The Federal Reserve just cut interest rates, and the market gave a harsh response, with Bitcoin crashing to around $85,600, and Ethereum even falling below the $3,000 mark, dragging down crypto-related stocks: Strategy and Circle fell nearly 7% in a single day, Coinbase dropped over 5%, and mining companies like CLSK and HUT suffered even more, with declines exceeding 10%. This wave of declines is not coincidental; the core issues are all macro-level problems, compounded by on-chain funds collectively fleeing, making it very difficult to stop the decline.

Yen Rate Hike: The Underestimated 'Trigger for a Crash'

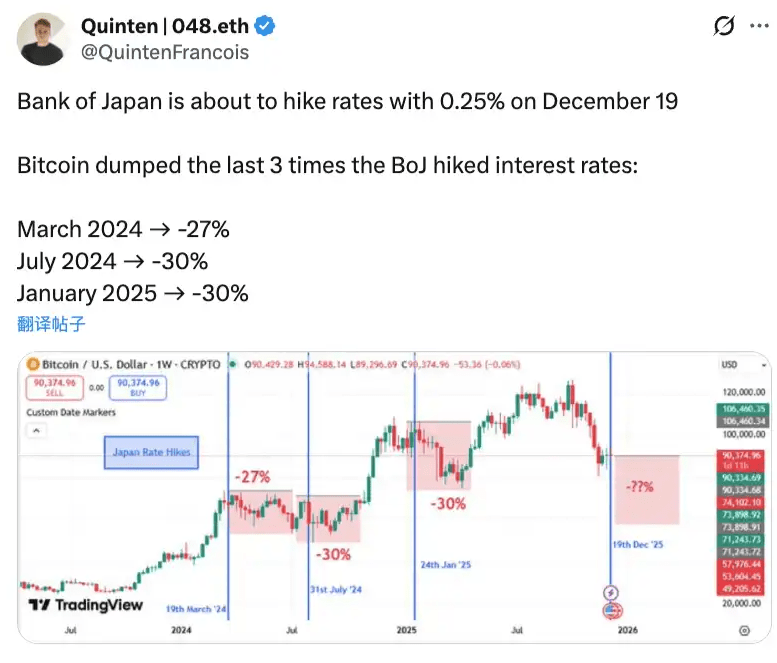

The number one culprit behind this wave of decline is definitely the expectations of rate hikes from the Bank of Japan; this could be the last 'black swan' in the financial world this year, but the market has already started to react early.

Historical data shows this: In the past three rate hikes by the Bank of Japan, Bitcoin has not escaped unscathed, with a guaranteed decline of 20%-30% within 4-6 weeks. In March 2024, it fell 27%, in July it fell 30%, and after the rate hike in January 2025, it fell 30%. This time, it is the first rate hike since January 2025, with rates possibly reaching a 30-year high. Currently, the market predicts a 97% probability of a 25 basis point rate hike, which is basically a done deal; the meeting is just a formality.

Why does the yen rate hike have such a significant impact? Many have underestimated its destructive power. Japan is the largest foreign holder of U.S. Treasury bonds, with holdings exceeding $1.1 trillion, and the yen is the largest currency player after the dollar, possibly having more influence than the euro. The near 30-year bull market in U.S. stocks has been supported by yen arbitrage, as investors borrow yen at low interest rates to buy high-yield assets like U.S. stocks, U.S. bonds, and cryptocurrencies. Now that Japan has raised interest rates, these arbitrage positions must be closed quickly, leading to forced liquidations + deleveraging, and the crypto market naturally suffers as a result.

Why does the yen rate hike have such a significant impact? Many have underestimated its destructive power. Japan is the largest foreign holder of U.S. Treasury bonds, with holdings exceeding $1.1 trillion, and the yen is the largest currency player after the dollar, possibly having more influence than the euro. The near 30-year bull market in U.S. stocks has been supported by yen arbitrage, as investors borrow yen at low interest rates to buy high-yield assets like U.S. stocks, U.S. bonds, and cryptocurrencies. Now that Japan has raised interest rates, these arbitrage positions must be closed quickly, leading to forced liquidations + deleveraging, and the crypto market naturally suffers as a result.

What’s more critical is that this rate hike itself isn’t the scariest part; the focus is on the policy signals for 2026. The Bank of Japan has already stated that it will begin selling about $550 billion in ETF holdings starting January 2026. If interest rates continue to rise next year, more arbitrage trades will need to be unwound, and the return of Japanese yen + risk asset sell-offs will continue to impact the market; unless there is a pause after the rate hike, perhaps we could see a rebound after a flash crash, but such luck is hard to come by.

The Federal Reserve's interest rate cuts are 'loud thunder but little rain'; uncertainty is the most grinding.

The Federal Reserve just finished lowering interest rates, and the market is already starting to wonder: How many more times can rates be cut in 2026? Will the cuts become slower? This uncertainty is more damaging than clear tightening policies.

This week, two key data points are to be released, directly determining the direction of interest rate cut expectations: the non-farm payroll report at 21:30 tonight, and the CPI data on December 18. The market currently expects the employment situation to be pessimistic, which superficially seems 'bullish for rate cuts,' but conversely: if employment cools too quickly, will the Federal Reserve be afraid of an economic stall and hesitate to ease? If there really is a 'cliff-like cooling,' they might choose to wait and see.

CPI data is more important; everyone is guessing: if inflation rebounds, will the Federal Reserve shout about rate cuts while speeding up balance sheet reduction to withdraw liquidity? After all, the situation in Japan is tightening, and the Federal Reserve needs to find balance; it could lead to 'nominal easing, but actual tightening.' Moreover, the next certain rate cut won’t happen until at least January 2026; currently, Polymarket predicts a 78% probability of maintaining the interest rate in January, with only a 22% probability of a rate cut, making the variables too large.

What’s worse is that global central bank policies are all in disarray: Japan is hiking rates, the Federal Reserve is hesitant, and the European Central Bank and the Bank of England are waiting and watching. This fragmented approach is a 'liquidity nightmare' for Bitcoin, with no unified easing environment; funds are reluctant to enter the market, so the decline naturally cannot stop.

The mine is closing + Old money is running away, the selling pressure on-chain simply cannot stop.

With macro conditions not supportive and on-chain funds continuing to flee, this wave of decline is even more exacerbated.

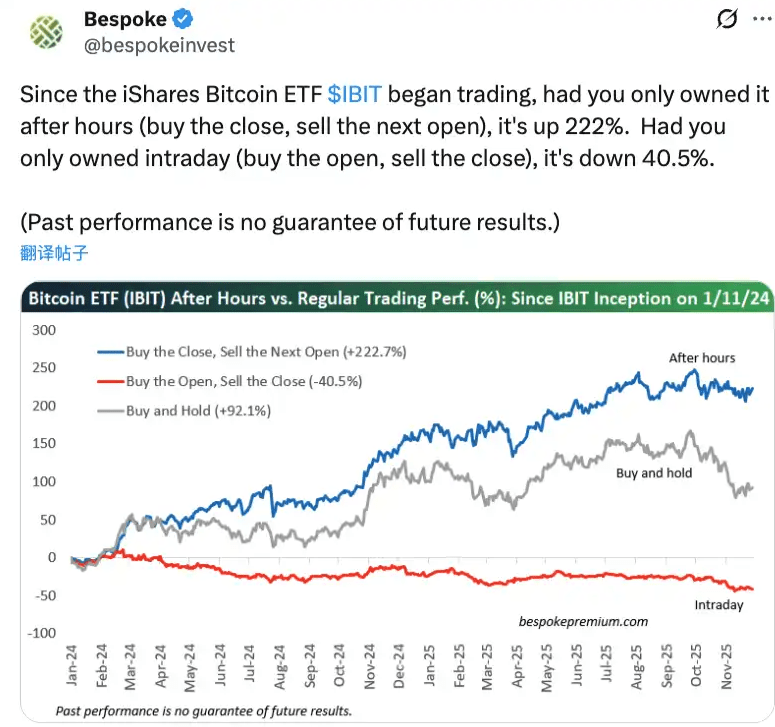

First, let's look at ETF institutions: Bitcoin spot ETFs saw a net outflow of about $350 million in a single day (nearly 4,000 BTC), with Fidelity's FBTC and Grayscale's GBTC/ETHE being the main outflow sources. Ethereum ETFs also didn’t perform well, with a cumulative net outflow of $65 million (about 21,000 ETH). There's an interesting data point: since BlackRock's IBIT was launched, holding after the close can earn 222%, but holding during trading hours instead results in a loss of 40.5%, showing how fierce the selling pressure is during U.S. trading hours.

On-chain signals are more direct: On December 15, net inflows to Bitcoin exchanges were 3,764 BTC (about $340 million), reaching a peak for the period. Binance alone had a net inflow of 2,285 BTC, which is eight times the previous amount, clearly indicating that large holders are concentrating their deposits in preparation for selling. Market makers are also on the move; Wintermute transferred over $1.5 billion in assets from late November to early December. Although they recently slightly increased their BTC holdings, the behavior of large transfers has already triggered market panic.

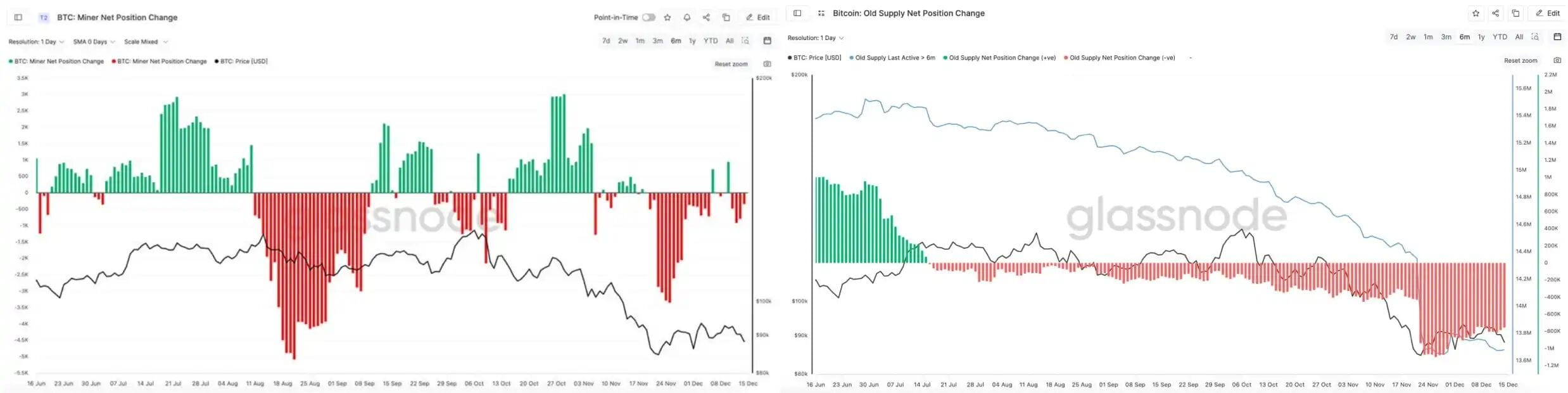

Long-term holders and miners are also 'voting with their feet.' Glassnode data shows that the OGs who haven’t moved their holdings in the past six months have continued selling for several months, accelerating after late November, with over 800,000 BTC sold in the past 30 days, reaching a new high since January 2024.

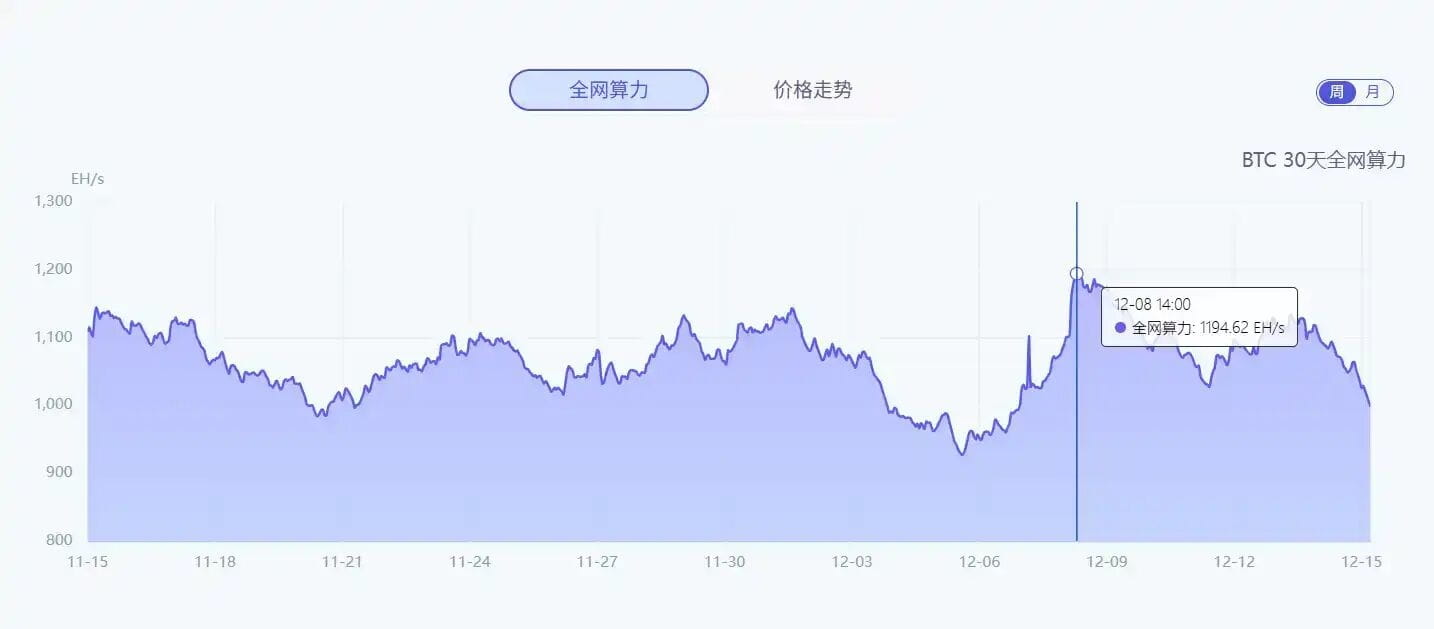

Miners are suffering even more, with the total network hashrate dropping 17.25% in a week, now only at 988.49 EH/s. Nano Labs founder Kong Jianping stated that based on a calculation of 250T per machine, at least 400,000 mining machines have shut down. The rumors of Xinjiang mining farms closing further confirm this point; miners under pressure naturally need to sell coins to raise funds, increasing the selling pressure further.

Miners are suffering even more, with the total network hashrate dropping 17.25% in a week, now only at 988.49 EH/s. Nano Labs founder Kong Jianping stated that based on a calculation of 250T per machine, at least 400,000 mining machines have shut down. The rumors of Xinjiang mining farms closing further confirm this point; miners under pressure naturally need to sell coins to raise funds, increasing the selling pressure further.

Ultimately, this round of Bitcoin's decline is not caused by a single factor: the rate hikes from Japan triggered the unwinding of arbitrage positions, the expectations of rate cuts from the Federal Reserve are unclear, and combined with on-chain institutions, old holders, and miners collectively reducing risk, multiple pressures have stacked up, and the downward trend is not over yet. Thinking about bottoming out now is likely to catch a falling knife; it’s better to wait for macro signals to clarify and for the on-chain selling pressure to stop before making a move.

Ultimately, this round of Bitcoin's decline is not caused by a single factor: the rate hikes from Japan triggered the unwinding of arbitrage positions, the expectations of rate cuts from the Federal Reserve are unclear, and combined with on-chain institutions, old holders, and miners collectively reducing risk, multiple pressures have stacked up, and the downward trend is not over yet. Thinking about bottoming out now is likely to catch a falling knife; it’s better to wait for macro signals to clarify and for the on-chain selling pressure to stop before making a move.