Markets Are Turning, But the Real Test Starts Now

Hey everyone, and welcome to the Weekly Market Roundup

Markets begin the last full week of April with optimism improving, but not yet fully validated. Bitcoin has pulled back toward $74,400 after completing last week’s bullish leg, now testing an important near-term zone as price searches for fresh direction. Broader structure remains constructive, with Bitcoin still positive on weekly time frames, though it continues to trade below the 21-week EMA. Key resistance levels remain overhead, with the major breakout zone near $81,000 still the level to reclaim.

The macro backdrop has become more complicated. Renewed US-Iran conflict concerns have brought energy markets back into focus, raising the risk of higher oil prices and a more persistent inflation narrative.

At the same time, Ether is showing relative strength, with the ETH/BTC ratio climbing to a 10-week high. Ethereum network activity has also improved sharply, with daily active addresses rising from 384,763 on April 5 to 730,278, signaling stronger user engagement and adding support to ETH’s recent momentum.

In this issue, I’ll break down what actually drove the movement, how macro catalysts are compressing into a high-impact window, what on-chain flows are revealing about holder behaviour, and where structural momentum may emerge next.

Let’s get into it.

Note to Readers:

Over the past months, many readers have told us that the Crypto Market Weekly has become a core part of their routine, and we will continue publishing these weekly updates here on Substack as usual.

As we evolve our research offerings, our long-form institutional research will gradually move from Substack to a dedicated research hub on our community platform. As part of this transition, paid Substack subscriptions for long-form reports will be discontinued going forward. Existing subscriptions will be cancelled as we shift to this new model, while the weekly market updates will remain available here unchanged.

We are building a more focused research environment designed for deeper, curated, institutional-grade analysis for investors. More details on the transition to new research hub and access model will be shared soon.

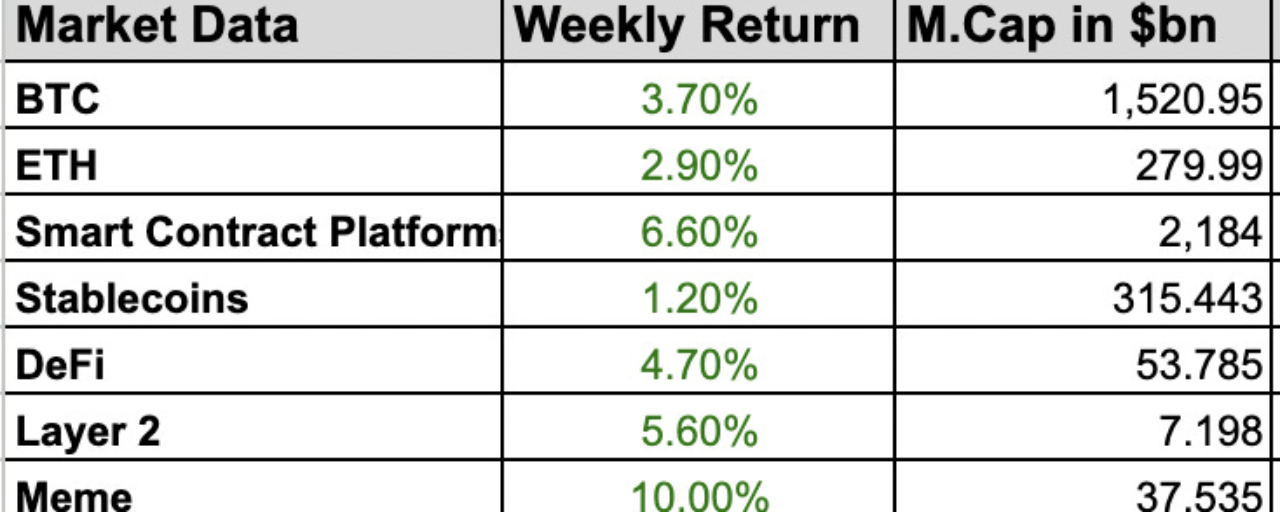

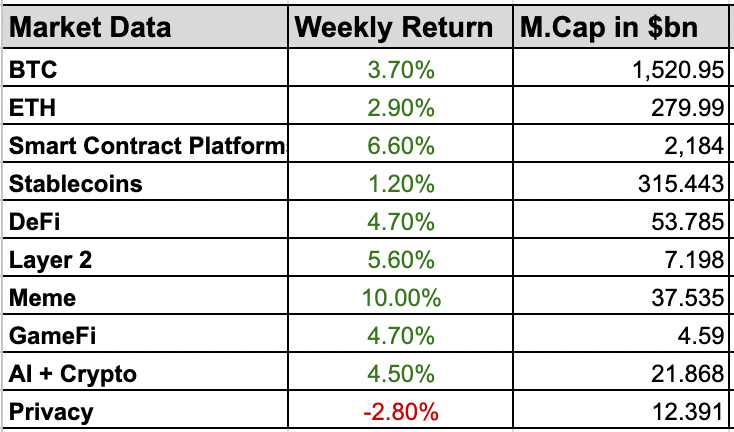

1. Sector Performance & Key Developments

Kelp restaking platform exploited, $293M drained in attack

Aave’s TVL tanks $8B a day after $293M Kelp DAO hack

Polymarket in talks to raise $400M at a $15B valuation

Strategy buys 34,164 Bitcoin for $2.5B, holdings top 800,000 BTC

ZachXBT asks MemeCore to explain valuation and token supply

Japan to test government bonds as digital collateral on Canton

Bitmine buys 101,627 ETH in largest purchase since December 2025

Tether takes 8.2% stake in Bitcoin mining finance platform Antalpha

Crypto in sustained winter as CEX volumes drop 39% in Q1 as per CoinGecko

2. Apple’s Next Era Begins: John Ternus Takes Over

Apple Inc. has announced its biggest leadership change since the Steve Jobs era. John Ternus will become CEO on September 1, 2026, while Tim Cook will move into the role of Executive Chairman. The decision was unanimously approved by the board.

Cook joined Apple in 1998 and became CEO in 2011 following the passing of Steve Jobs.

During Cook’s tenure, Apple grew from a company worth roughly $350 billion to nearly $4 trillion, making it one of the most successful corporate runs in modern history.

Now leadership moves to Ternus.

At 50, he is a longtime Apple executive and currently serves as Senior Vice President of Hardware Engineering. Inside the company, he has built a strong reputation as a serious product leader with deep technical credibility.

Ternus has played a major role across the iPhone, iPad, Mac and broader hardware engineering efforts.

More recently, his responsibilities expanded into areas such as design, robotics and future product categories.

Why this matters for investors:

Cook’s Apple became known for operational excellence with world-class supply chain execution, strong margins, rapid growth in services revenue, deep global relationships and aggressive shareholder returns through buybacks.

Ternus signals a different emphasis.

He is widely seen as an engineering-led executive, someone focused on products and building rather than purely operations and finance, thus a new product line is anticipated.

This could mean Apple is entering a new chapter. Less about refining an already dominant business, and more about creating the next wave of growth.

The last major product-led era at Apple delivered: iPod, iPhone & iPad.

Cook is still expected to play an important role.

As Executive Chairman, he can remain focused on:

China and supply chain diplomacy

tariffs and trade issues

regulatory pressure

AI policy and government engagement

long-term strategic oversight

That setup gives Apple continuity while allowing a new CEO to focus on execution and innovation.

What investors will watch next:

Ternus’s first major keynote

Apple’s AI hardware roadmap

Any new device categories

Product launch pace

Whether revenue growth accelerates beyond the iPhone cycle

Thus September 1 is more than a management transition. It may mark the shift from Apple as an operating powerhouse to Apple chasing its next breakthrough.

If Ternus can deliver a new product cycle, it could shape the next decade for Apple Inc..

3. Macro Backdrop

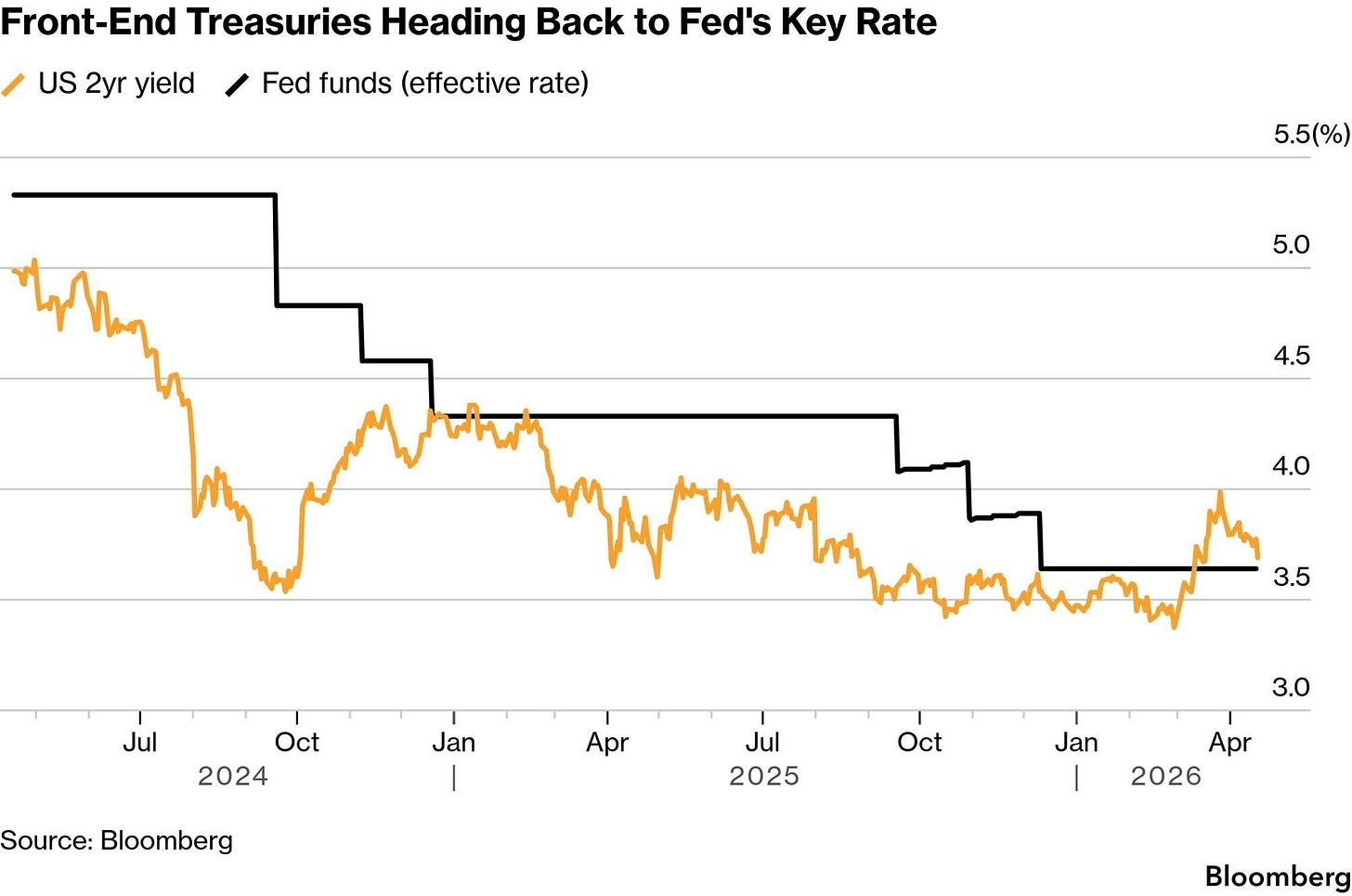

1. Energy Outperforms, Fed Put Removed

The US 2-Year Treasury Yield has quietly moved back in line with the Federal Reserve funds rate at 3.50–3.75%, signaling the bond market has stopped fighting the Fed.

Short-term rates now reflect expectations that the Fed is likely to stay on hold, with the Federal Open Market Committee meeting on April 28–29 widely expected to bring no rate change.

With that view largely priced in, the 2-year yield appears to have found a near-term floor.

Any credible peace deal, softer labor market data, weaker growth outlook, or lower inflation prints could reprice the 2-year sharply lower and quickly revive rate-cut expectations.

A fast drop in yields would typically support equities, lower borrowing costs, weaken the US dollar, and improve overall risk sentiment.

2. US Importers Can Now Claim Billions in Tariff Refunds

Big development for US importers: starting today, businesses can begin filing for refunds on certain 2025 tariffs through a new U.S. Customs and Border Protection claims portal.

These tariffs were originally imposed under Donald Trump using IEEPA authority. In February 2026, the Supreme Court of the United States ruled those actions exceeded presidential powers, making the tariffs unconstitutional.

Roughly $166 billion was collected across 53 million shipments, with an estimated $127 billion plus interest potentially eligible for refund.

Businesses must submit detailed shipment and payment records, and claims are expected to be processed within 60–90 days.

Refunds would go directly to importers rather than consumers.

Near-term implication: this could materially improve importer cash flow and margins over coming quarters.

Consumer impact is less certain, as any pass-through into lower retail prices depends on competition, pricing decisions, and ongoing legal challenges.

3. Markets Are Pricing Peace, But Peace Hasn’t Arrived

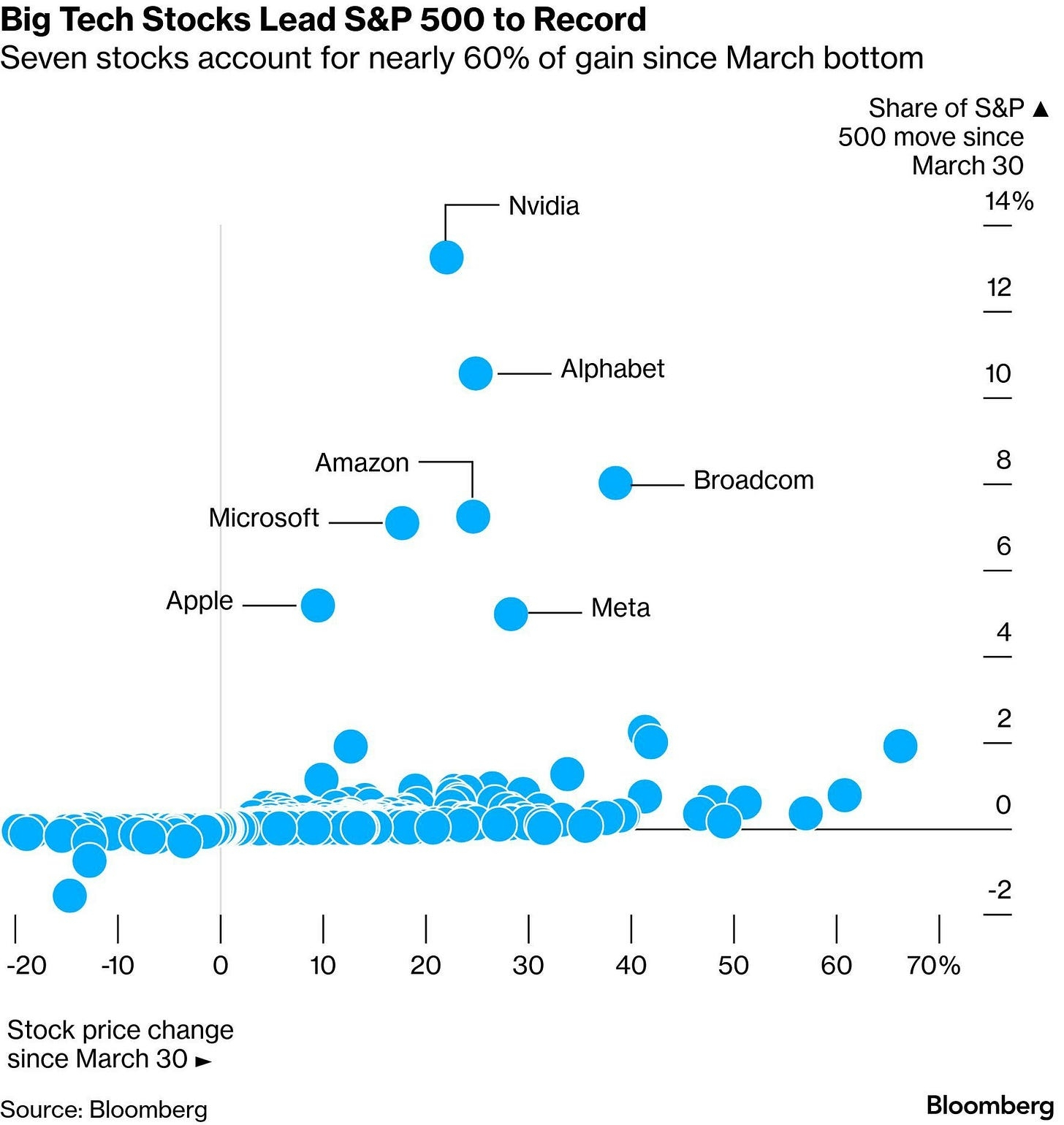

The S&P 500 has hit a fresh record high and fully erased its war-shock losses, but the rally is far narrower than it appears. Nearly 60% of gains since the March bottom have come from just seven mega-cap tech names, led by NVIDIA Corporation, Alphabet Inc., and Broadcom Inc., while most other stocks have barely moved.

Energy Sector is the clearest loser, down nearly 10%, as traders bet oil prices fall with easing geopolitical risk. That makes this move look less like a broad bull market and more like a peace trade concentrated in large-cap growth names. With leadership this narrow, the index has limited cushion if sentiment reverses.

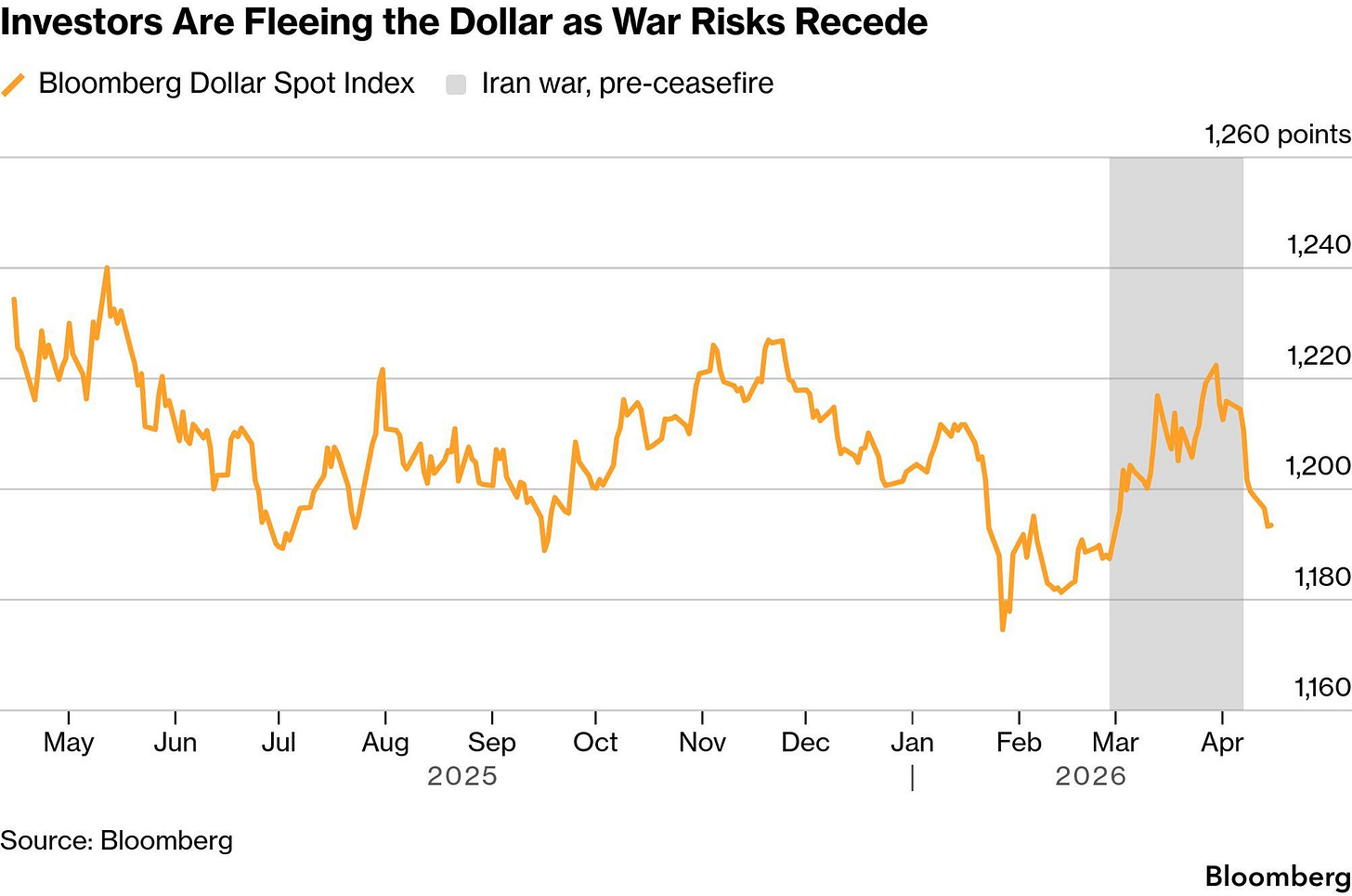

The US Dollar Index is sending the same message. It surged earlier in the conflict on safe-haven demand and expectations the Federal Reserve would stay hawkish during an energy shock, then weakened through March and April as ceasefire hopes increased. A softer dollar is typically a tailwind for equities and global risk assets.

Across assets, markets are pricing in peace before peace has actually arrived. Record equities, a weaker dollar, and stable yields all reflect expectations that the Hormuz crisis resolves quietly. But with reopening odds still below 20%, the Strait of Hormuz remains the key variable. A real resolution offers meaningful upside, while failed talks could trigger a sharp snapback.

4. ETF / ETP Flow Insights

ETF flows improved meaningfully through the week after a weak Monday start, turning positive for the rest of the sessions.

The key highlight was Friday, with $647M in inflows, the strongest single-day figure of the month.

That late-week strength pushed total ETF assets under management back to around $100B, recovering part of the recent drawdown caused by prior outflows.

Main takeaway: sentiment is stabilizing and institutional demand is returning, with signs of real conviction on stronger inflow days.

Whether this momentum sustains next week or remains dependent on broader macro conditions.

5. The Week Ahead

Focus for the week: Markets ended last week with improving sentiment. This week will determine whether that optimism is supported by stronger data and earnings, or if the rally remains fragile and macro-dependent.

6. Conclusion

Market sentiment continues to improve at a measured pace. The Fear & Greed Index has risen to 29, which still places it in fear territory, but represents a clear rebound from the extreme fear levels seen through much of the year. While confidence has not yet returned enough to move sentiment into neutral territory, the recent trend suggests panic conditions are easing and investor nerves are slowly stabilizing.

In a market driven by liquidity swings and institutional flow, our Crush Circle platform by CryptoCrush gives investors direct access to expert research, real-time guidance, and the frameworks needed to stay ahead of the next big move.

Do you think we'll hit the 'Neutral' zone by next week, or is this just a relief bounce? Let me know your thoughts below!

#StrategyBTCPurchase #WhatNextForUSIranConflict #RAVEWildMoves #KelpDAOFacesAttack #AltcoinRecoverySignals?