Liquidity stress doesn’t reveal itself during calm markets it reveals itself in moments of shock.

Liquidity stress doesn’t reveal itself during calm markets it reveals itself in moments of shock.

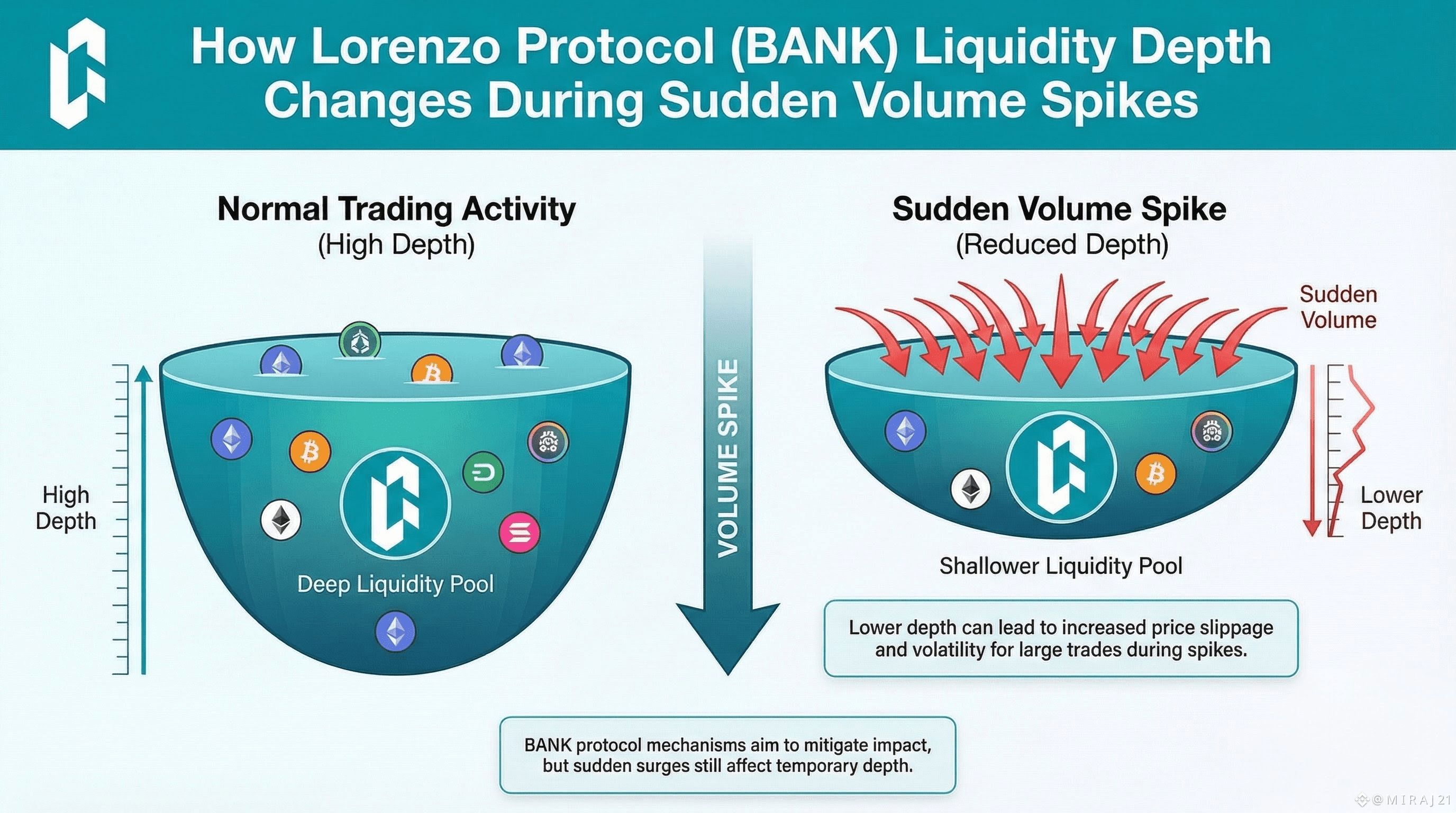

Sudden increases in volume are the ultimate stress test for any liquidity system. They expose whether depth is real or cosmetic, whether liquidity providers are aligned or mercenary, and whether price discovery remains orderly or collapses into slippage cascades.

For Lorenzo Protocol (BANK), these moments are not edge cases they are design assumptions. The protocol’s liquidity architecture is built to behave differently under stress than the emission-driven pools that defined earlier DeFi cycles.

Most liquidity disappears when volume spikes BANK’s goal is to make it reorganize instead.

In traditional AMMs and incentive-heavy pools, sudden volume often causes:

LPs to withdraw to avoid impermanent loss

liquidity to thin exactly when it’s needed most

spreads to explode

price impact to scale non-linearly

short-term traders to dominate price discovery

BANK approaches this problem by structuring liquidity as depth across bands, not just aggregate TVL. The objective isn’t to freeze liquidity in place, but to ensure that depth repositions predictably as volume increases.

During the first wave, the depth compresses, though it does not become zero.

When the volume suddenly shoots up, the usual behavior pattern of the liquidity of BANK is that:

near-mid liquidity tightens

deeper bands take absorptive flow

The price impact grows linearly but does not follow an exponential path.

depth redeemer instead of collapsar

liquefaction

However, in shallow markets, the initial trades account for most of the liquidity, causing price gaps to open quickly.

In regard to BANK, depth has migrated outward, ensuring that there is consistency in price discovery.

This is because liquidity is rewarded for staying, and not leaving.

BANK's incentive scheme also rewards participation over opportunistic presence. Liquidity providers who contribute constantly, regardless of market fluctuations, benefit from:

sustained fee capture in high volume

lower relative exposure than early exit LPs

incentive alignment with market conditions, not APY

structural prevention of immediate withdrawal

This has a very important underlying impact: in times of spikes, LPs are provided incentives to absorb demand, rather than withdraw from it.

Volume spikes widen spreads but in a controlled, information-rich way.

No healthy market keeps spreads fixed during stress. The question is whether widening is chaotic or disciplined.

On BANK, increased volume typically results in:

gradual spread expansion reflecting real demand imbalance

preservation of multi-level depth instead of a single thin band

reduced cliff effects where price jumps violently

better signaling of true market pressure

Instead of masking volatility, BANK allows it to surface but without breaking the market.

Liquidity depth now becomes asymmetric this is a feature, not a bug.

“When directional volume spikes occur, the liquidity pattern of BANK will necessarily diverge

There will be more depth on the side of aggressive flow.

contarian liquidity earns higher fees

"Price discovery accelerates, and then slows up just enough to prevent overshoots into

depth rebalances when the flow normalizes

This asymmetry helps to act as a shock absorber, preventing reflex trading and at the same time ensuring market clearance.

The comparison to a pool of the 2021 style makes clear the distinction.

In many 2021 DeFi pools, sudden volume caused:

instant liquidity evaporation

cascading slippage

price overshoots disconnected from fundamentals

rapid post-spike illiquidity

BANK’s design designates liquidity as a structural layer rather than a subsidy. A structural layer is not meant to be an elastic depth but a fluid one.

It is post-spike behavior that most clearly distinguishes BANK’s design.

Following the normalization of volume, the BANK liquidity usually reflects:

quicker re-centering on the new price

tighter spreads returning organically

decreased long tail illiquidity

very small need for external incentives to “restart” markets

It means that there was no destruction of liquidity during the peak; it was more of a re-pricing of liquidity that was subsequently re-anchored.

Why this matters for emerging tokens.

Early-stage assets: Sudden increases in trading volume tend to be associated with:

listings

news events

text changes

Coordinated Trading Activity

In these situations, if liquidity dries up, loss of reputation can become unremediable.

BANK’s behavior under stress gives emerging tokens a chance to survive their first real liquidity tests without devolving into chaos.

Liquidity depth under stress becomes a credibility signal.

Traders, funds, and market makers watch how depth behaves when volume surges. BANK’s controlled response provides:

confidence that markets won’t break under pressure

better conditions for professional participation

reduced fear of exit liquidity traps

higher trust in long-term market quality

Over time, this reliability compounds into benchmark status.

The deeper insight: BANK doesn’t try to eliminate volatility it engineers resilience.

Sudden volume spikes are inevitable.

Fragile liquidity systems pretend they won’t happen.

Resilient systems design for them.

BANK’s liquidity depth during spikes demonstrates a shift away from cosmetic TVL toward functional market structure where depth adapts, absorbs, and recovers rather than vanishing.

Conclusion: real liquidity is defined by how it behaves when stressed.

Anyone can look liquid during quiet markets.

Only disciplined architectures remain liquid when volume explodes.

If BANK continues to demonstrate controlled depth compression, predictable spread behavior, and fast post-spike recovery, it strengthens its case as a benchmark liquidity layer not just for calm conditions, but for the moments that truly define market quality.

Liquidity isn’t proven by how much is present it’s proven by how it behaves when everyone tries to use it at once.