I remember the first time I saw a robotics token start to attract real trading attention, and what caught my attention was not the chart strength. It was the speed with which the market skipped past the hard part. People were talking as if robot scale was mostly a hardware problem, maybe a model problem, maybe a deployment problem. Over time that started to look different to me. In crypto, systems usually fail earlier than that. They fail at the level of coordination, incentives, verification, settlement, and trust. That is why Fabric looks more interesting to me as an institutional bet than a pure robotics bet. Their own framing is not really “we have robots, now number go up.” It is much closer to “today’s institutions and economic rails were not designed for machine participation,” which is a very different trade.

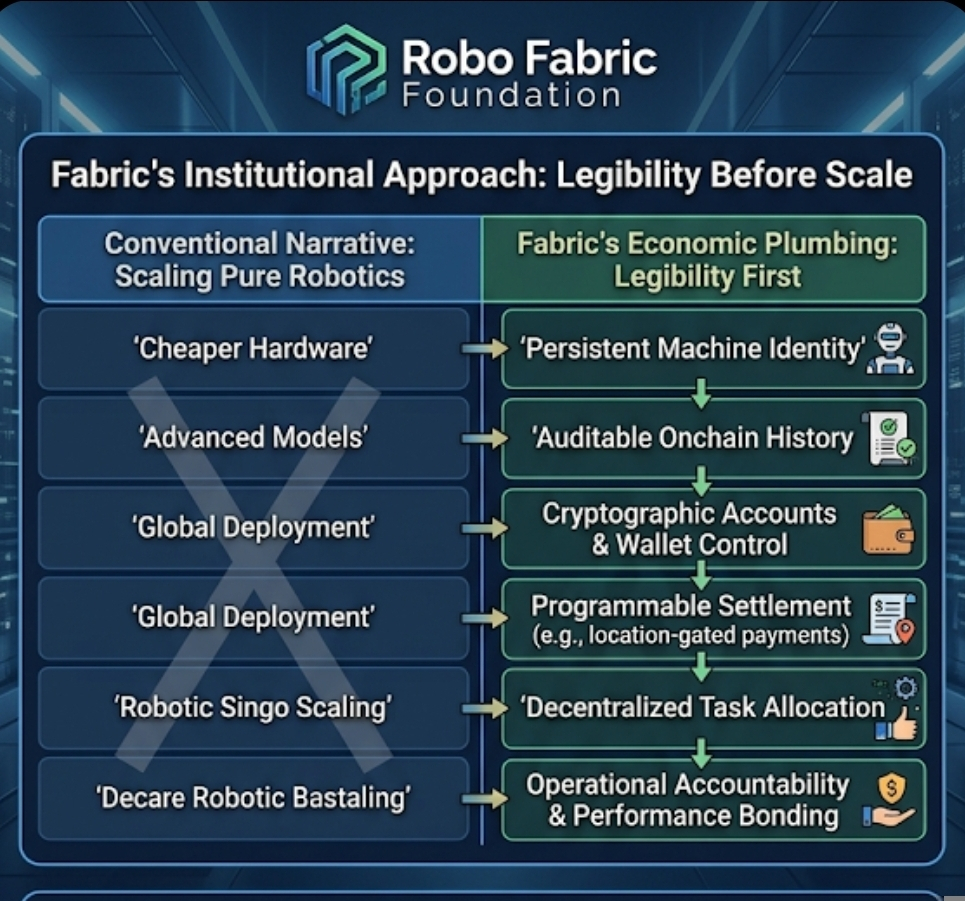

This is where I think the market misses something. A lot of people hear “robot economy” and instinctively picture more machines in more places. Fair enough. But Fabric keeps pointing to identity, accountability, payments, task allocation, tele-operations, and long-term stewardship. In other words, the stuff that makes an economy legible before it makes it large. The homepage is unusually explicit about that. It talks about machine and human identity, decentralized task allocation and accountability, location-gated and human-gated payments, and participation from people across regions through tele-operations and local customization. That is not a scale-first story. It is an institution-first story. The bet is that robots do not become meaningful economic actors just because the hardware gets cheaper. They become meaningful when someone can verify who they are, what they are allowed to do, how they get paid, who is responsible when they fail, and how outside participants can coordinate around them without trusting a single closed operator.

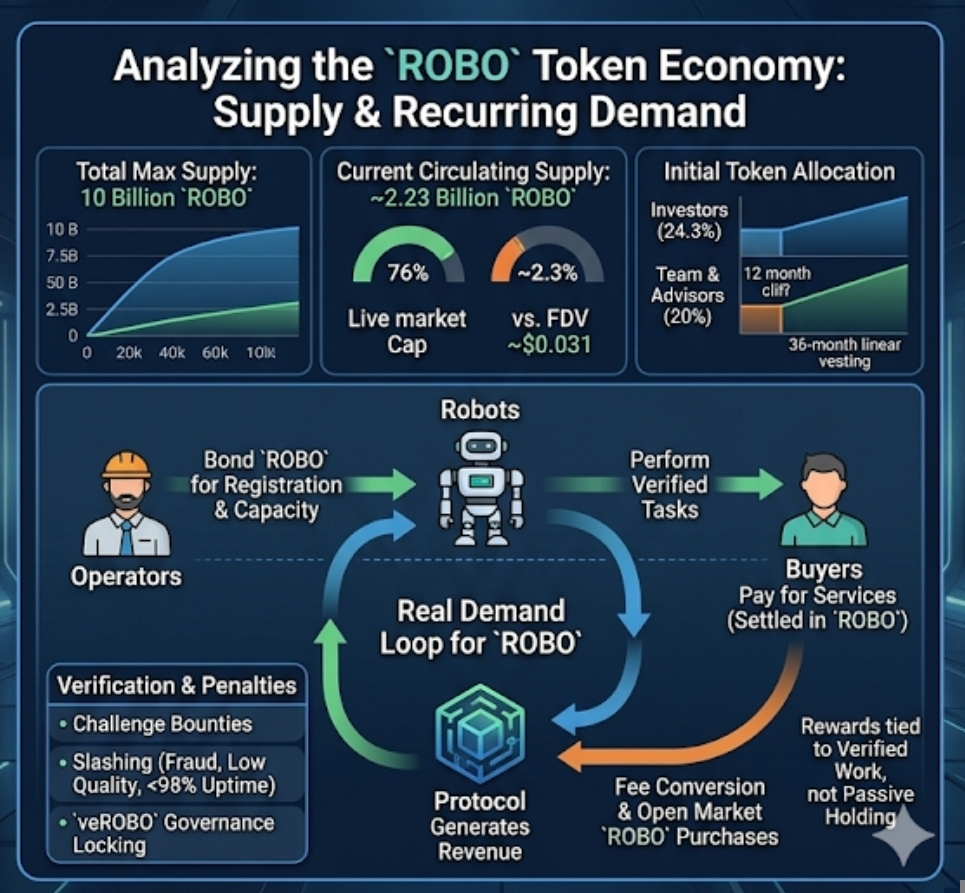

Once I looked at the token design, that interpretation made even more sense. The white paper describes ROBO less like a generic speculative asset and more like a network permission layer. Operators post refundable performance bonds in ROBO to register hardware and provide services, with bond size scaling against declared capacity. Fees for data exchange, compute tasks, and API calls can be quoted in stable-value terms, but final settlement still happens in ROBO. Holders can also lock tokens into veROBO for governance signaling, while revenue can be partially converted into open-market ROBO purchases. That package matters because it ties the token to operational roles rather than just community mood. Not perfectly, but more seriously than most launch-era AI coins I see.

At first I assumed this was just another bond-and-burn diagram dressed up in robot language. Then I noticed the more practical parts. Fabric says robots need persistent identity, wallets, and standardized participation rights. A robot in a warehouse or delivery network is supposed to have an auditable onchain history, cryptographic control over accounts, and programmable settlement for services like compute, maintenance, and insurance. That sounds abstract until you reduce it to operations. Imagine a delivery robot that completes tasks in a zone where payment permissions are location-gated and some activities require human gating. The network does not only need the robot to function. It needs the robot to be known, bonded, monitored, paid, and challengeable. That is much closer to institutional plumbing than to a clean consumer app story.

From a trader’s perspective, the supply side matters just as much as the mechanism. ROBO has a fixed 10 billion maximum supply according to both the white paper and market trackers. Current circulating supply is about 2.23 billion, which puts the live market cap around $69 million and the FDV around $311 million at recent prices near $0.031. That gap is not fatal, but it is not small either. The white paper allocates 24.3% to investors and 20% to team and advisors, both on a 12-month cliff followed by 36 months of linear vesting. So even if the story is interesting, the market still has to absorb future supply. I do not care how elegant the theory is; if usage does not grow fast enough to offset unlock pressure, the chart will feel that first.

That is also where the retention problem shows up. A network like this does not survive on launch attention. Operators have to keep bonding because there is enough real work to justify the lockup. Buyers of robot services have to keep paying because the service is cheaper, more reliable, or easier to verify than off-network alternatives. Validators and challengers have to keep watching because fraud detection is worth the effort. Developers and businesses have to keep staking because access to the network actually matters. Fabric’s own design hints at this by tying some rewards and usage credits to verified work rather than passive holding. Delegators, for example, are not supposed to earn like proof-of-stake validators just for parking capital; they earn usage credits only when supported operators complete verified work. That is healthier in theory. But it also makes the usage loop harder. Real demand has to recur.

And there are plenty of ways it can break. Weak verification is the obvious one. If the network cannot reliably distinguish real work from spoofed activity, the whole institutional claim starts to collapse. Fabric does at least define challenge bounties, fraud penalties, uptime checks, and quality thresholds. Proven fraud can trigger significant slashing of the earmarked task stake, availability below 98% over a 30-day epoch can slash bonds and wipe emissions, and low quality can suspend reward eligibility. Good. Necessary. Still, these are only as strong as the detection layer and the willingness of participants to challenge bad behavior. If verification is noisy, low-quality operators can farm the narrative while the token trades ahead of evidence. Crypto does this all the time.

So my framework here is pretty simple. I get more bullish if I see bonded participation rising alongside actual service demand, not just exchange volume. I want proof that operators are willing to lock capital, that task completion is being verified repeatedly, that protocol revenue is real enough for fee conversion and buy pressure to matter, and that the story stays messier than the marketing. Clean narratives usually top before messy systems mature. I get more cautious if the chart keeps leaning on listings and category hype while usage remains hard to measure, especially with a circulating-to-FDV gap that still leaves room for future supply pressure. ROBO is already liquid enough to trade on major exchanges, which means perception can run ahead of operational truth for quite a while.

My closing view is not that Fabric is guaranteed to work. It is that the most serious part of the idea is not robot scale at all. It is whether they can build enough institution-like structure around machine labor that recurring economic behavior starts to look durable instead of staged. Traders should watch that, not the slogans. Watch whether identity, bonding, verification, payment flow, and participation rights start producing repeat usage. If those behaviors show up, the market will eventually notice. If they do not, then “robot economy” is just another story with a ticker.