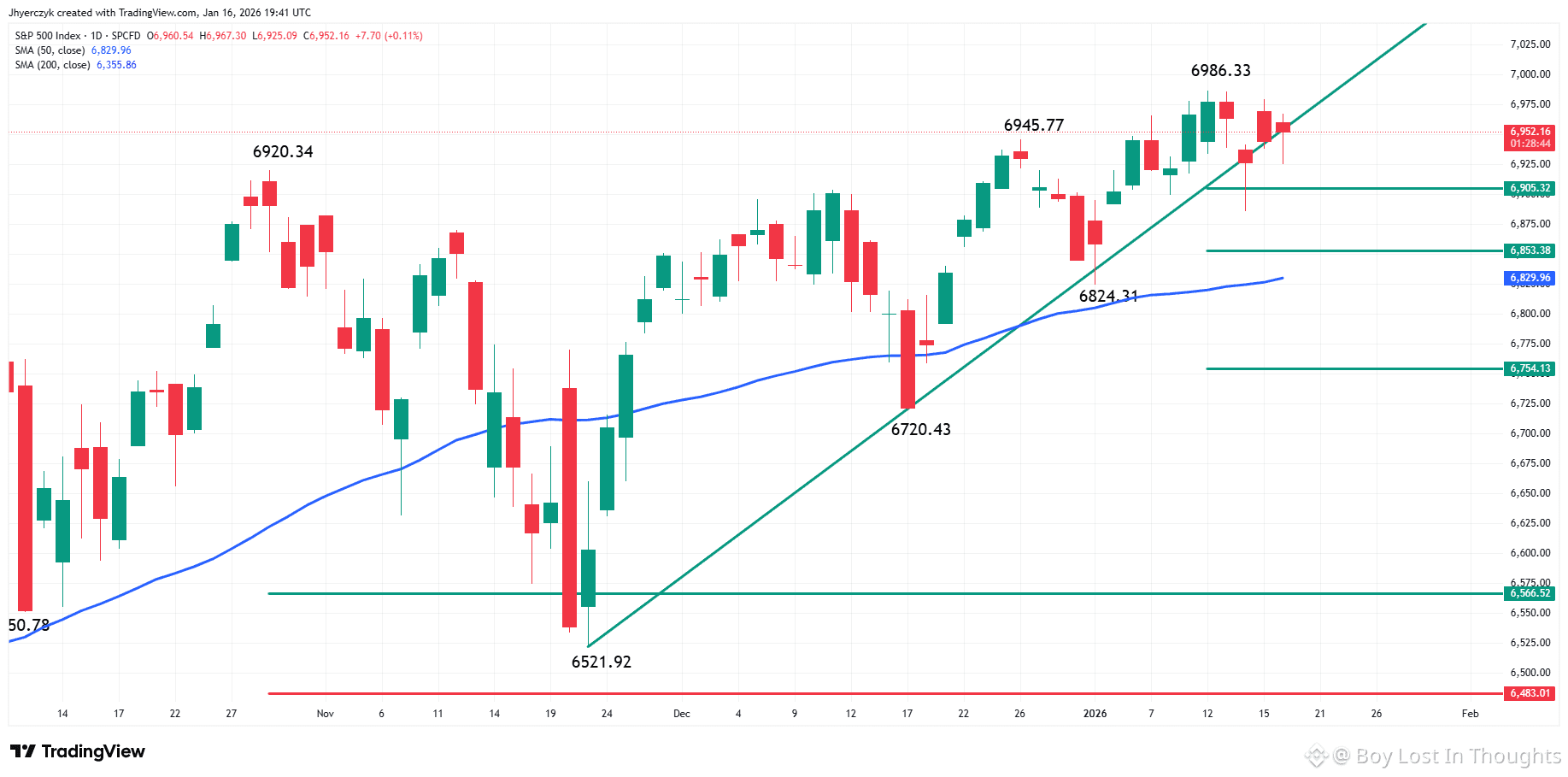

U.S. stocks are poised for a mixed close in thin, directionless trading ahead of the holiday weekend, with no clear market leader emerging. Early market weakness followed President Trump’s suggestion that he prefers Kevin Hassett remain in his current role rather than become the next Fed chair—triggering a mid-morning dip. Sentiment turned upward, however, as former Fed Governor Kevin Warsh emerged as the new favorite, seen by Wall Street as less inclined to cut rates.

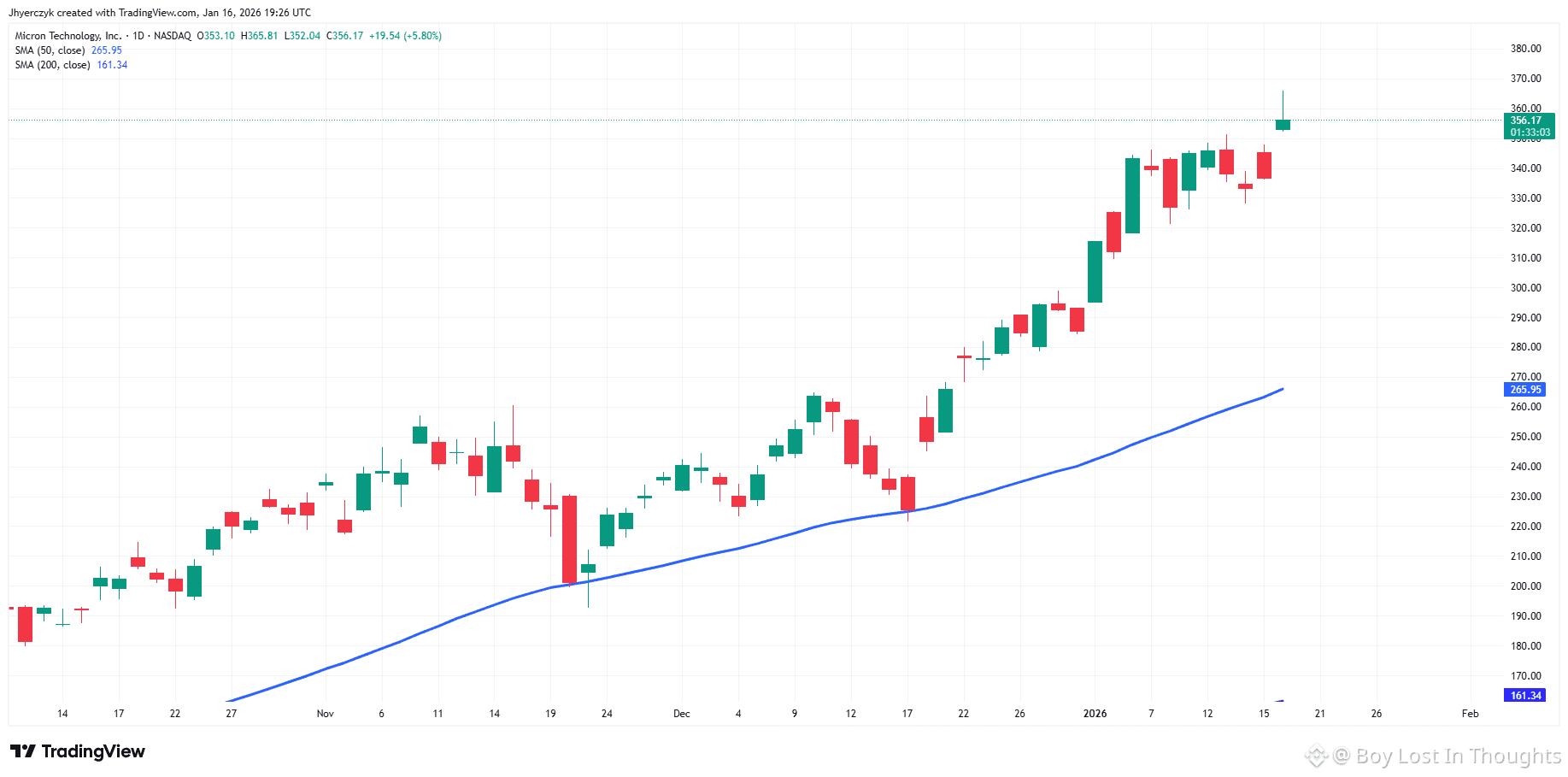

Tech and real estate sectors showed relative strength. Real estate led gains (+1.03%) as mortgage rates hit a three-year low, partly due to a recent Trump administration move directing $200 billion toward Fannie Mae and Freddie Mac bonds. Chipmakers like Micron (+5.6%) and Seagate (+2.2%) continued to ride AI-driven demand, supporting the tech sector.

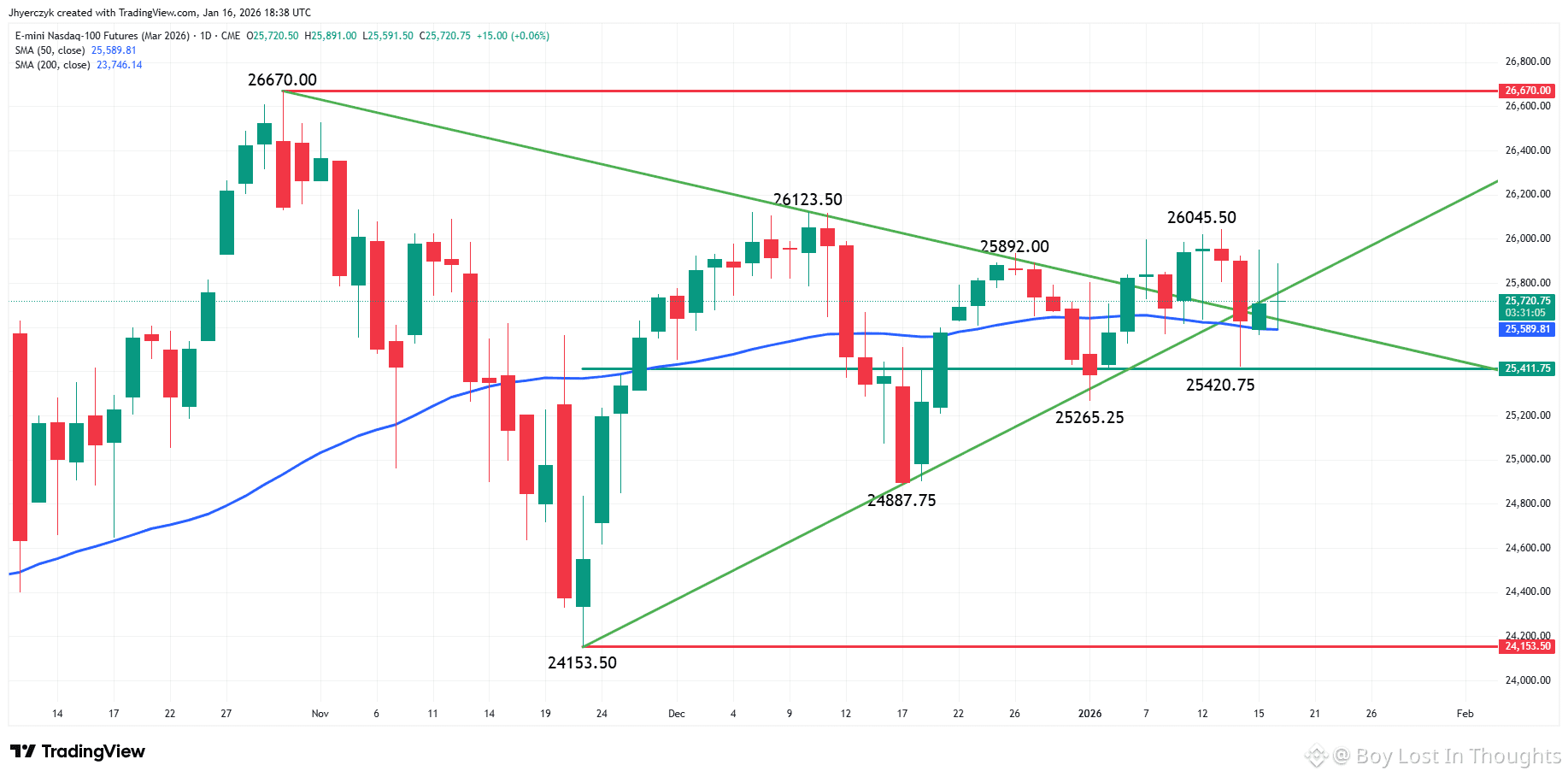

Technically, Nasdaq-100 futures hover near key trendlines—trading above a downtrend line but below an uptrend line—with the 50-day moving average serving as crucial support. A strong or weak closing tone will likely depend on whether the index reclaims the uptrend line or breaks below the 50-day average.

Volatility throughout the week has been largely driven by Trump’s statements—from Iran policy shifts to Fed leadership uncertainty—though his latest comments regarding Greenland drew little market reaction.

Key Points Highlighted:

Mixed, leaderless session ahead of a long weekend.

Trump’s Fed chair comments caused a mid-morning dip, then a reversal as Kevin Warsh became the new favorite.

Real estate sector outperformed amid falling mortgage rates and a $200B bond-buying directive.

Tech gains were led by chipmakers (Micron, Seagate) on strong AI demand.

Nasdaq-100 futures are balanced near key technical levels—watch the 50-day moving average for direction into the close.

Weekly volatility was heavily influenced by Trump’s remarks on Iran, the Fed, and other policy matters.