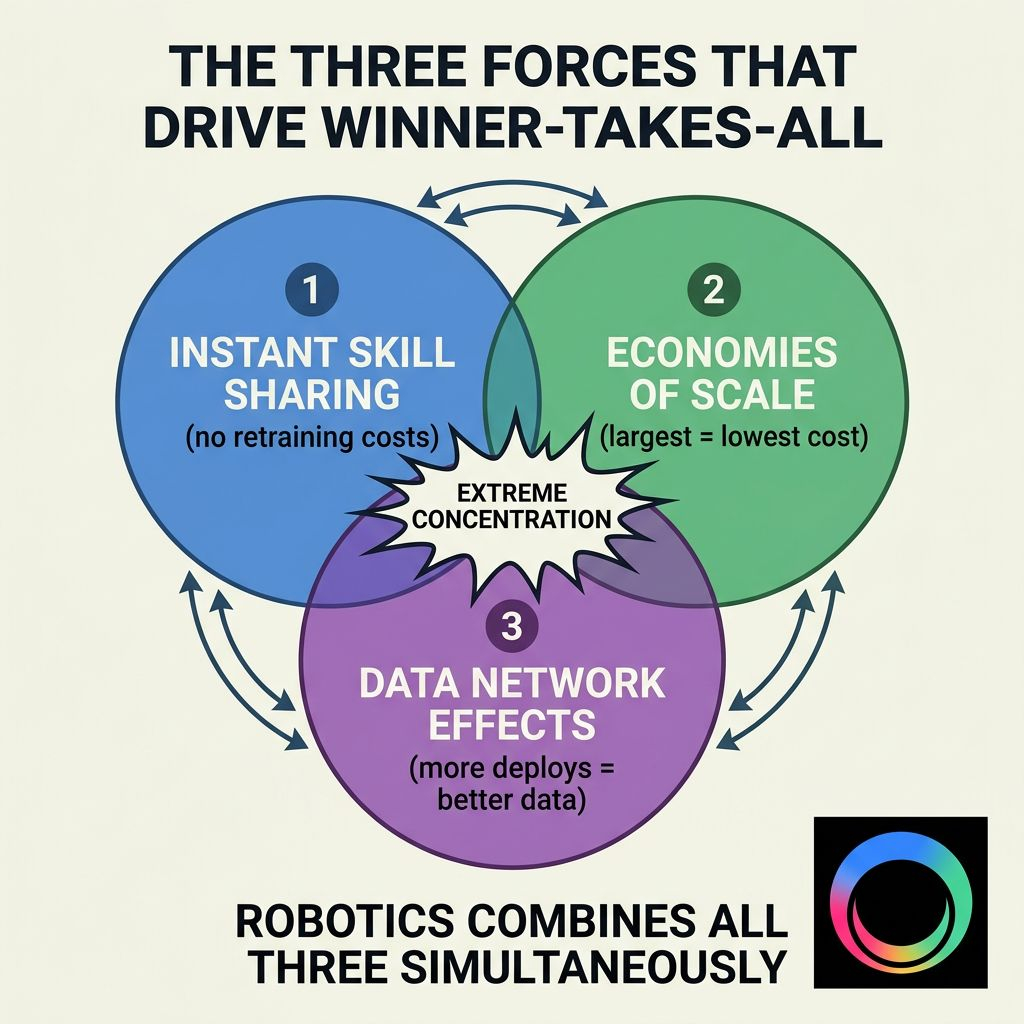

The winner-takes-all dynamic in robotics emerges from three compounding factors that reinforce each other: instant skill sharing that eliminates retraining costs when adding new capabilities, economies of scale that make the largest operator the lowest-cost operator, and data network effects where more deployments generate better training data which improves all existing skills which attracts more deployments. None of these factors exist in isolation in traditional industries. Manufacturing has economies of scale but not instant capability transfer across all units. Software has network effects but not physical presence in every geography. Service businesses have skills but those skills are locked in individual human workers who cannot share knowledge instantaneously. Robotics combines all three factors simultaneously, and when you model what that combination produces mathematically, the equilibrium is not multiple competitors coexisting indefinitely. The equilibrium is one dominant operator that controls enough of the market that challengers cannot achieve comparable unit economics or training data quality.

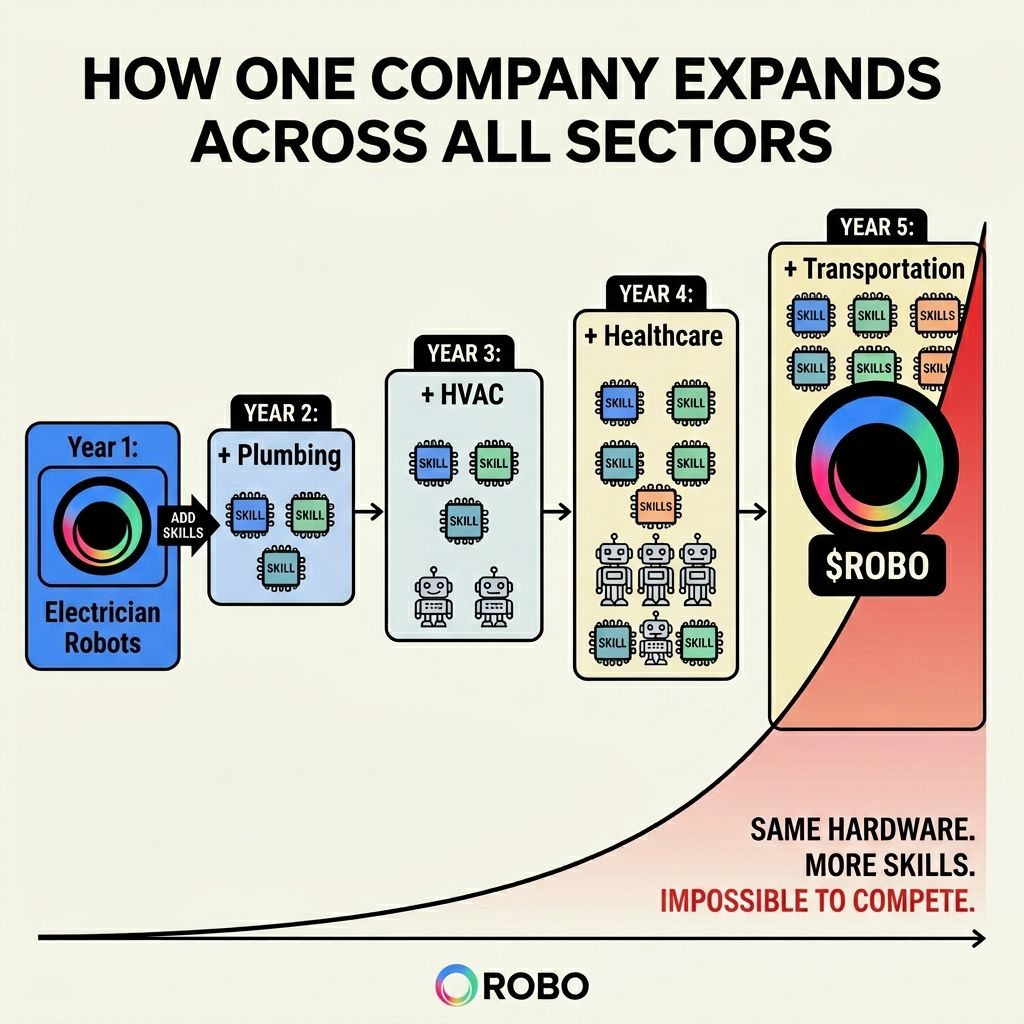

Consider how this plays out with a specific example from the whitepaper: electrician robots that master California Electrical Code and can be deployed at $3-12 per hour compared to human electricians earning $63.50 per hour. The first company to bring electrician robots to market captures the California electrical work market because customers prefer lower costs and more consistent quality. That company now has 23,000 robots deployed across California generating training data about edge cases, error modes, and customer preferences that robots operating in controlled test environments cannot generate. This training data improves the electrical skill performance for all 23,000 robots simultaneously through the shared learning system, which makes the company's offering even more attractive compared to human electricians or competing robot systems that lack equivalent deployment scale.

Now the company faces a strategic choice: continue focusing exclusively on electrical work or add additional skills to the same hardware platform. Adding plumbing skills to electrician robots costs far less than deploying an entirely new plumbing robot fleet because the hardware already exists and the locomotion, manipulation, and safety systems are already trained. The company adds plumbing skills through a software update. Now 23,000 robots can perform both electrical and plumbing work, which means the company can offer bundled services at lower prices than specialists who only do one type of work. Customers prefer bundled providers because coordination is easier and total cost is lower. The company captures the plumbing market in California.

The pattern continues across every skill that can be added to general-purpose robots. HVAC requires similar hardware and many of the same base competencies as electrical and plumbing work, so the company adds HVAC skills. Now they operate across three verticals with the same hardware fleet. Surgical assistance requires different end effectors but similar precision and safety systems, so the company branches into healthcare. Autonomous transportation uses different form factors but shares the navigation and safety algorithms, so the company expands into logistics. At each step, the company with the largest deployed fleet has better training data, lower unit costs, and faster capability development than competitors who are trying to enter individual verticals without the scale advantages that come from operating across multiple markets simultaneously.

The Fabric Protocol whitepaper describes this trajectory as "winner takes all" and notes specifically that "the first company (or country) to bring this technology to market could quickly control entire swaths of the global economy." This is not fearmongering about hypothetical scenarios. This is a straightforward extrapolation from the technical characteristics of skill-sharing machines combined with the economic incentives that drive company behavior when no structural constraints prevent concentration. A company that reaches product-market fit first in one vertical can expand faster than new competitors can establish themselves because each new skill makes the existing platform more valuable and generates more data that improves all capabilities simultaneously.

The only mechanism that changes this trajectory is architecture that makes skills, training data, and robot capabilities coordinate through open protocols rather than through proprietary platforms controlled by single entities. This is what $ROBO implements through three specific design choices that closed platforms cannot replicate without abandoning the business models that make them attractive to investors who expect concentrated ownership and monopoly-level returns.

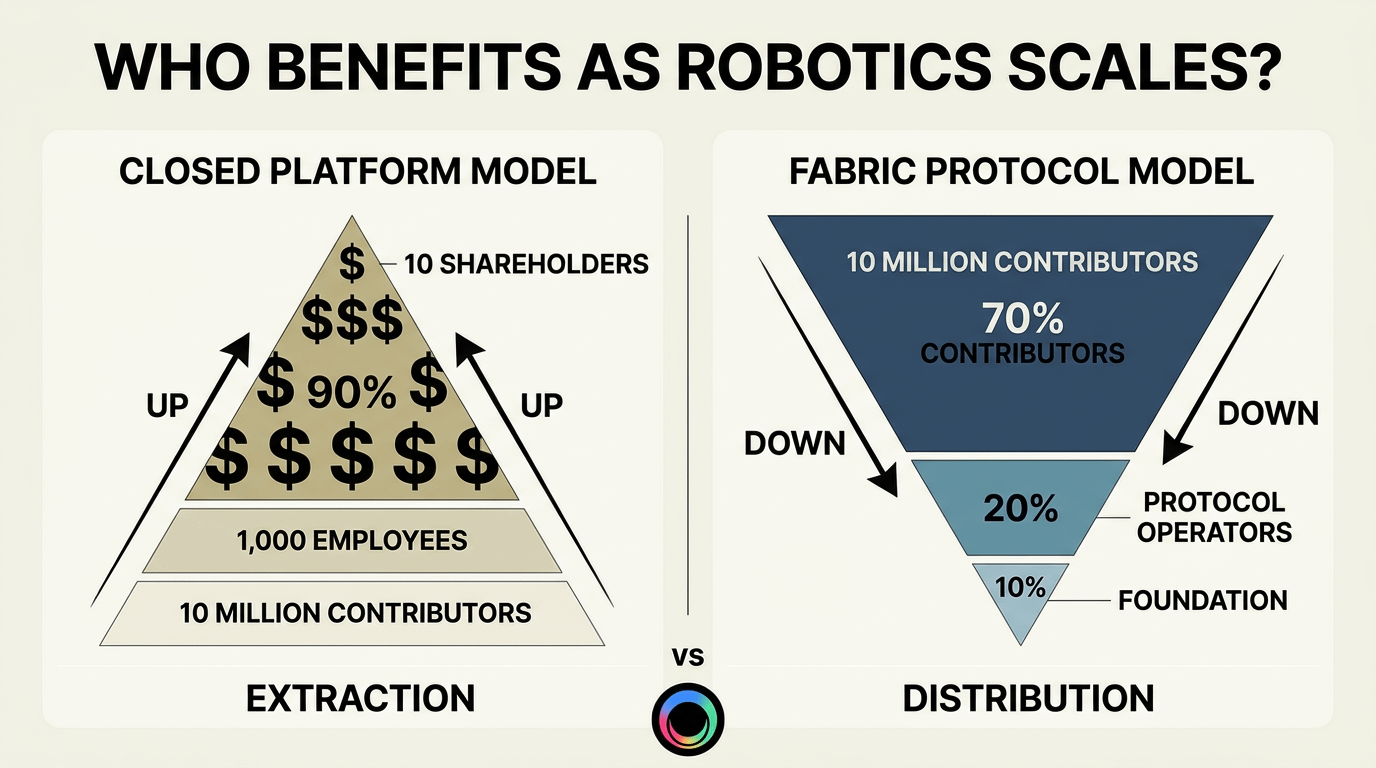

FIRST: Skill chips as open modules verified through public ledgers rather than as proprietary capabilities controlled by platform operators. When electrical skills exist as open modules that anyone can contribute to, train, and improve, the training data and capability improvements flow to the contributors who created them rather than accumulating exclusively in the company that operates the platform. This prevents the data moat from developing because the contributors who improve skills own the improvements and can move those skills to different hardware platforms if the original platform operator tries to extract monopoly rents. The economic incentive that drives winner-takes-all concentration—the accumulation of training data that competitors cannot match—is eliminated when training data is contributed openly and improvements are owned by contributors rather than by platform operators.

SECOND: Public ledger coordination of which skills exist, how they perform, and what they cost, rather than opaque platform control where the operator decides what gets built and what gets deployed. In closed platforms, the operator makes prioritization decisions based on which capabilities generate the most revenue or lock in the most users, which means capabilities that serve concentrated corporate customers get built before capabilities that serve distributed individual users or underserved markets. In open protocols coordinated through public ledgers, any contributor can build and deploy skills that they believe are valuable, and users vote with their attention and their payments rather than being limited to what the platform operator chose to prioritize. This prevents the concentration of control over which capabilities robots acquire and ensures that the skill development roadmap serves the ecosystem rather than serving the platform operator's revenue optimization goals.

THIRD: Fractional ownership distributed to contributors rather than concentrated equity owned by founders and investors. When people who train skills, improve robot performance, secure the network, and provide deployment infrastructure earn fractional ownership through the protocol, the economic value that would flow to one company in a closed system gets distributed across all participants who contributed to creating that value. This does not eliminate economies of scale or network effects, but it does change who benefits from those dynamics. In a closed system, scale and network effects concentrate wealth in the company that owns the platform. In @Fabric Foundation 's open system, scale and network effects increase the value of fractional ownership held by contributors, which means more people benefit as the system grows rather than wealth concentrating in fewer hands.

The honest assessment that makes this analysis credible rather than promotional is that preventing winner-takes-all concentration through architecture comes with real costs that closed platforms do not have to bear. Coordinating skill development through public ledgers is slower than having a product team make decisions internally. Verifying contributions and distributing ownership requires computational overhead and governance processes that centralized companies can skip. Allowing anyone to contribute skills creates quality control challenges that do not exist when one company controls what gets deployed. These costs are not trivial, and they explain why many successful technology platforms have used closed architectures even when those architectures create the concentration problems described here.

What makes those costs worth paying in robotics specifically is that the consequences of winner-takes-all concentration in robotics are more severe than in almost any other technology domain. When one company controls social media, users have worse experiences and less choice, but the direct physical harm is contained. When one company controls email, communication becomes less open, but competitors can still operate and users can still switch. When one company controls the robots that perform essential work across manufacturing, healthcare, education, transportation, and daily life, the concentration of control affects physical safety, economic opportunity, and political power at scales that threaten the social stability that functional societies depend on.

The whitepaper cites the example of taxi driving serving as "the first step towards the American dream, allowing humans with basic skills (a valid driver's license) to earn a regular income and feed their children" for the past 100 years. Waymo autonomous vehicles now demonstrate 8-fold fewer accidents than human-driven vehicles, which means the safer choice for parents sending children to school is the autonomous vehicle rather than the human-driven taxi. This displacement is happening regardless of governance models or political interventions because the performance and safety differences are measurable and the economic advantages are substantial. But whether that displacement concentrates wealth in one company that owns the autonomous vehicle platform or distributes economic participation across contributors who helped train the navigation systems and improve the safety algorithms depends entirely on whether the infrastructure is open or closed.

Extrapolating from taxis to every occupation that robots can potentially perform at lower cost, higher quality, or better safety creates a future where either one company (or a small number of companies, or one country) controls the infrastructure that performs most work, or where that infrastructure is open and the economic value flows to the distributed network of contributors who made it possible. The first future produces concentration of power and wealth at levels that historical examples suggest are politically unstable and socially destructive. The second future produces broad economic participation where improvements to the robot capabilities benefit the people who contributed to those improvements rather than benefiting exclusively the entity that happened to deploy first.

The critical window for determining which future emerges is not after robots become ubiquitous and the network effects are locked in. The critical window is now, while the technology is still in the phase where multiple architectural approaches are viable and where the costs of migration from one approach to another are still manageable. Once winner-takes-all dynamics establish themselves through closed platform deployment at scale, the switching costs become prohibitive and the concentrated operator has both the incentive and the resources to prevent competitors from gaining traction. Platform operators use their advantages to make their platforms stickier through proprietary protocols, exclusive partnerships, and strategic acquisitions of potential competitors before those competitors reach scale.

@FabricFoundation launching in late 2025 with open protocol architecture is strategically significant not because open protocols are philosophically preferable to closed platforms (though many people have preferences about governance models) but because open protocols implemented before concentration locks in can prevent concentration from occurring at all. The electrician robots and taxi replacements that the whitepaper discusses as examples are not distant future scenarios. Waymo is already operating at scale in multiple cities. Electrician robots are in commercial pilot deployments. The timeline from "interesting demonstration" to "controls significant market share" in robotics appears to be measured in years rather than decades, which means the architectural choices being made in 2026 will determine whether robotics infrastructure remains open and distributed or whether it concentrates in ways that cannot be reversed once network effects establish themselves.

The builders, contributors, and early adopters choosing $ROBO today are not making a bet about which protocol has better marketing or which team has stronger venture backing. They are making a bet about whether winner-takes-all concentration in robotics can be prevented through architecture, and whether preventing that concentration matters enough to accept the coordination costs and governance overhead that open protocols require. The companies choosing closed platforms are making the opposite bet: that the efficiency advantages of centralized control and the investor returns from concentrated ownership are more important than preventing the social and economic consequences of one entity controlling essential infrastructure that affects every person's livelihood and safety.

Both bets will be resolved by observable outcomes rather than by philosophical arguments. If open protocols can attract enough contributors and deployment scale to compete with closed platforms on capability and cost while maintaining distributed ownership and transparent governance, the prevention of concentration will be demonstrated empirically. If closed platforms achieve sufficient scale advantages that open protocols cannot match their training data quality or their unit economics, the winner-takes-all dynamic will prove to be structurally inevitable regardless of architectural alternatives. The distinguishing characteristic of this moment in early 2026 is that both outcomes are still possible and the choices being made now determine which equilibrium the robotics industry reaches.

The whitepaper's section on winner-takes-all risk is three paragraphs in a technical document mostly focused on genome-inspired architectures and skill chip modularity. But those three paragraphs describe the most important economic question about the next decade of robotics deployment: whether the first company to master general-purpose robots will control the global economy, or whether the architecture that enables general-purpose robots will prevent any single entity from achieving that control. @Fabric Foundation is a bet on the second outcome, built with specific protocol choices designed to make concentration architecturally infeasible rather than merely discouraged through governance preferences that can be ignored when concentration becomes profitable.

#ROBO @Fabric Foundation $ROBO