Here is a clear, structured, and more professional “standardized” version, suitable for analysis posts or reports:

$8 Trillion in U.S. Debt Matures in 2026 — Understanding the Real Impact

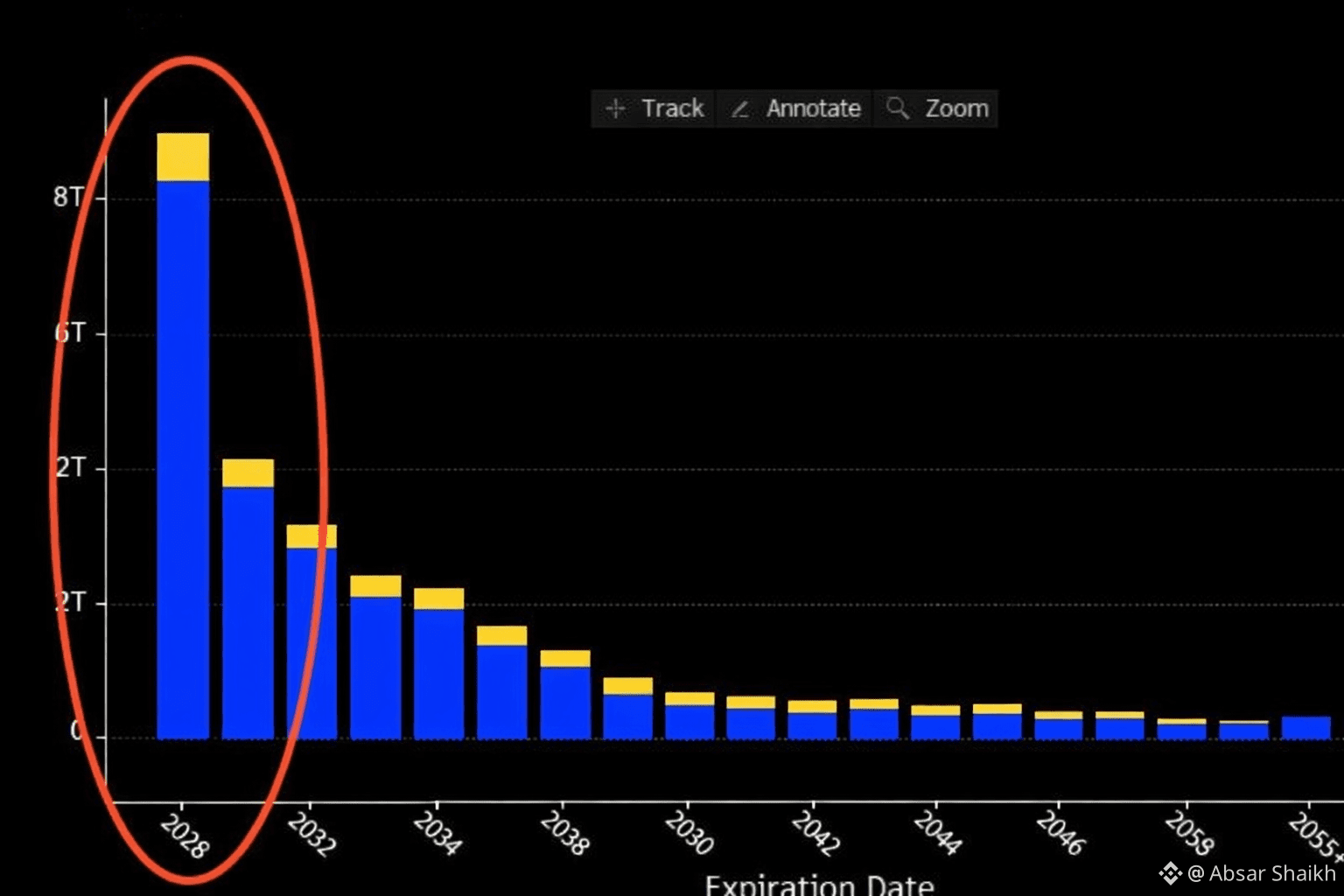

In 2026, more than $8 trillion of U.S. Treasury debt—primarily T-bills and short-term notes—is set to mature. This figure has raised concerns among many observers, with some predicting a potential debt crisis or market crash. However, this interpretation reflects a misunderstanding of sovereign debt mechanics.

The U.S. government does not typically pay off its debt outright; instead, it rolls over maturing obligations by issuing new securities. Much of the debt coming due in 2026 was issued during 2020–2021, when the government deliberately relied on short-dated instruments (T-bills and 2–3 year notes) to finance pandemic-related emergency spending.

Importantly, U.S. Treasuries are fundamentally different from corporate debt. They function as:

Global collateral

Reserve assets

The foundation of repo and money markets

Instruments supported by the Federal Reserve, which has unlimited liquidity capacity

For this reason, there is no realistic scenario in which the U.S. government is unable to refinance its debt.

That said, higher interest rates today compared to 2020–2021 do introduce meaningful implications. As debt rolls over at higher yields, the likely outcomes include:

Larger fiscal deficits

Increased Treasury issuance

Pressure to suppress real interest rates

Strong political incentives for easier financial conditions

Historically, such environments lead to:

Lower real yields

Increased liquidity support

Gradual currency debasement

This backdrop is typically bullish for risk assets. A large-scale debt rollover should not be viewed as a crash signal, but rather as an indication that policymakers will prioritize growth and liquidity over austerity.

This dynamic helps explain the Federal Reserve’s recent shift in tone. Reserve injections do not begin arbitrarily—they are often a precursor to facilitating future Treasury absorption.

In such conditions, bonds, fixed-income instruments, and cash holders tend to underperform, while equities, real assets, commodities, and cryptocurrencies benefit from accommodative policy and increased liquidity.

For these reasons, the outlook remains constructive for risk assets into the second half of Q2 2026, as the expansionary monetary framework is unlikely to reverse.

If you want this shortened for X (Twitter), converted into a thread, or made more bullish/neutral, just tell me.

#WriteToEarnUpgrade #TrumpTariffs #BTCVSGOLD