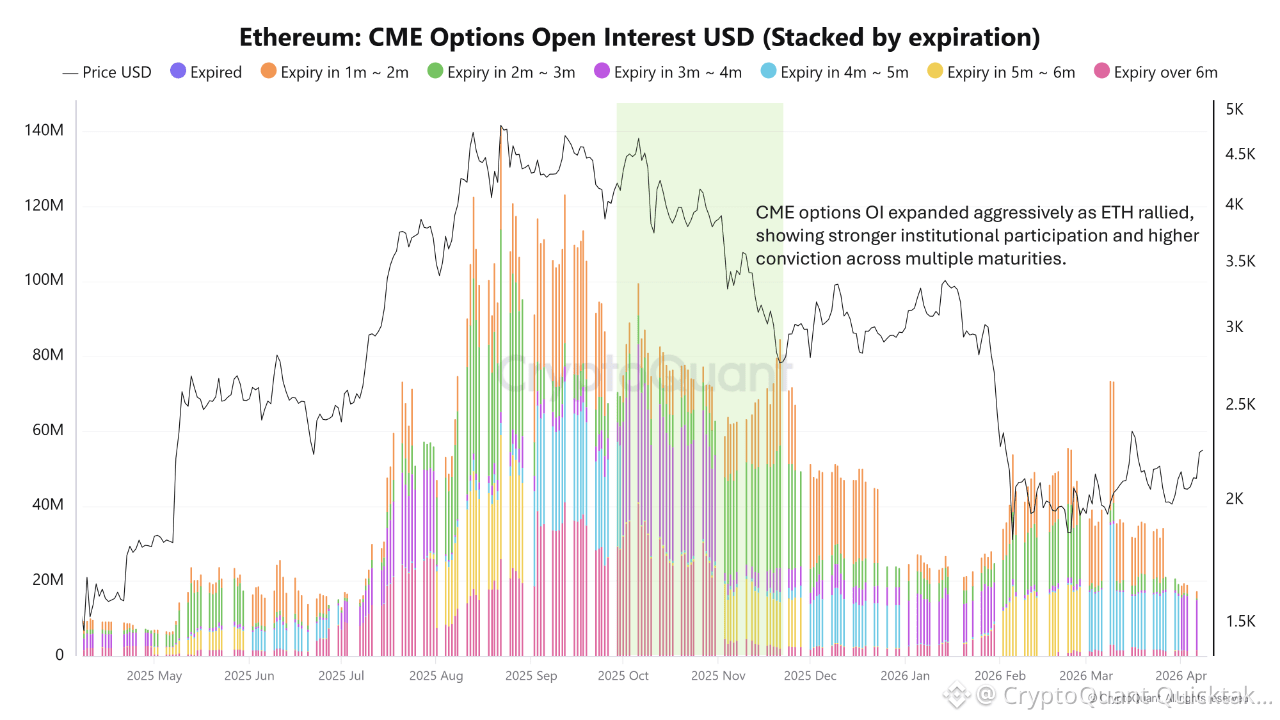

Open interest built aggressively into the August–October 2025 window, with layered exposure across multiple maturities and a total profile that at times exceeded $100 million. Since then, that structure has cooled sharply. Near-dated exposure remains, but the longer-dated stack is now much thinner and visibly less confident than during ETH’s stronger phase.

This matters because institutional conviction is often expressed not only through outright futures or spot buying, but through the willingness to hold optionality further out on the curve. A lighter long-dated options structure signals reduced confidence in a strong medium-term upside path.

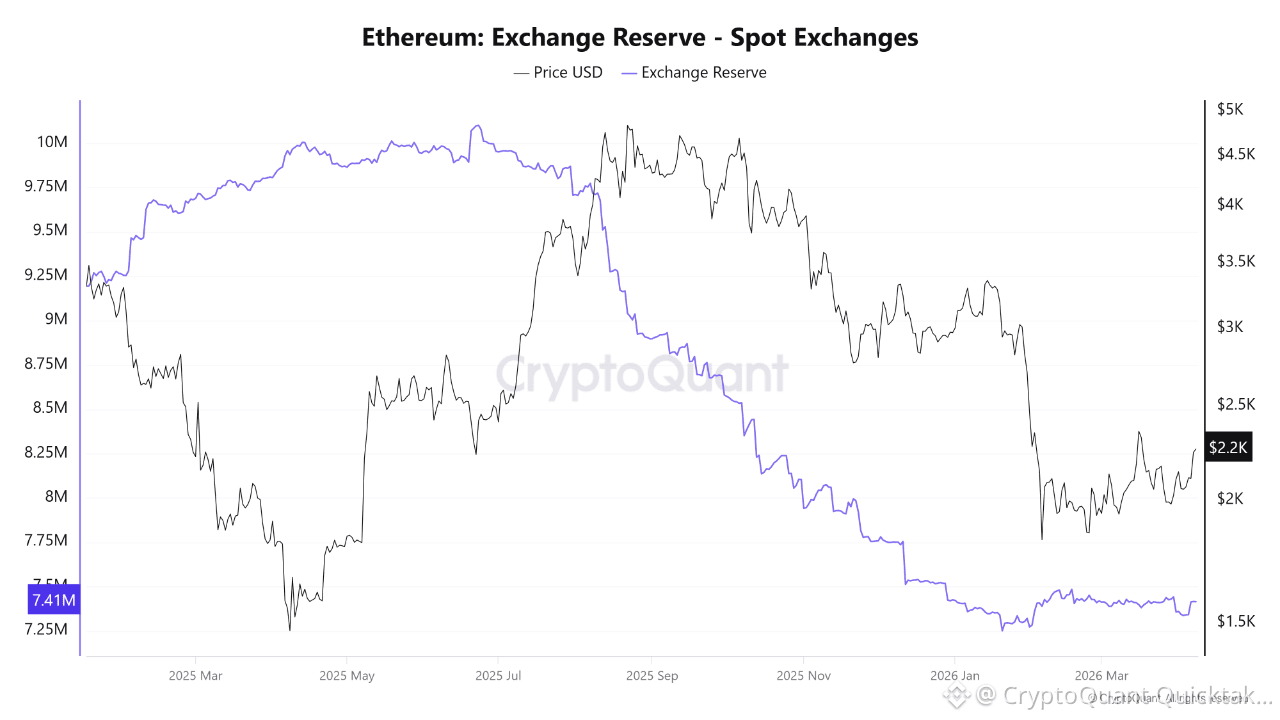

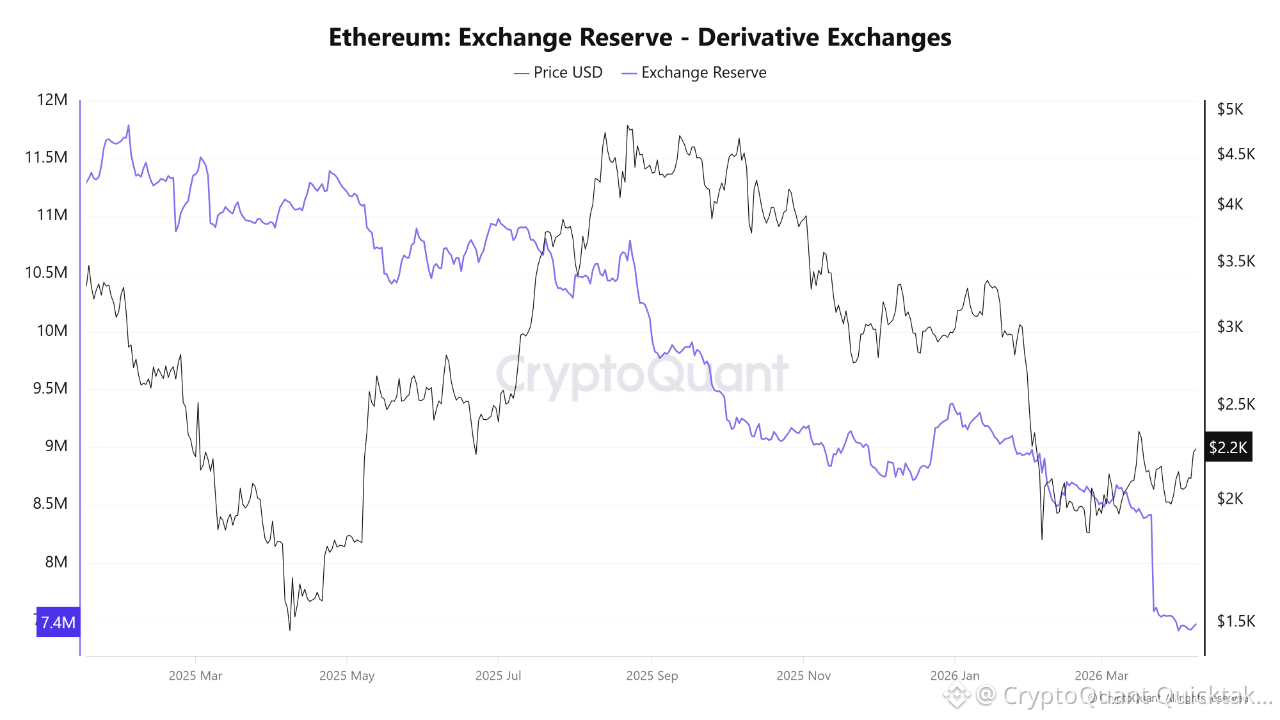

Spot exchange reserves have fallen to around 7.41 million ETH, while derivative exchange reserves have also declined to roughly 7.4 million ETH. This marks a broad drawdown across both spot and leveraged venues. In a healthier market structure, that kind of synchronised reserve contraction would typically support stronger price discovery by reducing immediately available inventory across the ecosystem.

Instead, ETH has remained fragile. That implies the problem is not simply excess supply. The deeper issue is the quality of demand.

Bitcoin can stay resilient in a cautious macro environment because investors still treat it as the cleaner reserve asset within crypto. Ethereum, by contrast, needs higher-quality demand to outperform. It requires conviction around real usage, sustained institutional flows, or a stronger risk-on backdrop.

Right now, the flows do not show that. They show an asset being withdrawn from exchanges, lightly supported by positioning, but not embraced with enough force to reclaim leadership.

Until ETH sees stronger spot-led demand and a more robust institutional bid, its structural underperformance versus Bitcoin is likely to persist.

Written by Novaque Research