On February 27, 26, #OpenAI完成1100亿美元融资轮 , the pre-investment valuation was 730 billion dollars (post-money approximately 840 billion dollars), setting the record for the largest single deal in private technology history.

Major investors include Amazon (50 billion), NVIDIA (30 billion), and SoftBank (30 billion), while Microsoft did not participate this time. This article will comprehensively analyze from business fundamentals, valuation and profit logic, technical barriers, comparisons within the same field, to professional investor judgment, helping you assess your holding decisions.

From the financing itself, what is the capital betting on.

From public information, this round of financing is not merely a financial investment, but rather a strategic capital deeply bound to computing power, cloud infrastructure, and long-term cooperation terms.

Amazon's investment comes with deeper cloud service collaboration, Nvidia's participation simultaneously means priority supply of high-end GPUs and inference resources in the future, and SoftBank provides long-term capital and global industrial resources. This investment structure itself indicates that OpenAI is seen as a 'strategic platform that requires long-term nurturing' rather than a short-cycle return application company.

For investors, the key to determining whether this round of financing is reasonable lies not in current profits, but in one question: has the large model evolved from being a tool to becoming an irreplaceable productivity infrastructure?

Business fundamentals: user-driven dual engines, revenue structure continuously optimizing.

OpenAI's current user base shows a distinct dual-engine driving pattern. The personal side has over 900 million weekly active users, doubling since early 2025, with over 50 million users being paid subscribers (Plus, Pro, Team plans), contributing stable cash flow and brand exposure.

The enterprise side serves over 1 million commercial customers and more than 7 million enterprise workstations, with 92% of Fortune 500 companies using it, achieving a retention rate of 88%. This structure allows OpenAI to transition smoothly from a consumer-level phenomenon to an enterprise-level infrastructure.

In 2025, annual revenue reached $13.1 billion, with an annualized run rate exceeding $20 billion by year-end. Among the revenue components, consumer subscriptions account for about 55-75%, while enterprise seats and customized solutions account for 25-30%, and API calls account for 15-20%. The token consumption on the enterprise API side has shown explosive growth, with organizations' average reasoning token usage increasing 320 times year-on-year, over 9,000 organizations processing more than 10 billion tokens, and nearly 200 exceeding 1 trillion tokens.

This indicates that enterprises are transitioning from the experimental phase to production-level deep deployment, continuously elevating single customer value. Growth expectations point to revenues of $25-30 billion by 2026, with a potential surge to $100 billion by 2029, and further reaching $280 billion by 2030. The core driving force behind this expectation comes from three aspects: the continuous leap in model capabilities directly unlocking new scenarios such as autonomous programming, medical assistance, and personalized education; deepening enterprise penetration, with employees of leading companies saving an average of 40-60 minutes of productivity daily, with ROI already quantifiable, and strong momentum across the entire industry; and the acceleration of global and ecosystem expansion, with API customers leading in international markets like Japan, forming an efficient distribution network with developer platforms and cloud partners. The expansion of computing power, model iteration, and adoption is forming a rapid positive cycle, and as long as the leading position is maintained, revenue growth will significantly surpass that of traditional software companies.

Value and profitability logic: high growth premium supported by scale flywheel.

With a pre-investment valuation of $730 billion corresponding to an annualized revenue run rate of $20 billion, the current PS ratio is about 36 times. This level is a reasonable premium in the context of high growth: if a compound growth rate of 2-3 times is maintained from 2026 to 2028, the forward PS will quickly drop to the range of 10-15 times, consistent with the paths of early Nvidia and Salesforce, among other high-growth tech platforms. The profitability inflection point depends on the continued decline in reasoning costs and the realization of scale effects, with the current gross margin at about 33%, expected to improve significantly after 2027 with enhancements in hardware efficiency and optimization. The market is essentially paying for the next generation of intelligent operating systems. Leading platforms train cutting-edge models through massive computing power, resulting in better products and user stickiness, which in turn feeds back data and revenue, forming a closed loop. The PS ratios of OpenAI and leading companies in the same sector are currently at 30-40 times the current revenue run rate, but when looking forward to a revenue level of $100 billion in 2029, the ratio will naturally compress. What investors are buying is the long-term certainty that AI will become a foundational infrastructure akin to electricity; if OpenAI captures 20-30% of the market share, it could support a market value of $1 trillion.

OpenAI's own technological barriers: data flywheel, computing power alliance, and product closed loop.

OpenAI's core competitiveness lies in a multi-layer composite moat. First is the data flywheel, with 900 million weekly active users generating massive amounts of high-quality interaction data daily for RLHF and continuous alignment, allowing for a model iteration speed far exceeding competitors reliant on public data. Second is the computing power and infrastructure alliance, with computing power reaching 1.9GW by 2025, through long-term cooperation with Microsoft, additional custom cloud services from Amazon, and Nvidia's binding of 3GW inference and 2GW training capacity, forming the most robust supply chain lock globally. Third is the product and distribution closed loop, with the GPT Store, custom GPTs, enterprise Projects workspace, and API + multimodal (voice, image, video) integrated platform, allowing developers and enterprises to embed seamlessly. Finally, reasoning optimization and frontline Agents, with the o series chain thinking mechanism significantly improving the success rate of complex tasks, will further expand the leading gap with the self-driving Agent prioritized in 2026. These barriers together form the foundation for the transformation from 'model provider' to 'intelligent platform.' Although open-source model parameters are gradually catching up, and reasoning costs are decreasing by an order of magnitude each year, OpenAI is strategically focusing on workflow integration and industry vertical solutions during the practical adoption years, building a wider new moat.

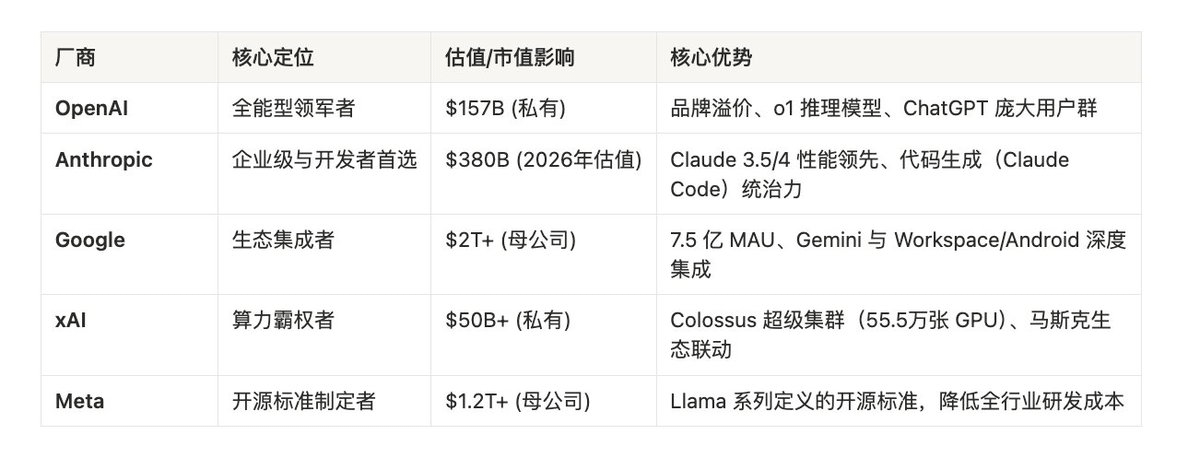

Comparison with peers: OpenAI's leading position is solid, but differentiated competition is intensifying.

In the leading camp of closed-source AI large models, OpenAI maintains the broadest ecosystem coverage with its GPT series (including o1 reasoning models, GPT-4o multimodal).

Anthropic's Claude series is rapidly rising in enterprise coding and security compliance scenarios, with enterprise LLM usage share reaching 40% by the end of 2025, and its valuation reaching $380 billion with the latest financing.

Google Gemini relies on search and cloud ecosystems, with significant cost-performance advantages, maintaining a share of about 21%. Meta Llama's open-source model attracts developers and small to medium-sized enterprises through a free strategy, but there remains a gap in closed-source capabilities and enterprise-level services.

xAI's Grok is accelerating its catch-up with real-time data and platform integration, but its overall scale is still in a following position. In terms of valuation, OpenAI leads at $730 billion, while Anthropic closely follows at $380 billion, reflecting the market's differentiated judgment on application landing paths.

In the consumer market, OpenAI holds a dominant share, while in the enterprise spending area, Anthropic and Google are accelerating their penetration. The technical capabilities are overall converging, but the landing pace varies. The overall sector has shifted from a parameter competition to a competition of ecosystems, data, and business closed loops.

For ordinary investors, they can indirectly participate through listed partners such as Microsoft, Nvidia, and Amazon; institutional investors need to focus on tracking the execution capabilities of each company in the practical adoption phase. Those who can truly embed cutting-edge intelligence into various industries will occupy long-term structural dividends. Risk factors include model commoditization due to competition, the phased pressure of capital expenditure on cash flow, regulatory and security issues, and talent mobility.

However, historical experience shows that leaders in periods of technological paradigm shifts often realize value at an unexpected speed. The story of OpenAI is essentially about humanity's strategic layout window for the ultimate resource of intelligence. Continuously tracking quarterly revenue realization, improvement in gross margins, and model benchmarking performance will help investors capture the next trillion-dollar opportunity earlier than the market.

The content of this article is compiled based on publicly available information and is for reference only, not investment advice. Investing in cryptocurrency assets involves high risks; please assess independently and consult professional advisors.