A growing narrative suggests Bitcoin may have bottomed. While price stabilization and short-covering rallies are visible, the key is not the rebound itself but understanding what drove the past six months and what is required to reach a new all-time high.

Bitcoin is a “terminal liquidity asset” in a hierarchical financial system where capital flows from central banks to bonds, equities, and finally crypto. Over the past six months, this upstream flow weakened. Elevated U.S. rates, a stronger dollar, and rising Japanese bond yields tightened global liquidity. As one of the largest external investors, Japan’s shift reduced capital available to global markets, limiting inflows into crypto. The issue was not demand destruction, but that capital never reached BTC.

At the same time, a structural deleveraging occurred. Excess leverage in derivatives markets led to cascading liquidations, consuming future demand and amplifying downside pressure. This was not a spot-driven sell-off but a credit contraction event.

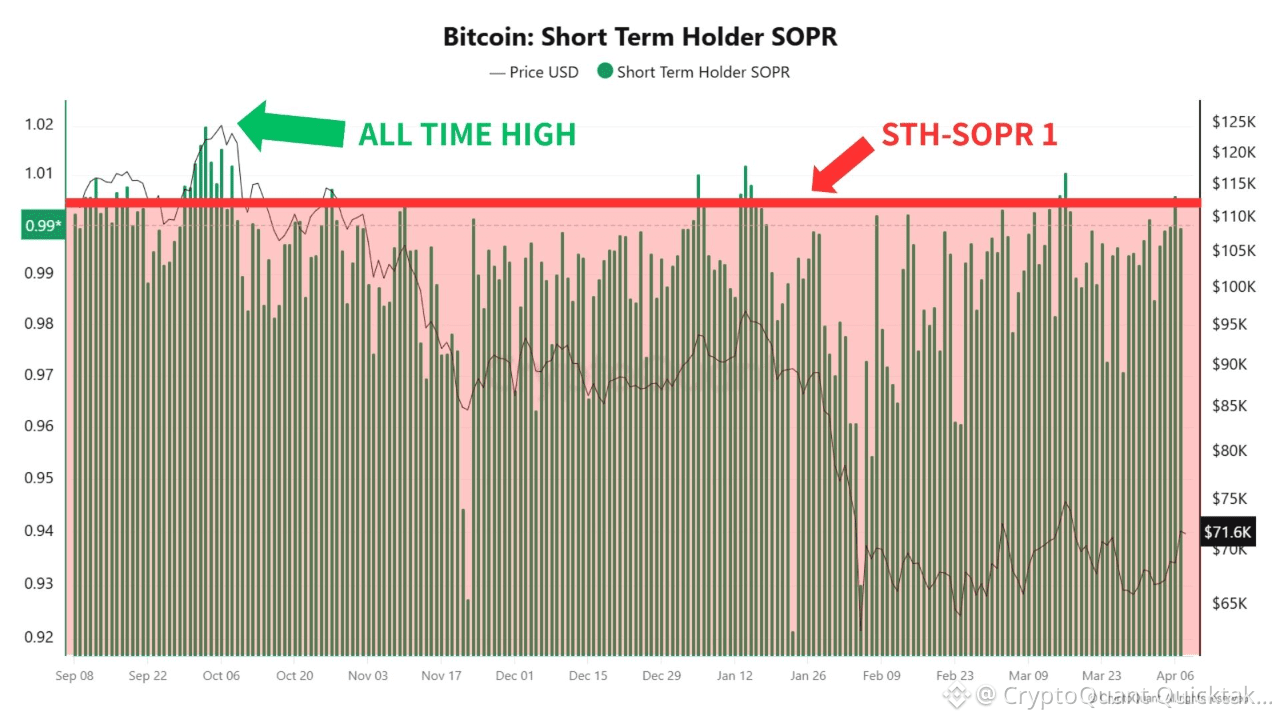

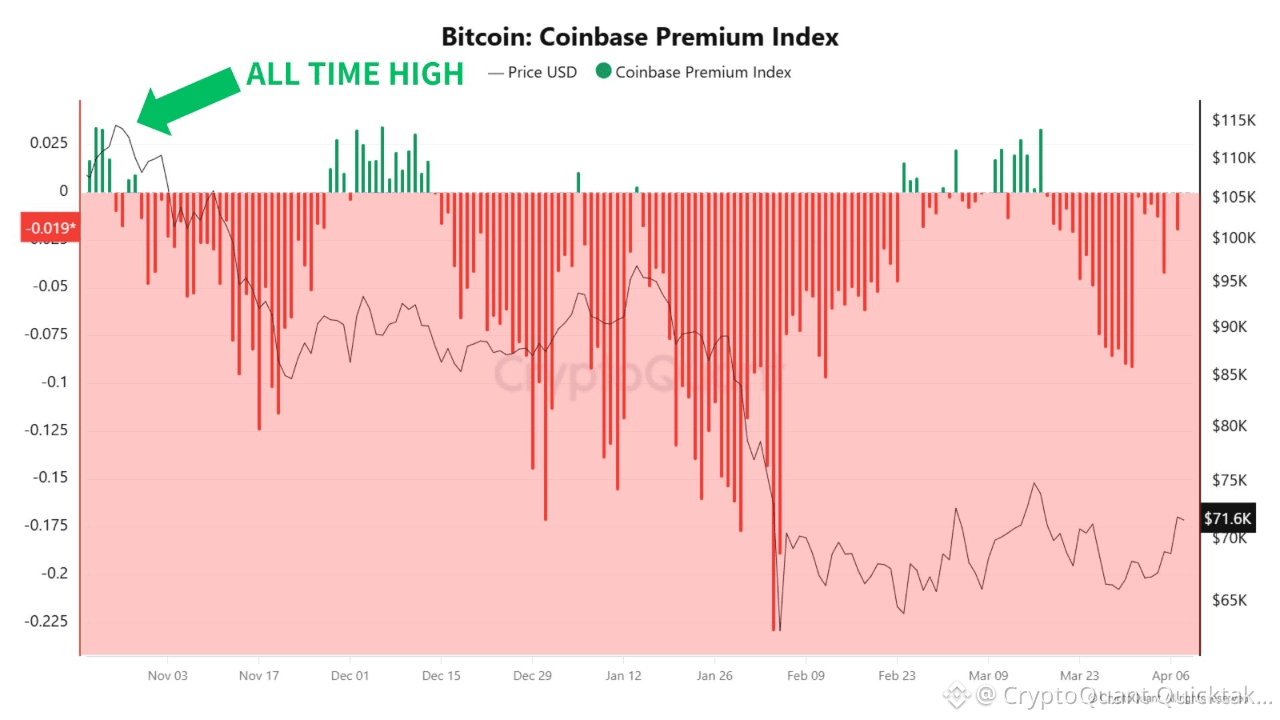

On-chain indicators confirm this structure. STH-SOPR remained below 1, signaling sustained loss realization among short-term holders, while the Coinbase Premium Gap stayed negative, reflecting weak U.S. spot demand. These are not causes, but outcomes of deeper liquidity constraints.

For Bitcoin to reach a new ATH, capital must flow back through the system. This depends on macro and policy shifts. The U.S. midterm elections may influence fiscal expansion and rate expectations, while potential Bitcoin ETF approval in Japan could open a new capital channel. With vast household assets, Japan represents a structural shift in access, not just incremental demand.

Ultimately, the past six months were not a failure of Bitcoin, but a reflection of global liquidity tightening. The next rally will not be driven by technicals or narratives, but by whether capital can once again reach the edge of the financial system.

Written by XWIN Research Japan