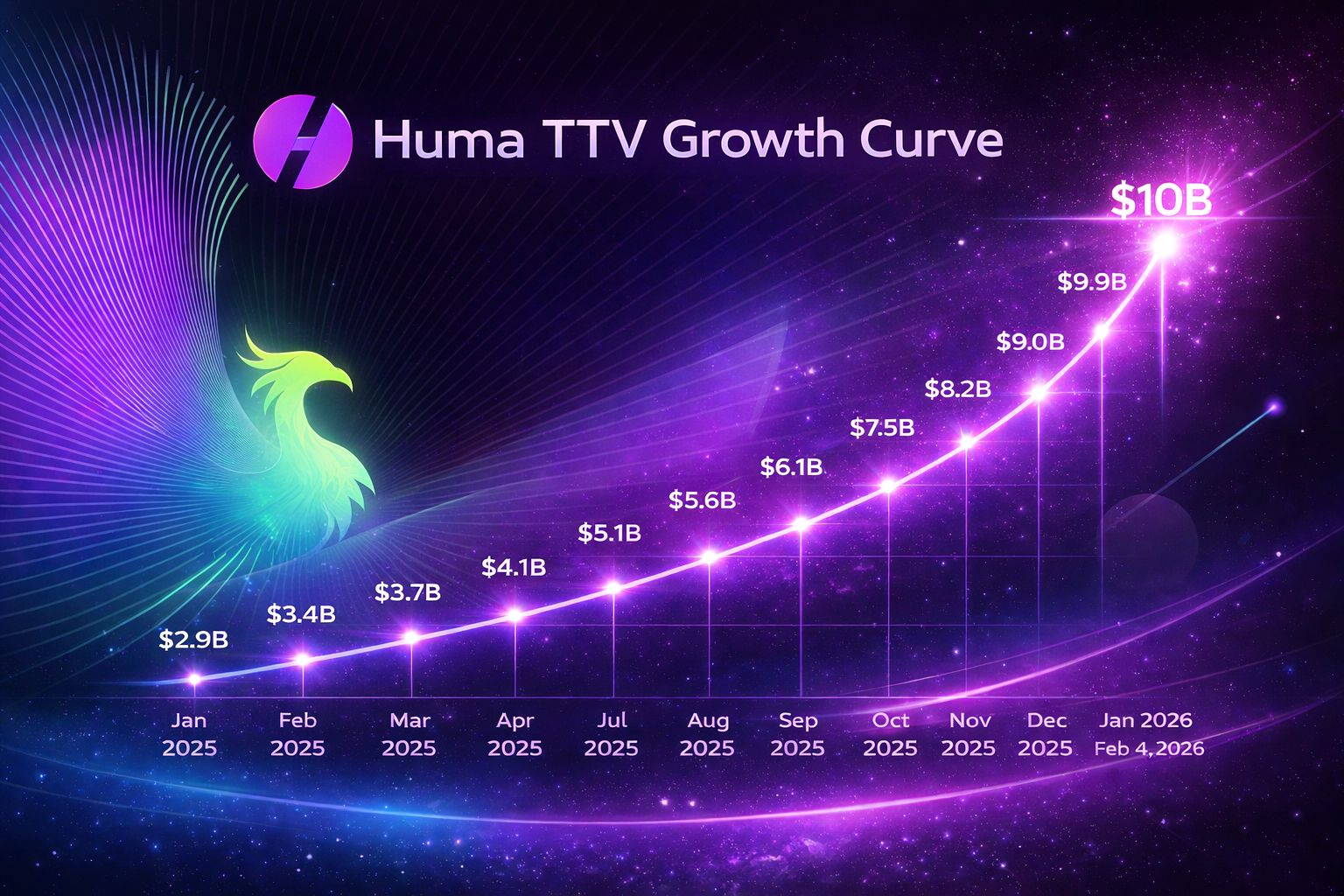

Huma crossed $10B in Total Transaction Volume.

Huma's Total Transaction Volume (TTV) has surpassed $10 billion.

$10 billion is really a lot!

According to Dune data, Huma @Huma Finance 🟣 TTV has seen significant growth since 2025, from $2.9 billion to over $10 billion. The growth curve shows that over time, it has become steeper, indicating that the growth rate is accelerating!

So, how was this $10 billion "刷" generated?

To explain this, one must first deeply understand the meanings of TTV and TVL.

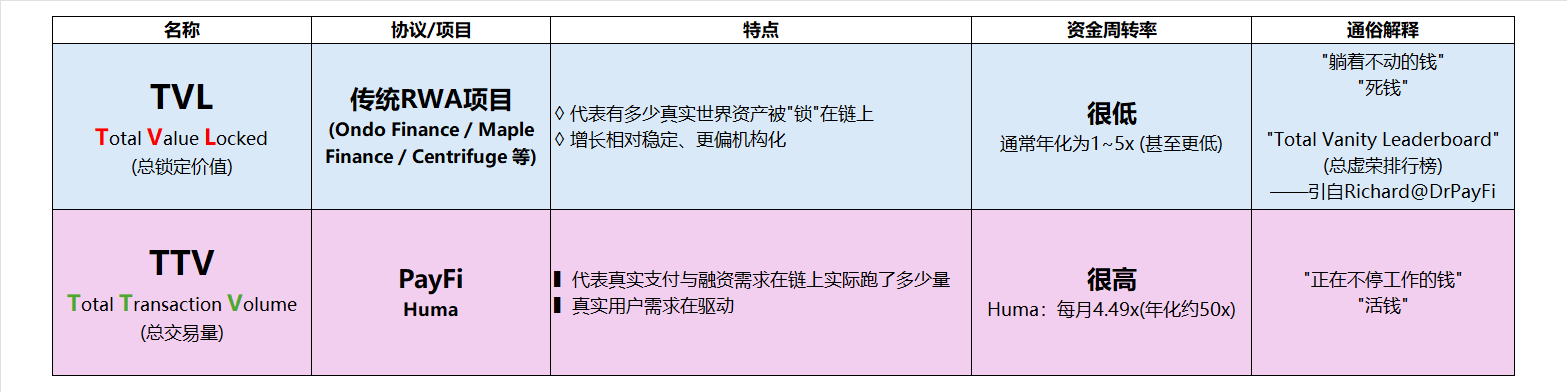

TTV = Total Transaction Volume (总交易量)

TVL = Total Value Locked

TVL

TVL is a traditional RWA protocol,

Like Ondo Finance / Maple Finance / Centrifuge, mainly reporting data,

◊ Represents how many real-world assets are "locked" on the chain

◊ Growth is relatively stable and more institutionalized

◊ The frequency of fund turnover is very low, usually annualized at 1~5x (or even lower)

◊ It's "idle money", "dead money"

So, this is also the reason Richard jokingly refers to it as the "Total Vanity Leaderboard".

TTV

TVL is the data that PayFi leader Huma focuses on.

▌ Represents how much real payment and financing demand has actually run on the chain

▌ Real user demand is driving

▌ Funds flow quickly, with a high turnover frequency,

According to Dune data, Huma's fund turnover rate—4.49x per month (annualized about 50x)

▌ It's "money that is constantly working", "living money"

Specifically regarding fund turnover rate, in one year,

Traditional RWA: Locked $1 ≈ contributes $1 TVL

Huma: High-frequency flowing $1 ≈ generates $100 TTV (about 50x)

It's like,

If you have 100,000 yuan, but it is locked in the bank account with poor liquidity, after a year, the TVL is still 100,000 yuan;

If you have only 10,000 yuan, but can keep borrowing/repaying, then borrowing/repaying again... and keep using it repeatedly like this, if you "rotate" 50 times within a year, the accumulated TTV can reach 1 million yuan!

This is why Huma can leverage about $150 million of TAL (Total Active Liquidity) to achieve over $10 billion TTV.

Therefore, Huma is "capable", with extremely high liquidity and turnover behind it, and the deeper reason comes from the demand driven by the real world—this can also be seen from Huma's PMF.

PMF, Product-Market Fit.

PMF was proposed by Silicon Valley venture capitalist Marc Andreessen in 2007, referring to providing products that meet market demand in a good market, and this concept has been defined as the only important core element for startups, emphasizing that the market environment has a decisive effect on product success.

Currently, Huma's PMF has been established, which can be confirmed from the following points:

★ Huma's product is already a necessity, solving the real pain points of cross-border payments.

★ Customers usually continue to use it continuously and periodically after trying it, with a high reuse rate.

★ Business growth is healthy and continues to rise, not relying on a large amount of incentives, 3.4x YoY is a good proof.

★ The global payment market is large enough, but the pain points of inefficiency have still not been effectively resolved.

★ Has established deep cooperation with major partners (Circle, Obligate, etc.)

In other words, Huma has far surpassed the early PMF stage and has entered a strong PMF stage.

This also means that Huma's deep liquidity has taken shape, and more and more real-world payment flows are being routed through Huma's infrastructure, which is a great reflection of Huma leading the PayFi wave and being a leader in the PayFi track.

But,

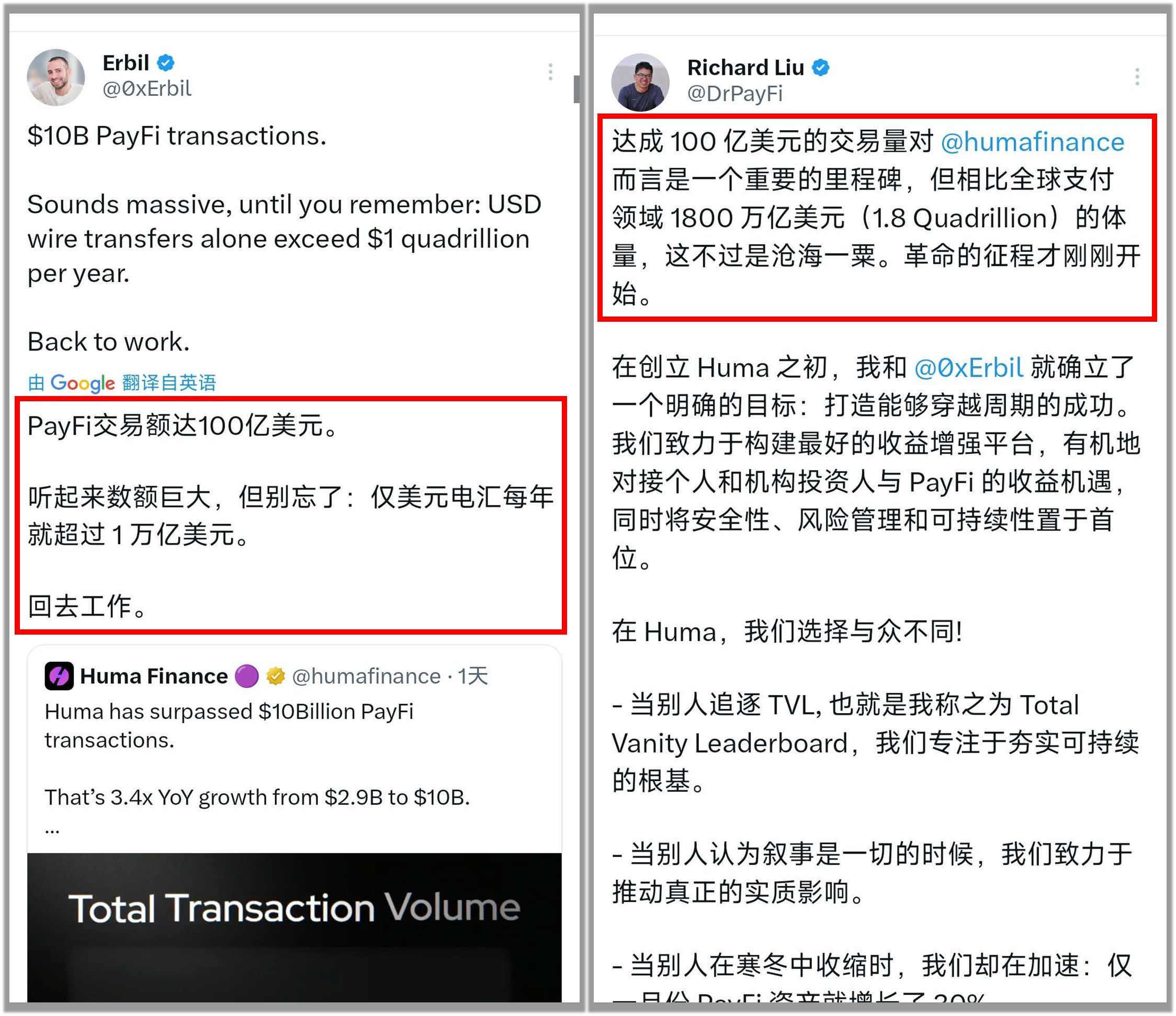

10 billion dollars is really not much!

The co-founders Erbil and Richard appear quite calm about Huma TTV breaking $10 billion.

Huma's TTV has exceeded $10 billion, with the global payment market at $180 trillion,

A drop in the ocean,

A drop in the ocean!

(Sorry, Curly Hair Bro 😼🙏)

So, $10 billion is really not much...

Fortunately, this market is big enough, and the "stage" is large enough— the bigger the stage, the bigger the ambition!

Jack Ma once said: If banks don’t change, we will change banks.

Huma is also shouting and putting into action: using PayFi to change traditional finance.

Do you remember the personal experience shared by Erbil on CatLumpurr?

It took 3 months, and I still couldn’t transfer the legal funds in the Turkish account to the U.S. account...

Look, these are the "good things" done by traditional finance:

✖️ Asset locking, locking liquidity

✖️ Payment completed, arriving T+N, N≠0

✖️ Payments and financing are completely separated

……

How can PayFi break the deadlock?

Bringing financing to the moment payment occurs— in the PayFi system, when real payment is triggered, the protocol instantly evaluates its risk and credit, and liquidity is synchronously released on the chain, meaning users receive usable funds on the spot, with no waiting period or billing period.

In PayFi, the speed of funds = the speed of transactions, completely changing the drawbacks of traditional RWA where assets are static and funds are hardly moving, allowing RWA to undergo a qualitative change from simple asset mapping to real-time liquidity and real-time settlement cash flow assets.

So, what exactly is PayFi?

The answer is simple:

PayFi is Freedom.

PayFi is freedom.