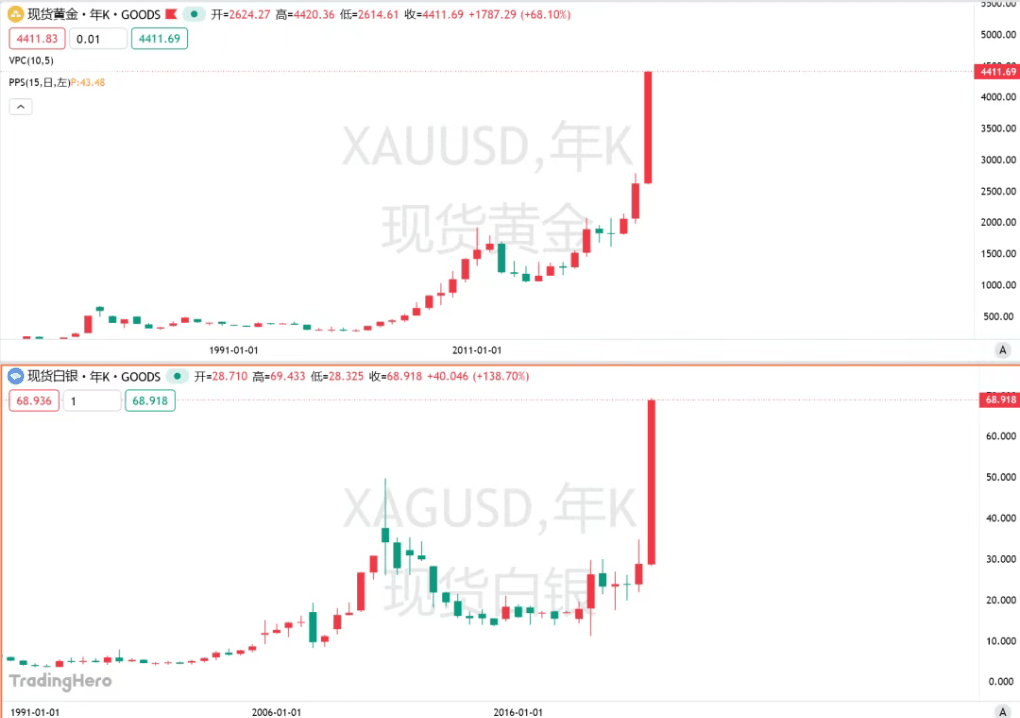

On December 22, 2025, the global precious metals market witnessed history. The spot gold price in London broke the $4400 per ounce mark for the first time, while the spot silver price also stood above $69. As of that day, gold had increased by approximately 68% for the year, while silver's increase reached an astonishing nearly 139%.

This is the first time since 1980 that gold, silver, and copper have all set historical highs in the same calendar year.

1. Market Status: Historic Breakthrough and Structural Changes

1. Market Status: Historic Breakthrough and Structural Changes

● The precious metals market is experiencing an unprecedented collective frenzy. As of December 22, the spot gold price reached a maximum of $4435.28 during the day, continuing to set historical records. Silver performed even more impressively, breaking through the $69 mark during the day and soaring to a historical high of $69.44.

● The structural changes in the market are also significant. The gold-silver ratio, which measures how many ounces of silver can be purchased with one ounce of gold, has narrowed sharply from a high of 105 in April this year to around 64. This ratio is approaching the lowest point in nearly five years, indicating that silver's performance has significantly outpaced that of gold.

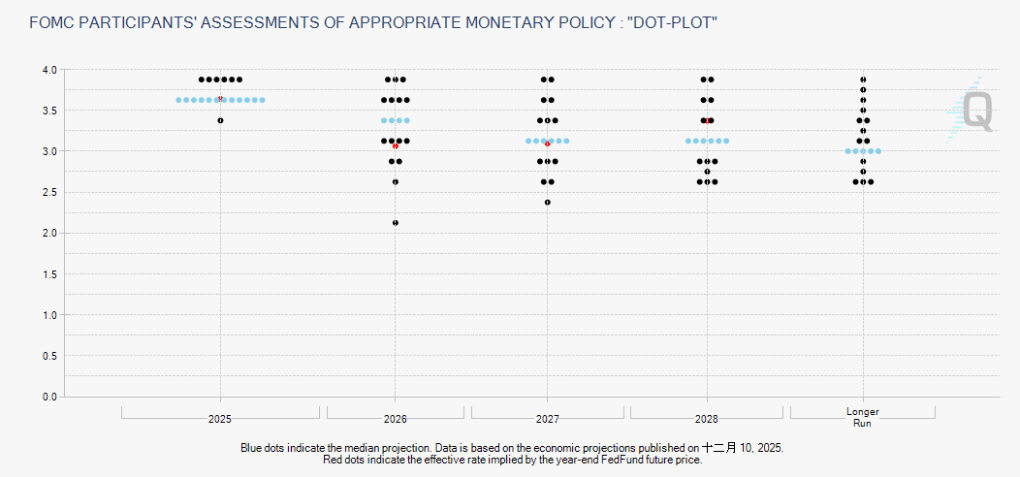

Second, driving forces for the rise: resonance of multiple factors 1. Macroeconomic policy and interest rate expectations

Second, driving forces for the rise: resonance of multiple factors 1. Macroeconomic policy and interest rate expectations

● Recent weak inflation and employment data in the United States have strengthened market expectations for the Federal Reserve to continue its accommodative monetary policy in 2026. Federal funds futures pricing shows that the market expects two rate cuts (a total of 50 basis points) next year. Gold, as a non-yielding asset, becomes significantly more attractive in a low-interest rate environment.

2. Weak dollar and risk aversion demand

● The U.S. dollar index has cumulatively fallen about 9% in 2025, marking the worst annual performance in eight years. Meanwhile, ongoing conflicts in the Middle East and uncertainties surrounding Russia-Ukraine negotiations continue to stimulate risk-averse buying in the market.

3. Central bank gold buying spree

3. Central bank gold buying spree

● Global central bank demand for gold has remained high for four consecutive years. According to the World Gold Council, the net gold purchases by global central banks have reached 634 tons in the first three quarters of 2025. The market expects net purchases for the entire year of 2025 to still reach 850 tons. This buying behavior has been described by Professor Li Huihui of EM Lyon Business School as not for 'reserve diversification,' but for 'survival.'

4. The unique industrial demand for silver

● Unlike gold, industrial demand is a unique driver for this round of silver price surge. By 2025, the proportion of silver used for industrial purposes has exceeded 60%. The photovoltaic industry (with a compound annual growth rate of 17%), the electric vehicle industry (13%), and the explosive expansion of global AI data centers together constitute the three pillars of silver demand growth.

● The supply elasticity of silver is quite limited; it takes about ten years from deciding to mine a new silver mine to the first output.

Three, historical trend review: similarities and differences

1. Comparison with historical highs

● Gold has set over 50 historical highs this year, with a cumulative annual increase of over 60%. This increase is second only to the record set during the second oil crisis in 1979 and the period of high inflation in the United States.

● Looking back at history, during the precious metals bull market in 1980, silver prices soared from about $11 to $50 in just two months, followed by a sharp correction. While the current rise in silver is vigorous, 'strictly speaking, it has not yet reached the level of a 'true parabola' like that of 1980.'

2. Changes in market structure

● The biggest difference from previous cycles is the 'spotization' of pricing power. The main buyers today are no longer hedge funds engaged in swing trading, but 'national teams' and 'physical hoarders.'

● After these buyers purchase gold, they often directly transport the gold bars back to their countries, no longer entering market circulation, leading to extreme exhaustion of liquid trading chips in the market.

Four, the impact on the macro economy

1. Reflecting changes in the global credit system

● Professor Li Huihui referred to gold as the 'thermometer of monetary credit.' The core driving force behind the recent rise comes from the 'collapse of sovereign trust' and the 'acceleration of de-dollarization.' Gold is upgrading from an investment 'asset' to a high-quality 'collateral' used by institutions.

2. Transmission to the real economy

● The high prices of gold and silver have begun to suppress some real demand. For example, jewelry demand in India dropped by 26% year-on-year in the first three quarters of 2025. However, on the other end, the rigid demand for silver from industries such as photovoltaics, new energy vehicles, and AI data centers has formed price support.

3. Financial market linkage effects

● In the Asian market, the non-ferrous metals sector leads the way in 2025 with a surge of over 70%. In the first three quarters, the 141 listed companies in the Shenwan non-ferrous metals sector achieved a total revenue of 2.82 trillion yuan, with a total net profit attributable to the parent company of 151.288 billion yuan, a year-on-year increase of 41.55%.

Five, institutional views and future outlook

1. Mainstream institutional forecasts

Regarding the future market, Wall Street institutions generally hold an optimistic attitude:

● Goldman Sachs predicts that by the end of 2026, gold prices may reach $4900 per ounce, while also indicating significant upside risks.

● HSBC has set a target price for gold at $5000.

● For silver, there are significant divergences in institutional forecasts, with the mainstream range concentrated between $60-70 per ounce, and an optimistic scenario seeing $80-100.

2. Risk warnings

Analysts have also pointed out potential risks:

● Technical indicators for silver have shown overbought conditions, and with low market liquidity at the end of the year, prices may experience severe fluctuations.

● If the Federal Reserve cuts rates fewer times than the market expects, the upward trajectory of gold may face resistance.

● The global aluminum market is expected to have an oversupply of 1.1 million tons in 2026, accounting for 1.5% of global primary aluminum demand.

The surge in the precious metals market in 2025 is the result of the resonance of multiple macro factors and industrial transformations. The current precious metals bull market is not just a traditional risk-averse or anti-inflation trend, but a product of the combined resonance of loose monetary cycles, high fiscal deficits, and the recovery of global manufacturing.

Wang Leyi, chairman of Zhaojin Group, admitted: 'The gold industry is undergoing a profound 'value return,' and a new cycle of 'value reassessment' has already begun. The fluctuation of gold prices in the historical high range will become a new normal.'

After reaching historical highs, the market will shift from a broad bullish trend to structural differentiation. For investors, understanding the deep logic driving the precious metals market—reconstruction of the global monetary credit system, resource demand from industrial revolutions, and changes in market microstructure—may be more important than simply guessing the peak. In this uncertain era, the shine of gold and silver is not just a market frenzy, but a reflection of profound changes in the global economy.

Join our community to discuss and become stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX benefits group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance benefits group: https://aicoin.com/link/chat?cid=ynr7d1P6Z