Standing at the present of 2026, investors generally feel a profound cognitive dissonance: cutting-edge technologies represented by artificial intelligence are iterating at an unprecedented speed, yet the macroeconomic sentiment remains cold, and traditional investment analysis frameworks seem to be failing. Are we at a turning point in the Kondratiev cycle? If so, how can we find a certain investment direction during the chaotic period of the old order's collapse and the new order's establishment?

This article attempts to break away from the vague debate about the specific position of the Kondratiev wave, instead using a more observable core contradiction - the 'productivity paradox' - as an analytical anchor, and combining it with a barbell asset allocation strategy to explore how to construct an investment portfolio with 'asymmetric advantages' during this special historical period.

Chapter 1 Positioning: Returning from Cycle Debate to the Reality of the 'Productivity Paradox'

K-wave cycle theory provides us with a grand historical perspective, but there is often significant lag and ambiguity in judging specific turning points. Instead of getting tangled in whether we are at the end of the fifth K-wave's depression or the beginning of the sixth K-wave's recovery, it is better to focus on a more intuitive and data-verifiable economic phenomenon: the 'productivity paradox'.

This concept was first proposed by Nobel laureate Robert Solow, which states that during a period of rapid development of computer technology, the statistical data of total factor productivity (TFP) did not show corresponding improvement. Historical experience shows that at the beginning of major technological revolutions (such as electricity, the internet, and artificial intelligence), social capital flows into the infrastructure construction of new technologies on a large scale, but due to the time lag of technology diffusion, the adaptation costs of organizational models, and the limitations of statistical caliber, macro-level productivity improvements often lag behind technological breakthroughs.

The current macro indicators confirm this judgment. Despite the exponential growth in global capital expenditure in the field of artificial intelligence, the total factor productivity growth rate of major economies remains low. This divergence of 'high input, low output' is a typical feature of the transition period between old and new cycles. It reveals that we are in a 'infrastructure investment period': technology is accelerating its penetration into the physical world, such as the surge in electricity consumption by data centers and the widespread application of AI in drug development, but this value has not yet been fully captured by the traditional GDP accounting system. Therefore, we judge that the current market is not on the eve of a technological bubble burst, but rather in a 'silent period' before a new growth curve explosion.

Chapter 2 Breaking the Deadlock: The Logic Reconstruction of Traditional Defensive Assets

In past economic downturn cycles, the consumer staples sector was regarded as a defensive asset's 'ballast' due to its rigid demand. However, under the current macro background, this traditional logic faces severe challenges. We need to carefully analyze whether this is a cyclical misjudgment or structural decline.

Looking back at the market performance from 2022 to 2024, traditional consumer staples leaders represented by Coca-Cola and Procter & Gamble, after experiencing a round of inflation-driven price increases, began to significantly underperform the market (in contrast, these assets performed well in the previous round of K-wave transitions). This is not simply a market style rotation, but a structural change in deep logic.

Observing the current consumer market, we tend to believe this is a structural logic collapse. Traditional branded consumer goods, especially those in the mid-range positioning and relying on brand premiums, are being squeezed from both ends. On one hand, the pressure of balance sheet repair globally is leading to a downgrade in middle-class consumption, significantly increasing consumers' sensitivity to prices; on the other hand, channel changes are causing extreme price-performance retailers to dismantle the pricing power of traditional brands.

However, this does not mean that all traditional consumer tracks have lost value. The market is undergoing a brutal 'Darwinian' evolution. Discount retail formats with extreme supply chain efficiency, as well as ultra-high-end brands with strong mental dominance, still demonstrate resilience through cycles. Therefore, the simple binary division of 'new and old' is no longer applicable; the real risk lies in those 'middle-layer' assets that have neither efficiency advantages nor brand moats. In constructing defensive portfolios, we should avoid such value traps and instead seek defensive varieties that are decoupled from the old economic cycle and have independent logic.

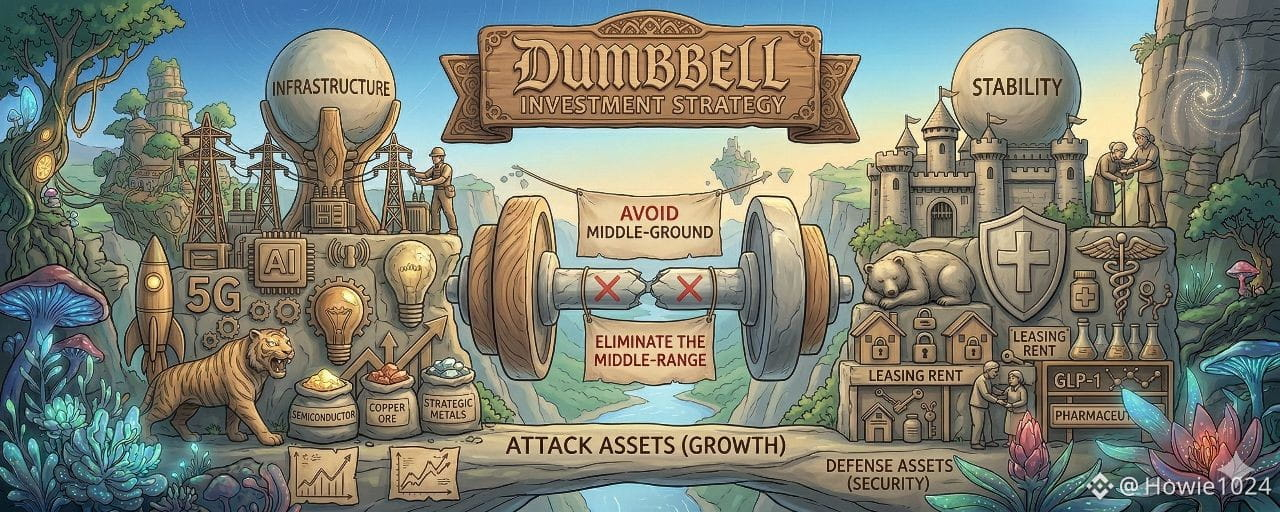

Chapter 3 Strategy: The Anti-fragile Structure of Barbell Configuration

Faced with the high uncertainty brought by the 'productivity paradox', a single style of risk exposure can easily lead to drastic fluctuations in the net value of the portfolio. We advocate adopting a 'barbell strategy', where the most certain offensive assets and the strongest independent defensive assets are allocated at both ends of the portfolio, abandoning mediocre assets in the middle to build an asymmetric reward-risk ratio.

On the offensive side, the core logic is to lock in the 'infrastructure' that cannot be bypassed in the new round of technological revolution. Before the 'productivity paradox' is resolved, the outbreak of application layers will take time, while the investment in the infrastructure layer is certain.

Energy and electricity systems: this is currently the track with the highest certainty. The essence of artificial intelligence is computing power, and the physical foundation of computing power is energy. Regardless of which tech company ultimately prevails, the property of data centers as 'electricity-consuming beasts' will not change. Therefore, independent power producers and grid equipment manufacturers that can provide stable electricity for high-density computing centers have extremely high allocation value.

Computing infrastructure: including semiconductor manufacturing, advanced packaging, and optical communication modules, etc. This is the 'shovel' of the digital economy, and its demand directly benefits from the increase in global capital expenditure.

Key strategic resources: such as industrial metals like copper. Benefiting from global grid upgrades and data center construction, its supply-demand gap has rigid support in the medium to long term.

On the defensive side, our screening criteria are to minimize correlation with macroeconomic fluctuations.

Healthcare track: The growth logic of this track stems from demographic characteristics rather than economic cycles. Specifically, two major directions can be focused on: first, the innovative drug industry chain for metabolic diseases represented by GLP-1 receptor agonists, whose market demand has surpassed the simple weight loss concept, showing application potential in areas such as cardiovascular diseases; second, medical services directly related to aging, such as professional nursing institutions and rehabilitation medical centers.

Housing demand: In the context of economic downturn and high interest rates, housing demand is shifting from 'purchase' to 'rental'. Rental housing assets with stable cash flow demonstrate excellent defensive properties.

Chapter 4 Timing: Finding Structural Opportunities Amid Giants' Wait-and-See

Recently, long-term value investors represented by Buffett have maintained record cash reserves, and this 'hands-off' posture has triggered widespread anxiety in the market. However, a deeper analysis of the logic behind it may provide us with different insights.

The giants' wait-and-see attitude mainly stems from two aspects: first, the valuation levels of major stock indices are still at historical highs, lacking sufficient safety margins; second, the uncertainty of the macroeconomic outlook, especially the absence of clear signals regarding when the 'productivity paradox' will be resolved. For institutions with massive funds, holding cash is a rational choice in the absence of clear right-side signals or extremely undervalued left-side prices.

However, this does not mean that retail investors can only passively wait. Unlike institutions, we have higher flexibility and can implement structured left-side layouts.

For the aforementioned core tracks on the 'offensive side' (such as energy and electricity) and the independent logic assets on the 'defensive side' (such as healthcare), the current market adjustment actually provides a window for phased building positions. The intrinsic value of these assets does not depend on short-term macroeconomic fluctuations, providing a safety cushion for left-side layouts.

For assets deeply bound to the old economic cycle and pseudo-AI applications that have not yet formed a commercial closed loop, we should remain cautious and wait for clear right-side signals before intervening.

Additionally, we can also pay attention to the lagging effects of changes in global liquidity. Historical data shows that the transmission of the growth of broad money supply to the prices of risk assets typically has a lag period of 6 to 12 months. This indicator may provide us with a more refined coordinate for judging market turning points.

Conclusion

Investment is not about seeking 100% precise predictions, but about finding relatively certain logic in an uncertain world. By identifying the 'productivity paradox', we penetrate the macro fog and position the current historical coordinates; by reconstructing the 'barbell strategy', we peel away the value traps of the old cycle and lock in the certainty increments of the new cycle. In the chaos and order at the intersection of the K-wave, only by adhering to logic and maintaining patience can we build an investment portfolio with asymmetric advantages and smoothly navigate through cycles.