It's been a while since I wrote, today I’d like to share my different views on the global stablecoin landscape.

It's been a while since I wrote, today I’d like to share my different views on the global stablecoin landscape.

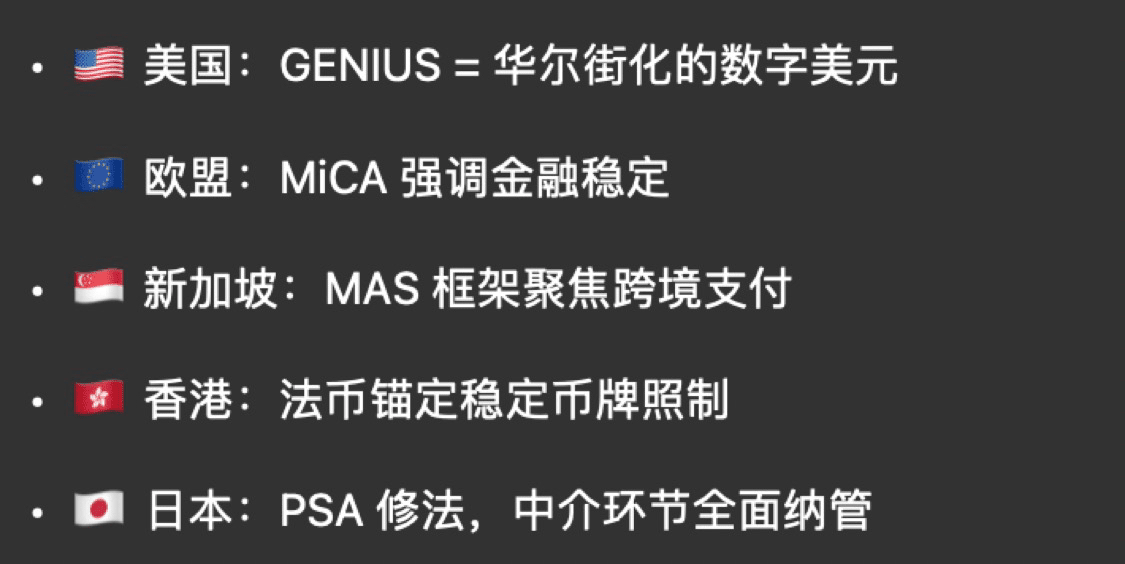

After 'Crypto Week' in July 2025, the U.S. positioning of stablecoins underwent a paradigm shift: from 'law enforcement regulatory targets' to 'digitalization vehicles for dollars constrained by federal legislative frameworks.' The House successively passed the (CLARITY Act) and the (Anti-CBDC Act), followed by the White House signing the (GENIUS Act) effective on July 18, establishing core rules for payment-type stablecoins: federal licensing, 1:1 qualified reserves, face value redemption, periodic disclosures, and 'issuers are not allowed to pay interest.' This is not a narrow 'regulation of crypto,' but the beginning of incorporating 'on-chain dollars' into national financial infrastructure and handing it over to Wall Street for industrialized operation.

I. On-Chain Migration of the Dollar System: A Complete Replication from Architecture to Functionality

Post-war dollar hegemony was built on three things: SWIFT/CHIPS cross-border clearing, a deep pool of U.S. Treasury bonds, and OFAC sanctions and compliance networks. Stablecoins have moved this framework on-chain: 24/7 second-level settlements replace batch processing for cross-border transactions; reserves anchor cash and short-term debt, directly mapping global 'dollar demand' to demand for U.S. Treasuries; and publicly verifiable on-chain data and the embedment of KYC/sanction rules enhance the visibility and enforceability of regulation over fund flows rather than weaken it. On-chain data also corroborates usage structures: stablecoins have become the dominant asset type in multi-regional trading activities, with long-term proportions fluctuating between 60% and 80%.

II. Legislative and Industrial Division of Labor: Handing over the 'On-Chain Dollar Minting Rights' to Regulated Wall Street

(GENIUS Act) writes 'who can issue, how to issue, and how to regulate' into federal law: the licensing path covers banks and compliant non-bank issuers, enforcing 1:1 qualified reserves and face value redemption, periodic audits and disclosures, and issuers are not allowed to pay interest directly to holders. After the regulation took effect, a key point of contention emerged: banks lobbied to tighten the space for 'platform rewards/indirect interest payments,' citing concerns about deposits being siphoned off by on-chain dollars; this just proves the policy power of 'stablecoins = on-chain deposit substitutes.'

III. Global Penetration: The Vanguard Battle for Digital Dollars Has Begun

In Latin America and Africa, high inflation and foreign exchange shortages have brought stablecoins to the streets. From the second half of 2023 to the first half of 2024, the proportion of stablecoins in on-chain funds in Latin America has significantly risen; the use of USDT in the African market has continued to increase since 2024, serving both payment and value preservation purposes, with P2P and local payment applications replacing 'dollar cash' with 'dollar tokens.'

In Asia, cross-border e-commerce and freelancers are bypassing SWIFT, directly using on-chain dollars for payments and settlements. The daily USDT settlement amount on the TRON network in the summer of 2025 exceeded the $20 billion to $24 billion range, with low fees and broad coverage, effectively forming a 'new emerging market dollar clearing layer.'

Europe is the first to incorporate stablecoins into unified law (the complete licensing, reserve, and disclosure framework for MiCA regarding EMT/ART will take effect from June 2024), but from the perspective of on-chain usage structure, dollar-pegged stablecoins remain overwhelmingly dominant, and euro stablecoins still struggle to compete in terms of scale and network effects. Regulatory readiness does not equal naturally forming monetary network effects, especially when the 'dollar stablecoin - U.S. Treasuries - U.S. compliance system' has already closed the loop.

IV. Technical Route: Transitioning from 'Multi-Chain' to 'All Chains Thriving' Pathway

The supply side is accelerating restructuring. Tether announced a redemption timeline for low-usage legacy networks (Omni, Kusama, SLP, EOS, Algorand, etc. will no longer be redeemable starting from 2025-09-01), focusing on high-demand main chains and new Bitcoin layers; simultaneously announcing the integration of USD₮ into Bitcoin RGB, promoting 'native dollars' onto Bitcoin and the Lightning Network.

Circle is adopting a 'broad coverage native issuance' strategy. As of 2025-06-24, USDC has been natively issued on 23 chains (Ethereum, Solana, Base, Arbitrum, Stellar, Sui, ZKsync, XRP Ledger, etc.), with the strategy being 'where there is compliance and real payments, the dollars will be sent there.' This means that stablecoins will evolve from financial primitives on a few main chains to the universal dollar bloodline for various business chains.

V. Institutional Hedging: The U.S. 'Market-Dominated Digital Dollar' vs. 'Central Bank Directly Issued Digital Currency'

The combination of the House passing the (Anti-CBDC Act) and the White House implementing the (GENIUS Act) clarifies the digital currency route for the United States: opposing direct access of central banks to retail accounts, instead allowing the market and Wall Street to issue and operate 'on-chain dollars' under strong regulation. This avoids the privacy and power controversies of direct government connections to retail while leveraging the long-term advantages of the U.S. capital market and compliance system. In contrast, China centers around the digital yuan, piloting licensed stablecoins in Hong Kong, aiming to form a digital extension of the yuan, but officials also acknowledge that they are still at a disadvantage compared to the global network effects of dollar stablecoins.

VI. Macroeconomic Implications: The Re-Closure of the Dollar Cycle and the 'New Extension' of Treasury Demand

Viewing stablecoins as 'on-chain dollar demand deposits,' their reserves are primarily anchored to cash and T-bills. This has led to a new cycle: U.S. Treasuries → Stablecoin Reserves → Global Payments/Investments → Capital Flow Back to U.S. Treasuries. The larger this 'digital dollar cycle' grows, the more stable the marginal demand for U.S. Treasuries becomes; even U.S. banks are beginning to worry that 'indirect interest payments' through platform rewards may trigger deposit outflows, indirectly confirming the 'on-chain deposit substitute' nature of stablecoins and their policy influence.

Let's take a look at the data comparison

📍 Europe: MiCA vs Digital Dollar

The EU's MiCA has gone live, but the daily trading volume of euro stablecoins (such as EURC) is less than 1% of USDT's. The reality is that in European DeFi, OTC, and cross-border scenarios, everyone still prioritizes using dollar stablecoins.

This means that even with a regulatory framework, the digital competitiveness of the euro lags far behind that of the dollar.

VII. Risks and Uncertainties

First, interest and profit sharing: how the 'gray area' where issuers are prohibited from paying interest but platforms can provide rewards will be tightened through secondary legislation or regulatory interpretations directly determines the boundary between stablecoins and bank deposits. Second, competition in the clearing layer: the game between TRON/Ethereum/Bitcoin layers and emerging high-performance chains determines the cost curve of 'on-chain dollars.' Third, cross-jurisdiction consistency: four frameworks operating in parallel in the U.S. (GENIUS), EU (MiCA), Singapore (MAS), and Hong Kong (licensing system) require 'multi-jurisdictional matrices' for cross-border products and custody arrangements.

Understanding stablecoins as 'moving the clearing layer and currency extension of the dollar on-chain' is closer to reality than seeing it as 'making crypto compliant.' The implementation of legislation means that the U.S. has allocated the minting and operational rights of 'on-chain dollars' to Wall Street through institutional frameworks; multi-chain expansion and the native integration of Bitcoin signify that the dollar clearing network is upgrading towards 'global, real-time, programmable'; and the usage scenarios in Latin America, Africa, and Asia have already transformed it into a new international dollar infrastructure. Bitcoin is an asset, Ethereum is a network, and stablecoins are a strategy—this is the fundamental landscape of geopolitics in digital currency post-2025.