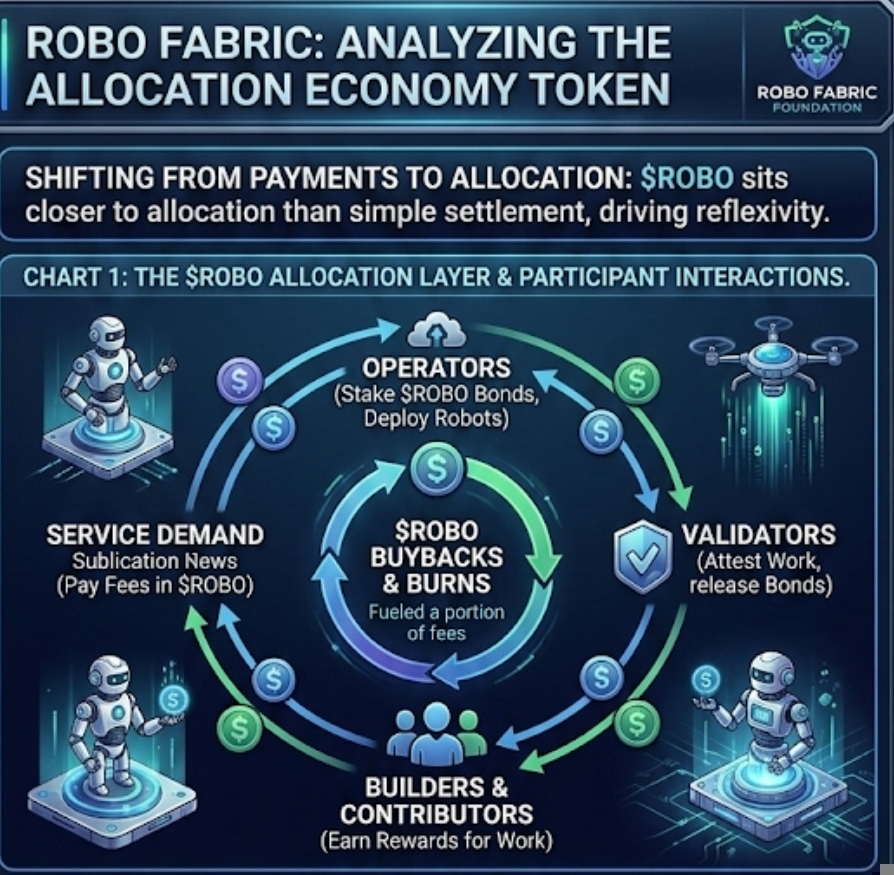

I remember watching a few infrastructure tokens reprice almost instantly the moment the market decided they were “not just another payments rail.” That shift usually happens when traders realize the token is sitting closer to allocation than settlement. Settlement is useful, but allocation is where markets tend to get more reflexive. What caught my attention with Fabric was that its own language keeps pushing past robot payments and into something broader: identity, coordination, deployment, and capital allocation for robotic labor. The official framing is pretty explicit about this. Fabric says it is building a payment, identity, and capital allocation network so robots can operate as economic participants, and its blog describes coordination pools where community-supplied stablecoins support robot deployment while $ROBO sits inside the operating and settlement layer.

At first I assumed this was just another AI-adjacent token using robotics as a narrative wrapper. Over time that started to look different. Fabric’s design is not mainly saying, “robots need a coin.” It is saying robots need a way to be financed, registered, verified, coordinated, and paid across a shared network rather than inside closed fleet silos. That matters because if a network helps decide which machines get deployed, who gets initial access to task flow, who posts bonds, and how work gets validated, then the token is closer to a market for robot capacity than a simple medium of exchange. That is a much more interesting structure from a trader’s perspective.

The mechanism is where the idea starts to get real. Fabric says operators stake $ROBO as refundable performance bonds, fees are paid in $ROBO, developers and contributors are rewarded for verified work, and governance locks create veROBO-style participation. On top of that, Fabric describes decentralized coordination for robot genesis and activation, where participants contribute tokens for network participation and priority access weighting during a robot’s early operating phase. In plain terms, the network is trying to turn deployment into a coordinated market: operators bond in, validators attest work, contributors earn for useful activity, and some revenue may be used to buy $ROBO on the open market. If this works, token demand does not come from vague future utility. It comes from operators needing access, builders needing entry, validators needing alignment, and service demand pushing fee flow through the network.

This is also where I think the market misses something. Most people hear “robot economy” and jump straight to hardware adoption curves. I think the first pricing question is simpler: who allocates scarce robotic capacity when machines are still expensive, operationally fragile, and unevenly distributed? Fabric’s own blog says the current model is one operator raising private capital, buying robots, running operations internally, and settling bilateral contracts off-network. Fabric is trying to replace some of that with transparent coordination pools and standardized participation rights. That does not mean token holders own robots. The project is careful to deny equity, profit share, or hardware ownership rights. But even without ownership, being the coordination layer for deployment can still matter a lot economically. Exchanges have priced stranger things.

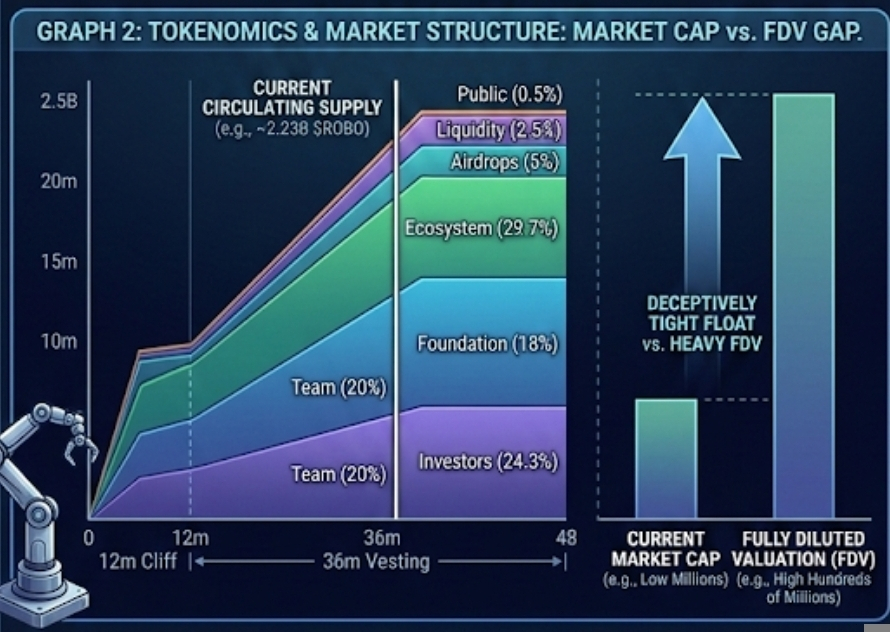

The tokenomics are worth slowing down for because this is where a good story can still become a bad trade. The whitepaper fixes total supply at 10 billion $ROBO. Of that, 24.3% goes to investors and 20% to team and advisors, both with a 12-month cliff and 36-month linear vesting. Foundation reserve gets 18%, ecosystem and community 29.7%, airdrops 5%, liquidity provisioning 2.5%, and public sale just 0.5%. That tells me two things. First, the float can look deceptively tight early, especially if staking and governance locks absorb part of circulation. Second, FDV can stay psychologically heavy for a long time unless real usage starts soaking up supply. Fabric’s own supply model is built around vesting releases, work bonds, governance locks, burns, and fee-driven buybacks, which is elegant on paper, but it also means traders need to separate “circulating squeeze” from actual economic demand.

Right now that distinction matters. Market trackers show roughly 2.23 billion tokens circulating out of the 10 billion max supply, with live price in the high two-cent to low four-cent range depending on the moment, leaving market cap materially below FDV while 24-hour volume has already been large relative to market cap. CoinGecko also shows trading concentrated on major centralized venues including Binance, OKX, and Bybit. That combination usually creates very noisy price discovery early on. Listings and volume can make a token look stronger than its retention loop actually is. I have seen that before. Good distribution plus derivatives access can manufacture attention long before a protocol manufactures repeat demand.

The retention problem is the real test. A robot network does not become valuable because people speculate on robot narratives for two weeks. It becomes valuable if operators keep bonding in, buyers keep paying for services, validators keep challenging bad work, developers keep shipping modules, and enough of that activity repeats without mercenary subsidies doing all the work. Fabric’s whitepaper tries to address this with an adaptive emission engine that raises or lowers emissions based on utilization and quality, plus structural demand sinks tied to fees, bonds, locks, burns, and buybacks. In theory that is sensible. In practice it only works if the network can measure real work credibly. If utilization is easy to spoof, or quality scores get gamed, emissions can subsidize noise instead of useful activity.

And there are obvious failure modes. Weak verification is one. The whitepaper leans on validator attestations, uptime checks, slashing, and challenge bounties, including meaningful penalties for proven fraud and service degradation. But robotic work in the real world is messy. Sensors fail. Tele-ops can mask autonomy gaps. Low-quality operators can inflate activity while offloading costs elsewhere. If detection probability is low, the slashing math looks less comforting than it does in a PDF. I also worry about coordination quality. A capital allocation market is only as good as the standards that decide which robots, tasks, and operators deserve scarce network attention. If that process turns political or gamified, the token can keep trading while the mechanism quietly degrades.

From a trader’s framework, I would get more constructive if I saw three things happen together. First, recurring on-network service demand rather than one-off listing excitement. Second, a rising share of supply locked in work bonds and governance without a collapse in liquidity. Third, evidence that buy pressure from real protocol activity is starting to matter more than launch-driven speculation. I would get more cautious if the story becomes cleaner while the evidence gets thinner, especially if volume stays high but usage metrics remain vague, or if upcoming vesting overhang starts meeting weak fee generation. Fabric’s concept is interesting precisely because it reaches beyond payments into capital allocation. That makes the upside more interesting, but it also raises the standard of proof.

My closing view is pretty simple. Fabric is worth watching, not because “robots” is a hot narrative, but because it is trying to turn deployment, verification, and access into market structure. That is more ambitious than a payment token and harder to fake over time. Traders should watch behavior, not branding. If bonded participation, verified work, and repeat service demand start to absorb supply, the market may eventually treat $ROBo as infrastructure for capital allocation. If not, it will trade like many early tokens do: a smart story with a thin loop underneath.