@Lorenzo Protocol In late 2025, yield-bearing “cash” on-chain stopped being a niche hobby and started looking like infrastructure. People still want dollar exposure, but they also want it to do something besides sit idle. Tokenized Treasury products have helped normalize that expectation, because they turn a familiar instrument into an on-chain building block with visible yields and recognizable custodians. At the same time, U.S. stablecoin regulation stopped being theoretical: the GENIUS Act became law in July 2025 and established a regulatory framework for payment stablecoins.

USD1+ arrives right in the middle of that mood swing, and it’s hard to separate the product from the way Lorenzo positions itself as a builder. Lorenzo isn’t trying to be a passive wrapper that disappears behind a ticker. It’s presenting USD1+ as a designed experience: a structured route for stablecoin holders to step into yield without pretending the token itself is a payment coin. That matters because design choices are where most of the hidden tradeoffs live, and Lorenzo is making one of those choices loud and clear.

Lorenzo describes its USD1+ OTF as a yield product for stablecoin holders: users deposit stablecoins and receive sUSD1+, a token representing shares in the fund, with redemptions settled in USD1. The project also notes USD1 is issued by World Liberty Financial, which is a detail worth clocking because “settlement” is where promises become operational. If you’ve watched DeFi long enough, you learn to pay attention to where the cash-out door actually opens, not just how glossy the front entrance looks. I don’t mean that cynically. It’s just how you stay sane.

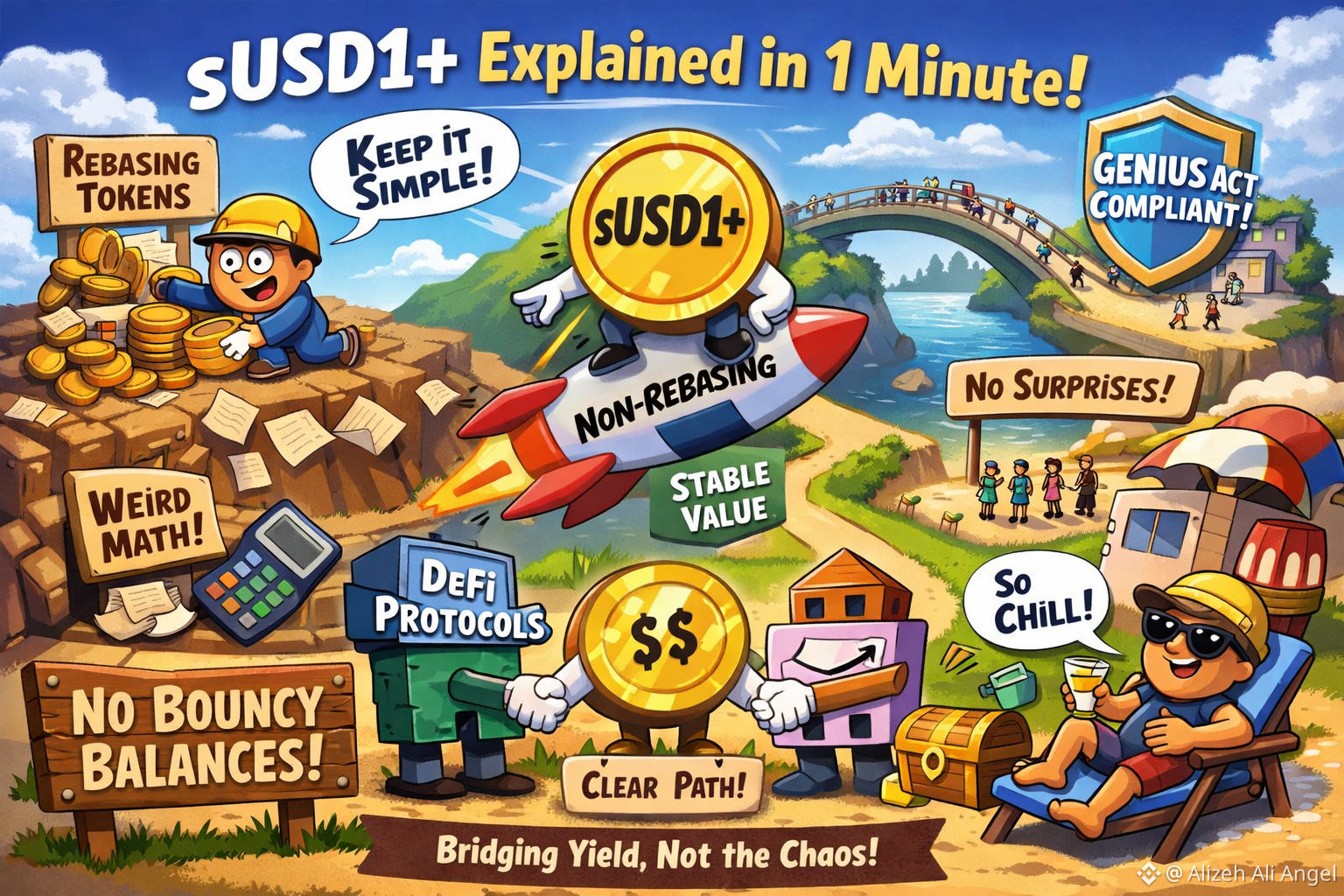

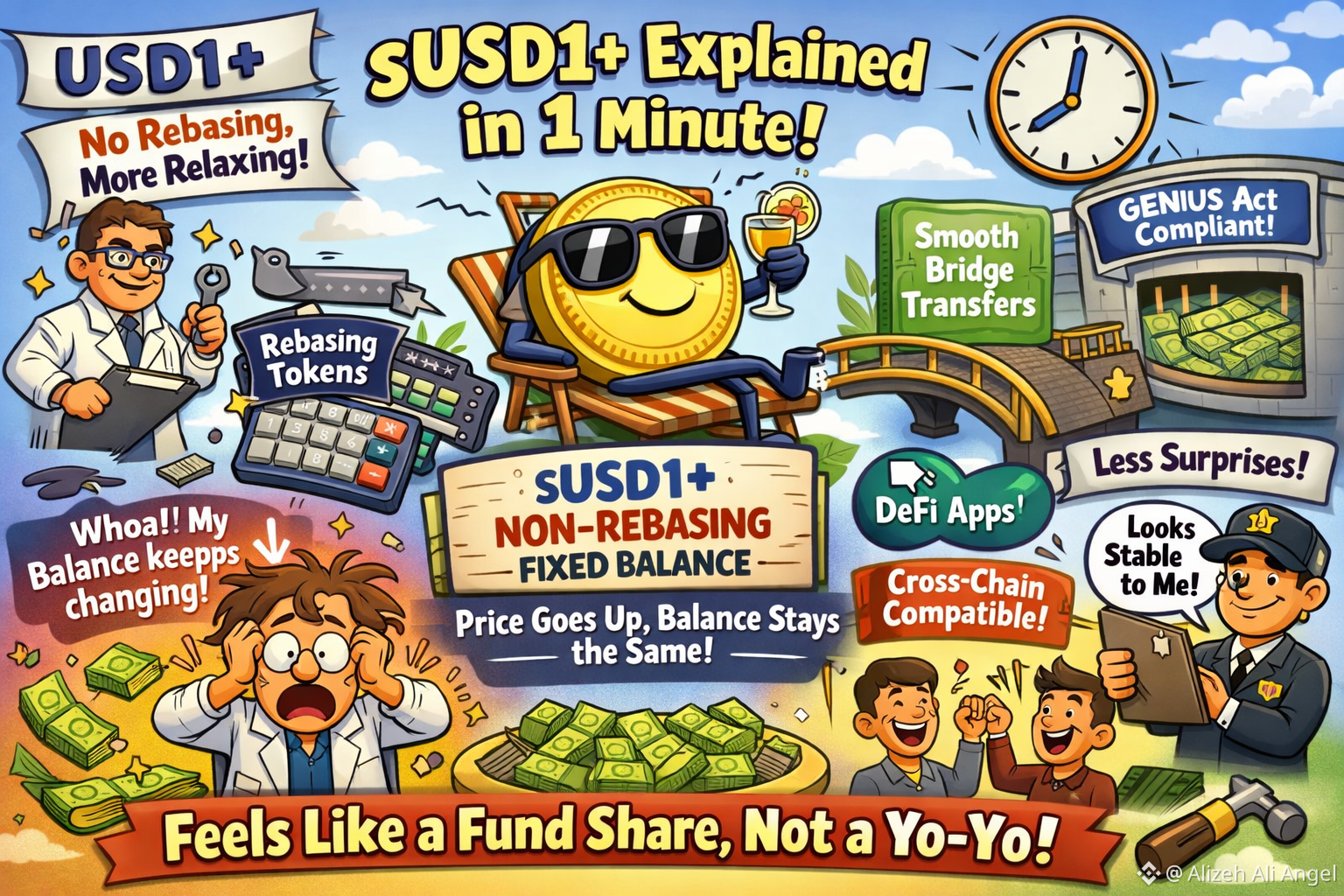

Here’s sUSD1+ explained in one minute. Some yield tokens “rebase”: your wallet balance increases over time, while the token aims to keep a steady unit value. Origin’s documentation describes this model plainly—balances rise like interest in a bank account. sUSD1+ takes the other route. It’s non-rebasing: your balance stays fixed, while the redemption value per token increases as the strategy earns, so yield shows up as price appreciation rather than extra units. That’s the core design choice people are reacting to, because it changes how the token fits into everything else.

The Lorenzo angle is that this isn’t just a technical preference; it’s an integration strategy. If you’re building something you want to travel across apps and chains, you start optimizing for the boring kind of compatibility. Rebase mechanics can be perfectly sound in isolation, but they force every downstream product to understand and accommodate them. Lorenzo’s choice reads like it’s trying to make sUSD1+ behave in a way that more protocols already know how to handle, even if that means your “yield” looks like a growing claim rather than a growing balance.

Why pick that approach? Because DeFi is full of assumptions, and rebasing violates more of them than people expect. Many apps and contracts implicitly treat an ERC-20 balance as stable unless you send or receive tokens. When that stops being true, you get edge cases: accounting that drifts, collateral checks that need special handling, and integrations that break in ways that are hard to spot until users are already in the blast radius. The broader point shows up in security write-ups about tokens that behave “weirdly” at transfer time, whether that weirdness is a fee, a reflection mechanic, or a rebasing-style balance change. The industry has spent years trying to reduce surprises, and rebasing, by definition, introduces surprises.

The staked ETH world already ran a version of this play. Lido’s stETH rebases, and the ecosystem standardized around wrapping it into wstETH for compatibility with protocols that prefer fixed balances. Lido’s own help docs say the quiet part out loud: wrapping exists so you can use your staked asset in more DeFi places without giving up the rewards. Once you’ve seen that pattern, sUSD1+ reads like a stablecoin-native rhyme: keep balances static, let value accumulate via an exchange rate. It’s not a philosophical stance so much as a practical concession to how many systems were written.

There’s also a regulatory-flavored reason this design is trending now. The St. Louis Fed’s explainer of the GENIUS Act notes that payment stablecoin issuers must hold one-to-one reserves and are prohibited from paying holders yield or interest on those coins. So if you want “dollars that earn,” you often end up building something that looks less like a payment instrument and more like a share in a strategy. Lorenzo is effectively leaning into that separation. sUSD1+ isn’t trying to be “a stablecoin that pays yield” in the simplistic sense; it’s a token that represents participation in a yield product that happens to be settled in a dollar token.

Cross-chain is another pressure point. If your balance can change on a schedule independent of your actions, bridges and messaging systems have to be extra careful about “amounts” and replay protection. Static balances make movement easier to reason about, and easier to integrate. The value is still changing, but at least the unit count isn’t quietly shifting under your feet. When Lorenzo pushes sUSD1+ into a world where people expect assets to hop networks and plug into other primitives, that predictability becomes a product feature, not just an implementation detail.

If all of this sounds abstract, look at what “progress” tends to mean in DeFi: does anyone hold it, and does anyone bother to integrate it. DeFiLlama tracks Lorenzo sUSD1+ and shows meaningful TVL, largely on BSC, which suggests the token is being used, not just talked about. That detail also tells you something about Lorenzo’s environment. BSC is pragmatic. Users tend to care about whether a token works smoothly across venues, wallets, and strategies. Non-rebasing share tokens are a clean fit for that culture because they reduce the number of places where “weird math” can ruin a normal day.

None of this turns sUSD1+ into a risk-free savings account, and it shouldn’t be framed that way. Lorenzo’s materials explicitly warn that yield is not guaranteed, NAV can fluctuate with strategy performance and market conditions, and redemptions may follow schedules rather than instant exits. The non-rebasing design doesn’t erase those realities. It just makes the asset easier to plug into other tools without creating extra technical footguns, and it makes Lorenzo’s own job easier when it comes to partnering with protocols that don’t want to special-case one more token type.

My broader takeaway is that the trend isn’t “rebasing is bad.” It’s that the market is maturing toward fewer surprises. Late 2025 feels less obsessed with compounding speed and more focused on portability, auditability, and clean integrations. A non-rebasing token like sUSD1+ is, at its core, a decision to make yield feel like a fund share instead of a constantly shifting balance. That’s not glamorous, but it’s probably why it’s catching on. And in Lorenzo’s case, it also signals a deliberate bet: if you want to be the rails for yield-bearing dollars, you have to make your token behave like something the rest of DeFi can live with.