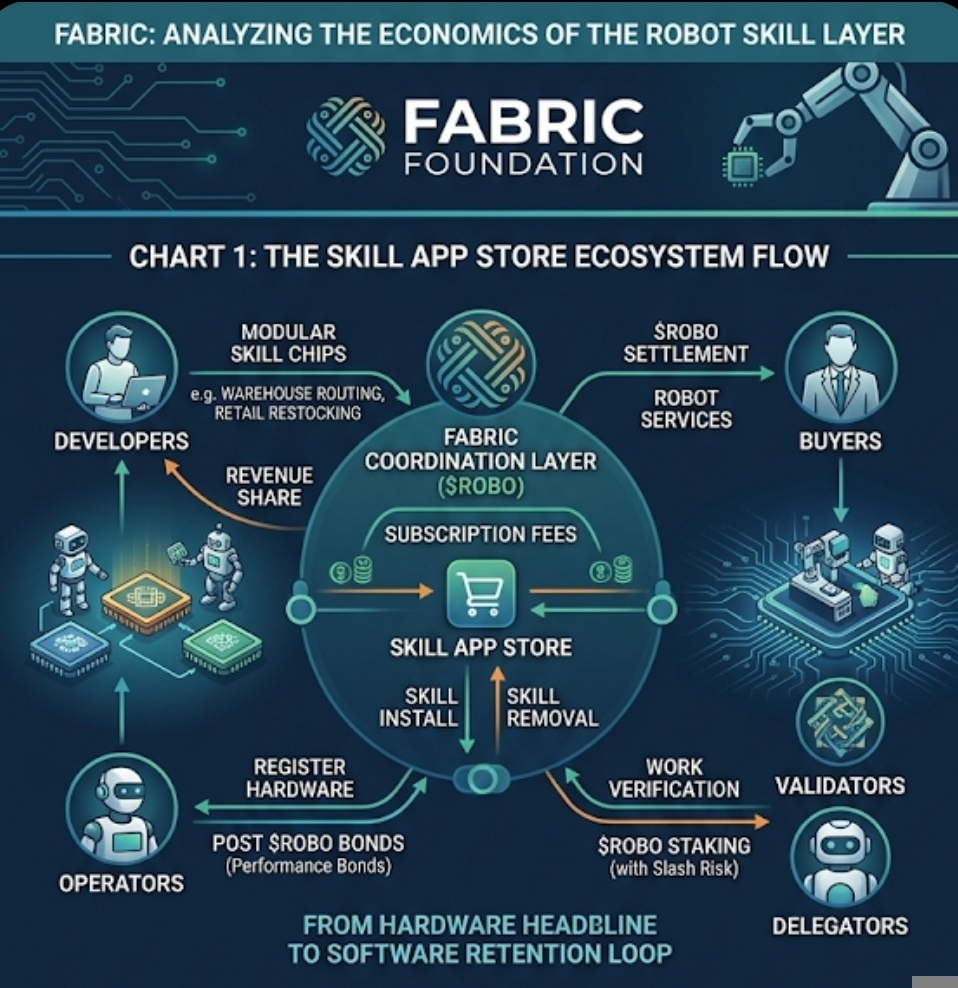

I remember the first time I started looking seriously at robot networks as token trades. My instinct was to treat them the same way the market usually does: find the hardware story, find the AI angle, check the float, then decide whether the chart is just another attention cycle wearing industrial clothing. That was the easy framework. What caught my attention with Fabric was something smaller and, honestly, a bit less flashy. Buried in the whitepaper was the idea of a robot skill app store, where modular “skill chips” can be installed and removed like phone apps, with subscription-style fees attached to usage. At first I assumed that was just branding. Over time that started to look different. It is not the robot that may become the recurring economic unit here. It may be the skill layer sitting on top of it.

That matters because markets usually overprice the hardware headline and underprice the software retention loop. A robot sold once is a capital event. A robot that keeps pulling paid skills into its stack is a demand loop. Those are very different things. Fabric is describing a network where robots, operators, developers, validators, delegators, and buyers all interact through a tokenized coordination layer, with $ROBO used for settlement and for posting operational bonds. The economic pitch is not just “robots onchain.” It is that work, verification, and access can all be tied back to one unit of settlement, and that fees generated by usage can feed demand for that unit over time. A portion of protocol revenue may even be used to acquire $ROBO on the open market, which is the kind of detail traders notice because it shifts the conversation away from pure emissions and toward actual supply absorption.

This is where I think the market misses something. Most people hear “app store” and think distribution. I hear pricing power and modular monetization. If a robot can load a warehouse routing skill this month, a retail restocking skill next month, and then remove both when they stop being useful, the economic center of gravity starts moving from the base machine to the recurring software layer. Fabric’s own framing is explicit here: skill chips can be added and removed, and subscription fees stop when the skill is no longer needed. That is a much cleaner revenue model than the usual token narrative around vague future adoption. It gives you something closer to usage-based infrastructure. Not guaranteed demand, but at least a mechanism that could produce it.

Mechanically, the system is more serious than the surface narrative suggests. Operators stake ROBO as performance bonds to register hardware and take work. Those bonds scale with declared capacity. Buyers use the network for robot services and settlement. Validators and challenge mechanisms are supposed to verify whether work was actually done and whether quality stayed above threshold. Delegators can augment operator bonds, which lets capacity scale faster, but they also inherit slash risk. That part is important. It means capital is not just passively parked; it is underwriting execution quality. If the operator fails, the capital behind them can get hit. In theory, that produces a more honest market for reputation than simple token staking because bad performance has a cost. In practice, it also creates a new question: how strong is the verification layer really when work leaves the clean world of digital compute and enters physical reality?

That is probably the biggest practical risk in the whole model. An app store for robot skills only works if the network can tell the difference between genuine execution and performative telemetry. Spoofed activity is the obvious failure mode. Low-quality operators can also slip through if the validation process is weak, especially early when the network is hungry for growth and tempted to accept noisy participation. Fabric’s whitepaper lays out slashing for fraud, downtime, and quality degradation, including penalties tied to uptime and service quality. That is directionally right. Still, slashing frameworks always look cleaner in a document than they do in a real market where sensors fail, humans intervene, logs can be gamed, and quality is often subjective at the margins.

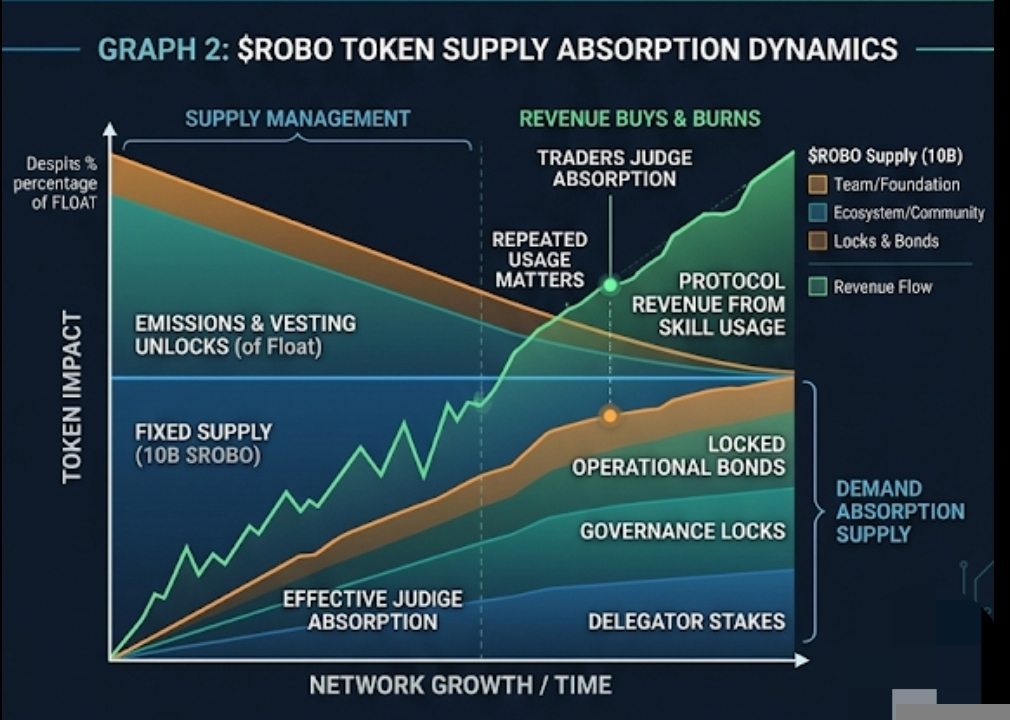

Then there is the token itself, which I would not ignore just because the concept is interesting. The total supply is fixed at 10 billion $ROBO. Investors hold 24.3%, team and advisors 20%, foundation reserve 18%, ecosystem and community 29.7%, with smaller allocations for airdrops, liquidity provisioning, and the public sale. That immediately tells me this will be a supply-discipline story as much as a robotics story. A big fixed supply is not fatal. Plenty of infrastructure tokens survive that. But the market will care about float quality, vesting rhythm, and whether real lockups through bonds and governance can offset emissions and unlocks. Fabric at least tries to address this structurally: circulating supply is modeled as vested supply minus locked bonds and governance locks, minus burns, plus emissions, minus buybacks. In other words, the project is openly admitting that usage has to absorb supply or the narrative will outrun the economics. Good. It should be judged that way.

The retention problem sits right in the middle of all this. Developers do not keep building robot skills because the whitepaper sounds ambitious. They keep building if there is recurring installation demand, revenue share, and enough distribution to make the next skill worth shipping. Operators stay if task flow is steady and the cost of bonding capital is justified by service income. Buyers stay if the robot service is cheaper, more reliable, or easier to scale than existing alternatives. Delegators stay if slash-adjusted returns make sense. Validators stay if verification rewards are worth the work. That is the loop. If even one side drops out, the app store thesis gets weaker. An app store with no paying installs is just a catalog. A token with no repeated service demand is just float looking for a story.

From a trader’s perspective, I would get more constructive if I saw a few specific behaviors emerge. First, actual repeated usage rather than one-off pilot announcements. Second, evidence that operators are bonding meaningful amounts of $ROBO relative to capacity, which would tell me the token is becoming operational collateral instead of just speculative inventory. Third, signs that protocol revenue is real enough for fee conversion and open-market purchases to matter at the margin. And fourth, some proof that skills are becoming reusable economic objects across machines or deployments, because that is the part that turns this from “robot network” into something closer to an asset platform. If the story gets cleaner while the evidence stays thin, I get cautious. I have seen that movie too many times.

So I do think the market may be underpricing one part of Fabric. Not the robot dream. Not the usual AI headline. The more interesting possibility is that modular robot skills become recurring economic units, and that the network coordinating them starts to look less like a hardware experiment and more like a marketplace with software-like margins. Maybe. But that only matters if behavior confirms it. Traders should watch installs, fees, bonded participation, and repeat usage. Narratives are cheap. Retention is the real chart.