1. The Psychology of the Software Sector Collapse

The recent volatility in software equities serves as a critical leading indicator for broader market sentiment, mirroring the structural re-ratings observed during previous epochs of rapid technological displacement. Historically, the software sector has been a primary engine of growth; however, its current price action reflects a profound psychological shift among institutional participants. We are witnessing an "anthropic disruption" where Artificial Intelligence is no longer viewed exclusively as a tailwind for legacy providers. A pivotal moment in this sentiment shift was the recent robot exhibition during the Chinese New Year, which acted as a catalyst for investors to re-evaluate AI as a terminal threat to established moats. This has led to an aggressive re-rating of valuations for stalwarts such as Adobe, Salesforce (CRM), and IBM.

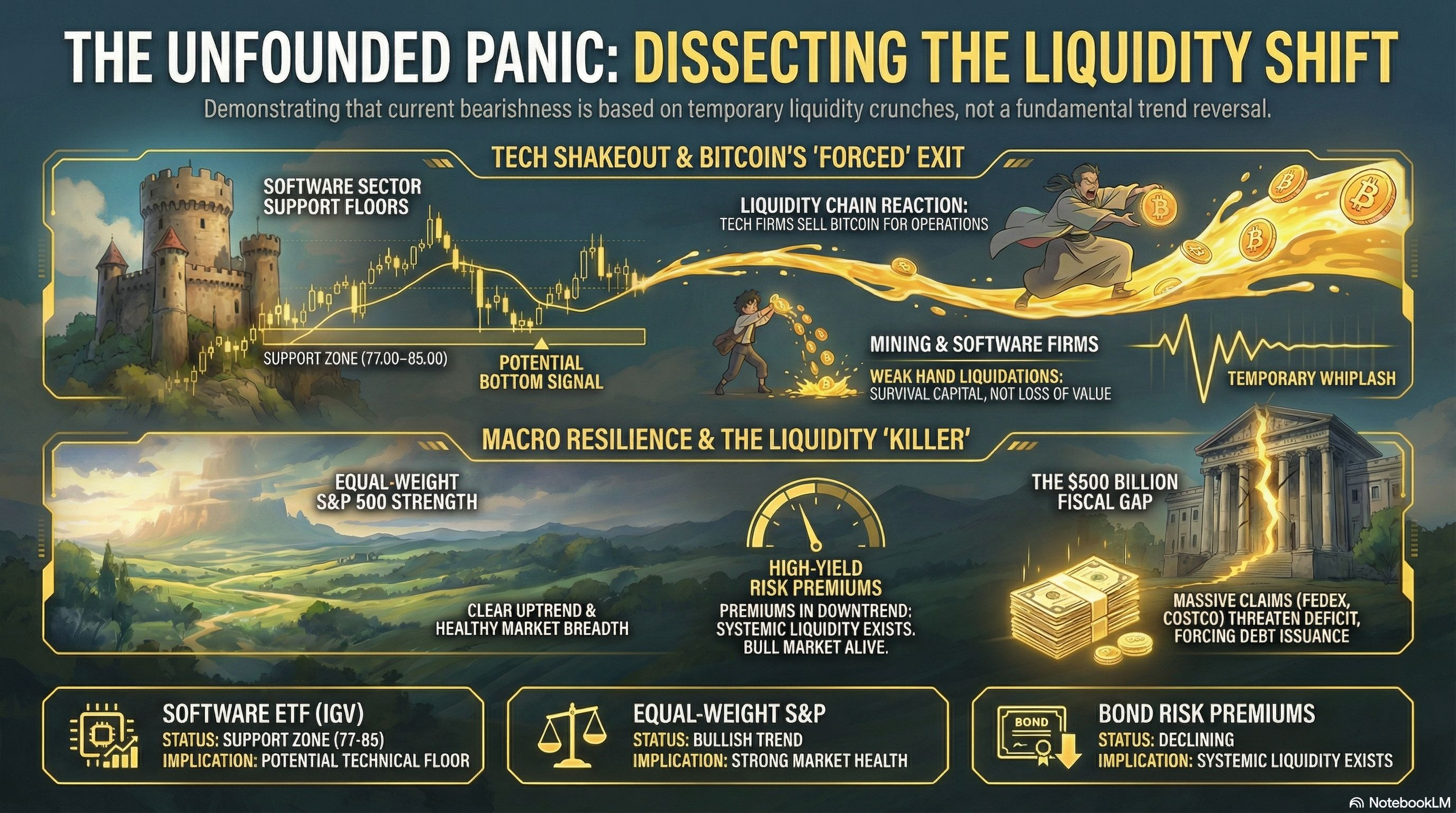

The parallels to the 2000s "Dot-com" era are instructive. During that period, companies with multibillion-dollar market capitalizations—once considered indispensable—saw their valuations compressed toward zero as their underlying models were rendered obsolete. From a strategic perspective, identifying a "technical floor" is paramount before assuming a mean reversion. We are monitoring the IGV ETF, which is currently testing a historical support zone between 77 and 85. For a signal of stabilization, the index must reclaim the 79.35 level and fill the subsequent gap. However, institutional control remains biased to the downside until the 87 resistance level is cleared; below this threshold, the bearish narrative maintains structural dominance. This sector-specific capital destruction is exerting secondary pressure on liquidity, spilling over into alternative asset classes.

2. The Bitcoin Liquidity Trap: Forced Selling vs. Fundamental Value

The high correlation between software sector weakness and Bitcoin’s recent price compression is not an indictment of the asset’s fundamental thesis, but a symptom of specific market plumbing failures. As traditional and shadow banking entities restrict credit to the tech sector, firms are forced to treat their most liquid holdings as "liquidity valves." In this environment, Bitcoin has been sold not due to a loss of faith in its role as a store of value, but as a desperate measure to maintain operational solvency.

The liquidation profile of Bitdeer (BTDR) provides a clinical case study of this "Weak Hand" phenomenon. As the firm pivoted from cryptocurrency mining to AI and High-Performance Computing (HPC), it faced acute treasury pressures. Over an eight-week period, Bitdeer aggressively liquidated 2,000 BTC. Critically for market timing, Bitdeer has now reached zero BTC holdings. This represents a vital exhaustion signal, as a significant source of price-insensitive selling pressure has been fully depleted. Having exhausted its digital reserves, the firm has been forced to issue high-interest convertible notes—a high-cost survival strategy that underscores the severity of the current credit environment.

The Mechanics of the Liquidity Crunch

Credit Restrictions: Tightening lending standards from both traditional and shadow banking institutions are choking tech-sector cash flows.

Bitcoin as a Liquidity Valve: Digital assets are being utilized as the primary source of immediate cash when traditional credit lines are frozen.

High-Cost Survival Strategies: The transition from asset liquidation to the issuance of dilutive convertible notes marks the final stage of the liquidity search for distressed tech firms.

While these localized disruptions are significant, they must be weighed against broader market indices that suggest these pressures have not yet become systemic.

3. Gauging the Bull Market’s Vital Signs: RSP and Credit Spreads

To understand the true health of the current cycle, analysts must look beyond the capitalization-weighted S&P 500, which is heavily distorted by the "Magnificent Seven." A more accurate diagnostic of the economy is found in the Equal-Weight S&P 500 (RSP). Despite the acute volatility in the software space, the RSP’s primary upward trend remains intact. This divergence suggests that the broader market is currently robust enough to absorb the localized "whiplash" affecting the tech sector.

Ultimately, the Federal Reserve remains the primary "market killer." Institutional history shows that bull markets do not die of old age; they die of liquidity withdrawal. A clinical analysis of high-yield bond risk premiums (credit spreads) confirms that systemic liquidity remains sufficient. Credit spreads are currently in a sustained downtrend, signaling that the Fed has not yet initiated the type of liquidity contraction required to end the primary bullish trend. The current distress is a function of specific participants running dry on cash rather than a systemic failure of the credit markets. However, external fiscal pressures are emerging that may eventually challenge this stability.

4. The Fiscal Reckoning: Tariff Litigation and the Debt Deficit

A significant strategic risk is emerging from legal challenges to historical trade policies, specifically litigation regarding "illegal tariffs" implemented during the Trump administration. Major corporate entities, led by FedEx, have initiated lawsuits to reclaim funds paid under these tariffs. This legal movement is scaling rapidly; while it began with approximately 1,000 large-cap firms like FedEx and Costco, it has the potential to expand to 300,000 companies.

The fiscal implications of this litigation represent a significant impairment to U.S. revenue projections. Estimates suggest potential refunds of $133 billion to $140 billion. More importantly, this creates a substantial "fiscal hole" in long-term planning. While the Trump administration's initial revenue projections were optimistic, this litigation could result in a $600 billion shortfall over the next decade. This revenue gap will inevitably force the Treasury to increase debt issuance to fund the widening deficit, further straining a fiscal system that is already showing structural fractures. This looming increase in debt supply reinforces the long-term necessity of holding "hard" assets that reside outside the traditional credit system.

5. Conclusion: Strategic Positioning in a Fragmented Economy

The current market landscape is defined by a sharp dichotomy: a localized credit crunch in software and forced selling in Bitcoin, contrasted against a broad equity market that remains structurally sound. The "anthropic disruption" in software is a genuine evolutionary shift, but the resulting forced liquidations should not be mistaken for a systemic market peak. The exhaustion of selling from "weak hands" like Bitdeer suggests that the downward pressure on Bitcoin is reaching a point of depletion.

Personal Reflection My assessment is that while the fiscal system is effectively "broken"—evidenced by the $600 billion revenue shortfall and the necessity of increased debt issuance—the primary market trend is still supported by sufficient liquidity. The extreme bearishness currently surrounding software is a standard reaction to a major technological pivot, reminiscent of the early days of the railroad or the internet. My strategic focus remains fixed on the path of least resistance: once the forced selling phase concludes and "liquidity-dry" participants have exited the market, high-quality assets will likely resume their upward trajectory. In an era of fiscal instability, the S&P 500 (broadly), Gold, and Bitcoin remain the only viable hedges against a deteriorating credit system. Professional investors should prioritize liquidity signals and credit spreads over the current wave of sensationalist headlines.