As the Christmas holidays approach, global financial markets enter the traditional 'Christmas rally' period. However, during this seemingly calm trading week, a series of major events will determine the direction of the market at the year's end.

Will Trump announce the nominee for the Federal Reserve Chair during the Christmas period, becoming the focus of the market? Current predictions show that Kevin Hassett, Director of the National Economic Council, has a nomination probability of about 54%, former Federal Reserve Governor Kevin Walsh about 21%, and Federal Reserve Governor Christopher Waller about 14%.

At the same time, the U.S. third-quarter GDP data will test the effectiveness of previous interest rate cuts, while Bank of Japan Governor Kazuo Ueda's speech may provide clues for Japan's monetary policy in 2026.

I. Christmas Market

I. Christmas Market

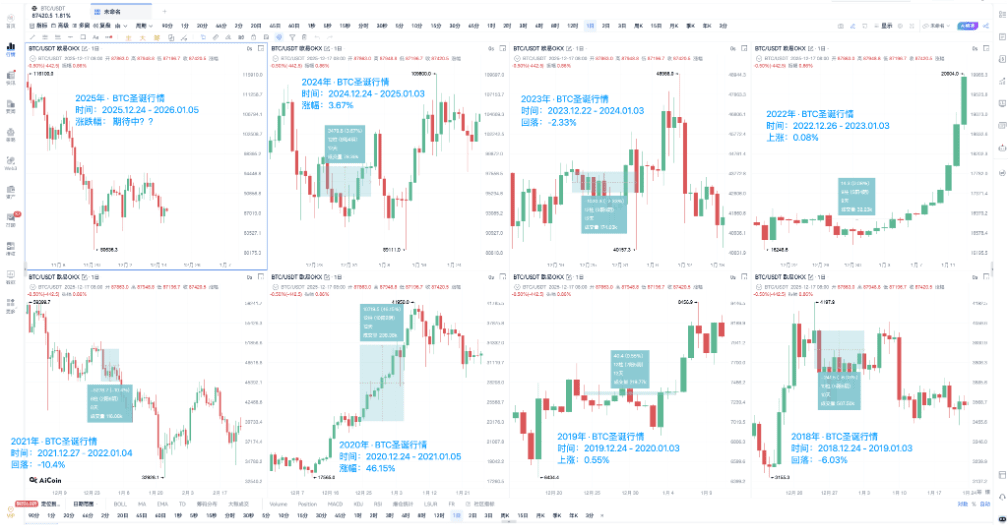

Looking back at Bitcoin's Christmas market history, data reveals the truth of this seasonal phenomenon. Over the past seven years, Bitcoin's performance during Christmas has shown a high degree of divergence, with the probabilities of rising and falling being roughly equal, and the probability of rising being about 57%. The performance of BTC during the last 7 complete Christmas-New Year cycles (roughly from around December 24 to January 3-5 of the following year):

● 2024 (2024.12.24 → 2025.01.03):+3.67%(slight increase)

● 2023 (2023.12.22 → 2024.01.03):-2.33%(slight decline)

● 2022 (2022.12.26 → 2023.01.03):+0.08%(basically flat)

● 2021 (2021.12.27 → 2022.01.04):-10.4%(significant decline)

● 2020 (2020.12.24 → 2021.01.05):+46.15%(super increase)

● 2019 (2019.12.24 → 2020.01.03):+0.55%(slight increase)

● 2018 (2018.12.24 → 2019.01.03):-6.03%(slight decline)

II. The Power Struggle for Leadership of the Federal Reserve

II. The Power Struggle for Leadership of the Federal Reserve

The nomination of the Federal Reserve Chair is undoubtedly the focus of the global market this week. Whether the Trump administration will announce the nominee during the Christmas period has become a hot topic of discussion in the market. Currently, the policy tendencies of the three main candidates vary, which may lead to different directions in monetary policy.

● Kevin Hassett, as the Director of the National Economic Council, has close ties with the Trump administration, and the market expects his nomination may lead to Federal Reserve policies that are more aligned with the government's economic goals.

● Former Federal Reserve Governor Kevin Warsh is known for his hawkish stance, and if he is nominated, it may imply a quicker shift towards tightening monetary policy.

● Currently, the Federal Reserve Governor Christopher Waller is viewed as a centrist, and his nomination may imply policy continuity.

This leadership change coincides with a critical moment for the U.S. economy. Since the Federal Reserve began cutting rates, the market has been closely monitoring the effects of the policy, and the monetary policy philosophy of the new chair will directly influence the interest rate path in 2026.

III. U.S. Economic Checkup Report

The preliminary annualized quarterly rate of real GDP for the third quarter to be announced on Tuesday is an important test of the effects of previous interest rate cuts.

● The preliminary quarterly real personal consumption expenditures for the third quarter can reflect the health of the consumption sector, which accounts for about 70% of the U.S. economy. The core PCE price index's annualized preliminary quarterly rate is the inflation indicator most closely watched by the Federal Reserve, directly related to future interest rate decisions.

● The release of this data was delayed due to the U.S. government experiencing a 43-day shutdown. Last week, the U.S. unemployment rate for November rose to 4.6%, the highest level since September 2021. The investment community is eager to judge from this data whether the signs of economic slowdown provide space for the Fed to further cut interest rates.

● The market currently shows a divergence of 'soft data turning hard, hard data turning soft.' The University of Michigan Consumer Confidence Index has rebounded from a low of 52.2 in April. However, actual economic data such as retail sales and structural issues in the labor market show signs of weakness.

IV. Canadian Monetary Policy Outlook

On Wednesday, the Bank of Canada will release the minutes of its monetary policy meeting to provide the market with more clues about the country's economic outlook and policy direction.

● The Bank of Canada maintained its target overnight rate at 2.25% during the December 2025 meeting. The central bank indicated in October that the policy rate is generally appropriate. This position has been maintained against the backdrop of third-quarter GDP growth of 2.6% and improvement in the labor market.

● Regarding inflation, the October CPI has slowed to 2.2%, but core inflation indicators remain in the range of 2.5% to 3%. Decision-makers point out that global uncertainty persists, and tariff pressures and unstable trade may continue to lead to quarterly fluctuations in GDP.

● If inflation and economic activity are roughly consistent with the October forecast, the management committee believes the current policy rate can keep inflation around 2%. Citigroup economists expect the Bank of Canada to maintain rates and policy guidance unchanged in the short term.

V. Japan's Monetary Policy Shift

● Bank of Japan Governor Kazuo Ueda will deliver a speech at the Japan Business Federation on Thursday, and the market is eager to gain insights into the direction of Japan's monetary policy for 2026.

● The background of Ueda's speech is quite significant. Last week, the Bank of Japan just raised the benchmark interest rate by 25 basis points to 0.75%, the highest level in 30 years. Ueda stated that this decision is based on the increasing likelihood of achieving economic outlook.

● The market is particularly focused on this speech, as Japan remained inactive after the new Prime Minister Suga Yoshihide took office until last week when it resumed rate hikes. At the same time, Japan will also announce the unemployment rate data for November, providing more basis for assessing economic conditions.

VI. U.S. Labor Market and Tariff Impact

The number of initial jobless claims in the U.S. for the week ending December 20, to be announced on Wednesday, is a high-frequency indicator for observing the health of the labor market. While the surface data is acceptable, there are structural issues in the employment market.

● Although 147,000 new non-farm jobs were added in June, half of them came from government hiring, and the private sector's job creation capacity is relatively limited. The impact of tariff policies on the employment market is gradually becoming evident.

● The impact of tariff shocks on the economy shows phase characteristics. The investment side has already begun to show signs of fatigue, and businesses are generally adopting cautious strategies in the face of policy uncertainty, cutting back on capital expenditures.

● The impact on the consumption side is expected to gradually become apparent in the second half of the year, as the negative effects of tariff policies on corporate production costs, job positions, and income levels transmit to the labor market, potentially further impacting household consumption capacity.

Global markets are holding their breath for the announcement of the Federal Reserve Chair nomination, and traders have prepared for various possibilities. If Hassett is nominated, the market may expect more accommodative monetary policy; if Warsh wins, they need to be ready for a potentially more hawkish policy shift.

U.S. third-quarter GDP and personal consumption data will visually demonstrate economic health. Even if the data is robust, the market still needs to pay attention to whether consumption growth is sustainable and whether the core PCE price index is approaching the Fed's 2% target.

As Christmas approaches, global financial markets will enter the new year of 2026 with these economic data and policy signals after a brief market closure.

Join our community to discuss and become stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX benefit group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance benefit group: https://aicoin.com/link/chat?cid=ynr7d1P6Z