Aave’s founder just dropped a 2026 roadmap — and the market is still digesting what it actually means for $AAVE .

The plan revolves around three pillars: Aave V4, Horizon, and the Aave App. Together, they’re meant to turn Aave into the global onchain credit layer — not just the biggest DeFi lender, but the rails for trillions in credit.

A few things stand out if you look past the headlines:

• Aave V4 is about unifying liquidity at scale. Fewer silos, deeper pools, better capital efficiency. That’s critical if Aave wants to absorb institutional-sized flows without fragmenting liquidity.

• Horizon targets institutional RWA lending — the bridge between TradFi balance sheets and DeFi rails. If RWAs keep growing, Aave is positioning early to be the default backend.

• The Aave App signals a shift toward mass adoption. Not just protocols talking to protocols, but a consumer-facing layer built for millions of users who don’t care about DeFi jargon.

What’s interesting is the framing: despite dominant market share, record fees, and deep liquidity, Aave still calls itself “day zero.” That’s not hype — it’s a signal that current revenue may be small compared to what comes next if even a fraction of global credit moves onchain.

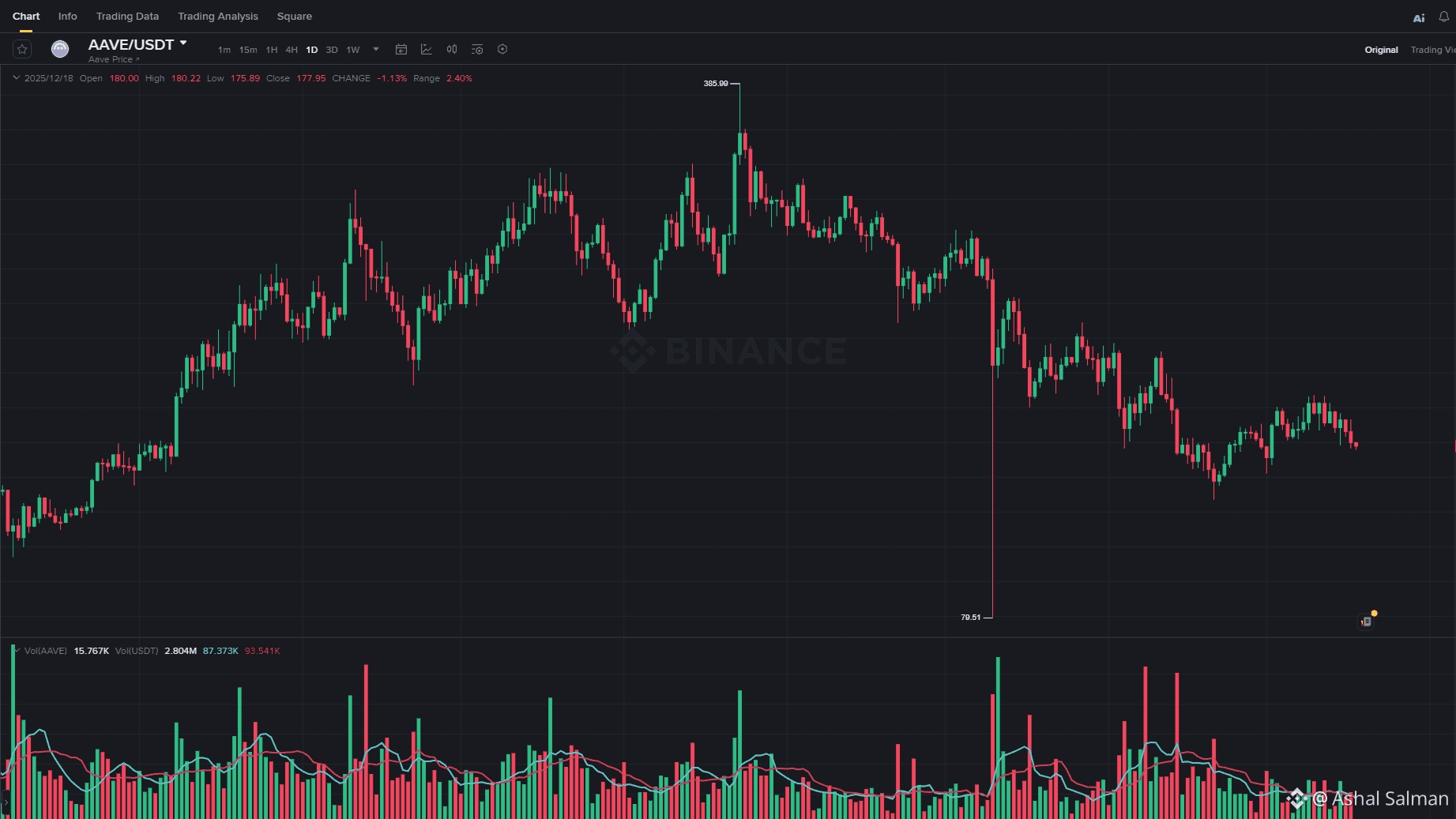

With RWAs heating up and DeFi narratives rotating back toward real yield, $AAVE is one of those assets traders tend to reprice after the infrastructure is already in motion. Worth keeping an eye on how the market reacts around this roadmap.

If you’re tracking $AAVE or exploring onchain credit plays more actively, having a clean setup helps. I use Binance for price tracking and execution — this link just unlocks the standard referral perks if you need it:

https://www.binance.com/referral/earn-together/refer2earn-usdc/claim?hl=en&ref=GRO_28502_8AUQ9&utm_source=default

Either way, the next leg for DeFi may not be about new tokens — but about who ends up owning the credit layer. And Aave is clearly trying to claim that ground.