Have you ever wondered: Why do we work more productively, have more advanced machinery, yet real wages can't even buy a house like in our fathers' time?

The answer does not lie in effort; it lies in the "Rules of the game" that have completely changed since 1971.

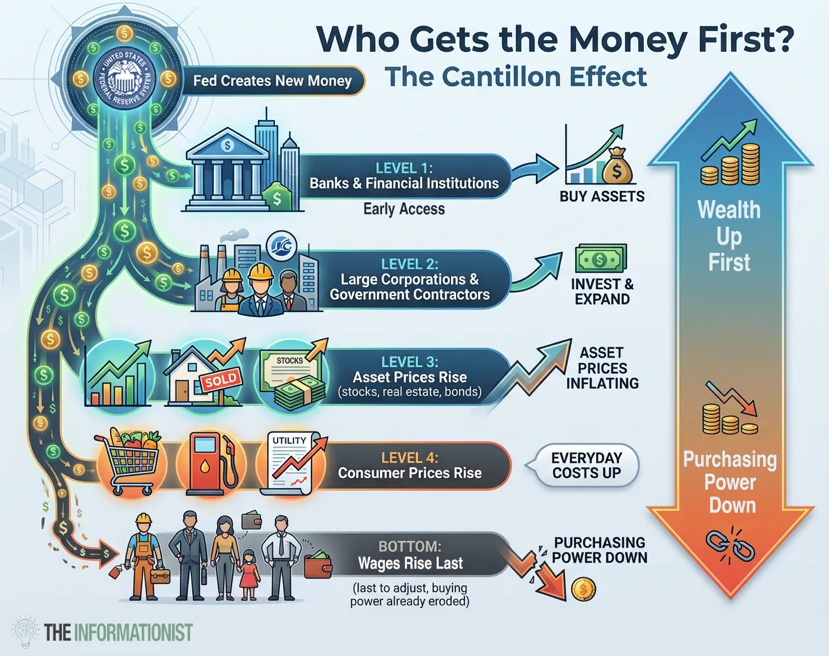

The answer is a phenomenon called the Cantillon Effect, named after an 18th-century Irish-French economist named Richard Cantillon.

And when that is realized, the way we view everything gradually changes. New money does not flow into the economy like rain soaking everyone at once when it rains on the roof. It flows in and out from specific points. Like a rainwater umbrella tipping over the roof of a high-rise building, it collects at certain points on top of the building, sometimes in penthouse apartments, then flows into drains leading directly to dedicated storage tanks, while the remaining water flows down both sides of the building and meanders along the streets.

It can be understood that when the dollar left the gold standard, money was printed endlessly. But it does not fall evenly for everyone at once.

• Group close to the money source (Banks, large corporations, financial institutions): Those who access money the most, spending new dollars before prices adjust. They buy assets, and then prices rise. The result is that their assets increase. ($BTC , gold, real estate) and push prices up.

• Group far from the money source (Salaried workers, savers, retirees with fixed incomes): Receive money last in the form of wages. By the time the money reaches them, prices have already increased. At this point, housing and food prices have skyrocketed. Their purchasing power has decreased. You are always the one left behind and have to pay a higher price.

The same new dollar. But the results are the opposite. (And while it is not the only factor, it is a very important one.) This helps explain why there has been a divergence between productivity and wages since 1971.

Workers continue to produce more. But the benefits from that productivity flow into the hands of asset owners more than laborers. The new money created by the Federal Reserve (Fed) is no longer constrained, leading to increased stock prices, real estate values, and bond portfolios. It makes the rich richer.

Meanwhile, real wages (after inflation adjustment) are stagnant. The average income of workers may increase on paper, but they cannot purchase more in life. Housing is more expensive. Healthcare is more expensive. Education has become more expensive. And ultimately, everything is increasing in price, including insurance and food.

Real labor productivity has increased, that is true. But people's wage increases lag far behind, nearly just an illusion.

📉 "The silent leak" in the savings account

Monitoring American politics reveals that the US federal government is currently carrying a debt of over $38 trillion. This figure is equivalent to about $114,000 for each American. Over 130% of GDP. Just the interest alone has exceeded $1 trillion per year, more than defense spending.

Every major economy in history that has faced this situation ultimately chose to devalue its currency. Not because they wanted to, but because it is the only door that is not closed.

The Federal Reserve (Fed) will assert its commitment to price stability. They will raise interest rates and publicly condemn inflation. And when the next crisis occurs (and it surely will), they will print thousands of billions more. They did it in 2008. They did it in 2020. And they will do it again.

This is not a conspiracy. This is an incentive structure. Those who make these decisions do not bear the consequences. They own assets. They are on the benefiting side of the Cantillon Effect. They will be fine, while you will not.

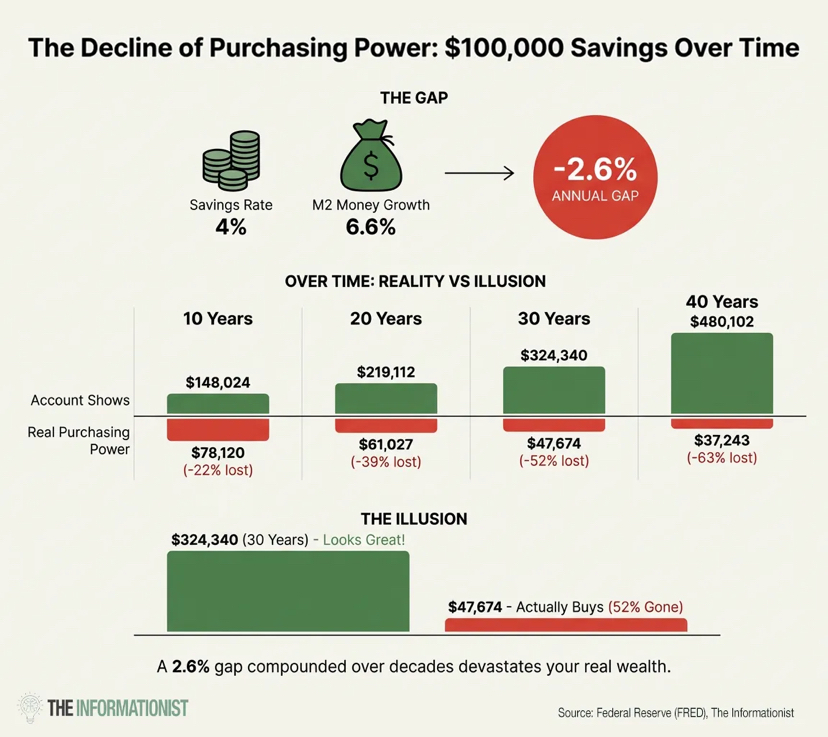

If you save at an interest rate of 4%, while the money supply (M2) increases by 6.6% per year. In reality, you are losing 2.6% of your asset value each year.

It does not disappear suddenly or appear on the statement. It is as silent as a water leak in the basement; you won’t realize it until your entire financial house is submerged. Each year, your salary buys fewer houses, less education, less healthcare, and fewer retirement savings. And that is not a coincidence. That is the system working exactly as designed.

💡Simple lesson from the wealthy:

The wealthy do not become rich by earning more money. They become wealthy by OWNING things that appreciate in value when the value of money decreases.

This is the obvious secret that everyone sees. The wealthy do not save in cash. They save in assets. Stocks, real estate, businesses, land, gold. Anything that can absorb new cash flow instead of being diluted by it. They are not smarter than you. They just understand the rules of the game.

When the Federal Reserve (Fed) prints more money, asset values increase. When asset values increase, owners become richer. When owners are richer compared to workers, the wealth gap widens.

Discussion:

If I consider that 'cash is trash,' I will continuously emphasize the importance of gold, Bitcoin, and preparing for what is to come.

Currently, the price of gold is at a record high of $4,500, and the price of silver has skyrocketed to an astonishing $80 an ounce. Central banks around the world are accumulating gold at an unprecedented rate over many decades.

The stock market could decline by 20% this year and drag down Bitcoin with it. Inflation could also surge back, and the Federal Reserve (Fed) could reverse its policy. Or we might have a soft landing, and everything will gradually increase.

I do not know for sure because short-term predictions are futile. But here is what I am certain of.

Debt will not disappear. The budget deficit will not decrease. The dynamics remain unchanged. Whether this year, next year, or five years from now, the trajectory remains the same: creating more money, greater depreciation of currency value, and an increasing transfer of wealth from savers to owners.

Therefore, I do not try to time the market. I choose the right position.

I own gold because it has been a store of value for 5,000 years, and central banks are buying it in droves.

I own Bitcoin because it is the first scarce digital asset in history, and over the long term, it has closely followed the expansion of the money supply almost perfectly.

I own real estate because assets absorb inflation and generate income in a context of a depreciating dollar.

I own stocks because businesses adjust their prices for goods and services when the currency weakens.

Will the value of these assets decrease? Certainly. Bitcoin could drop 40% tomorrow in a sell-off driven by risk-averse sentiment. Gold and silver could and very likely will be highly volatile. Real estate is illiquid. None of this is a straight line.

The goal is not to catch every move. The goal is to have the right position for the long game. Own things that benefit from value depreciation instead of being destroyed by it. Stop thinking like a saver and start thinking like an owner. And this is the discipline if you want to hold assets. The government's actions will increase asset values while wage increases are merely an illusion.

In my opinion, that is how this unfair system operates. No hope for fairness in the future, no fear.

If this article helps you see things differently, please share it with someone you care about. A friend, a family member, a colleague who feels frustrated for working harder but still being left behind. Sometimes, the most valuable thing you can give someone is insight. $BTC $XAU