In mid-February 2026, a once-in-a-decade winter storm swept across the East Coast of the United States, leading to widespread flight cancellations and forcing the Senate's schedule to be disrupted. As a result, the Senate Agriculture Committee postponed the hearing on the cryptocurrency market structure bill (the CLARITY Act) originally scheduled for Tuesday to Thursday, and a joint press conference by the heads of the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) was also delayed.

This meteorologically significant storm aptly metaphorizes the current political and financial turmoil on Capitol Hill in Washington.

Since the House passed the CLARITY Act (Digital Asset Market Structure Clear Act) in July 2025, the progress of this bill in the Senate has been arduous. On the surface, this is a dispute over the academic and legal definitions of whether 'digital assets are securities or commodities'; however, penetrating through hundreds of pages of bill text, its underlying logic is a zero-sum game between crypto newcomers represented by Coinbase and traditional Wall Street banking giants, revolving around the pricing power of funds, the underlying settlement network, and core business models.

Under the Trump administration, the crypto industry hoped for comprehensive deregulation, but the unexpected changes to the CLARITY Act in the Senate led industry leaders to choose to 'flip.' For professional financial practitioners and crypto investors, understanding the deeper logic behind this legislative deadlock is an essential lesson for asset allocation and risk avoidance in 2026.

Before the CLARITY Act was born, U.S. crypto regulation was in a chaotic state of 'litigation instead of regulation' for a long time. During the Biden administration, the SEC, leveraging a broad interpretation of the Howey test, initiated protracted lawsuits against several leading institutions, including Coinbase, Kraken, and Ripple. This unlimited extension of regulatory power not only created a huge 'regulatory risk premium' but also led to the outflow of North American crypto capital and technical talent to regions with clearer compliance frameworks such as Singapore and Europe.

The original intention of the CLARITY Act is to end this internal strife by delineating a clear boundary between the SEC and CFTC through a structured federal regulatory framework.

The bill establishes the standard of 'functional and decentralized.' If the underlying blockchain network corresponding to a crypto asset meets the decentralization standard (e.g., Bitcoin and some mature public chain tokens), that asset will be defined as a 'digital commodity,' with its spot market and secondary market trading platforms exclusively governed by the CFTC. Conversely, if the asset has obvious financing attributes, heavily relies on a core team for operation, and meets the characteristics of an investment contract, it will continue to fall under SEC jurisdiction, subject to strict primary market issuance, information disclosure, and investor protection rules.

The bill attempts to establish unified registration and conduct standards for exchanges, brokers, and dealers, mandating centralized exchanges to isolate customer funds and have them custodied by third parties, fundamentally preventing tragedies of misappropriation like FTX. At the same time, the bill seeks to integrate the stablecoin framework, excluding licensed payment stablecoins from traditional securities definitions.

This framework received widespread support from the crypto industry when it successfully passed through the House. The industry generally believes that the improvement in regulatory clarity will completely eliminate compliance uncertainties in the market and pave the way for the large-scale entry of traditional Wall Street funds. However, when the bill entered the Senate review stage, especially when the Senate Banking Committee and Agriculture Committee began revising the version in January 2026, the plot underwent a stunning reversal.

Last month (January 2026), the Senate version of the amendment began to surface, and the severity of its terms shocked the industry. As the largest compliant crypto trading platform in the U.S., Coinbase's CEO Brian Armstrong publicly withdrew support for the bill, stating, 'I would rather have no bill than a bad bill.'

The 'flip' by institutions like Coinbase is not due to a natural resistance to regulation itself but because the Senate amendment precisely targeted the core profit areas of crypto platforms and attempted to strangle the most imaginative business increments in the future. Specifically, the controversy focuses on three fatal clauses:

First, comprehensively block the interest-bearing model of stablecoins.

The amendment substantially restricts trading platforms and intermediaries from providing users with rewards related to stablecoins. Currently, Coinbase, in cooperation with Circle, invests users' USDC reserves in risk-free assets like U.S. Treasury bonds and allocates about 3.5% annualized returns to coin holders.

In 2024, Coinbase earned nearly $908 million from USDC-related business alone; by the third quarter of 2025, this business revenue had surpassed $350 million. This is Coinbase's most stable and highest certainty 'cash cow' beyond trading fees. Cutting off stablecoin yield distribution is akin to physically severing the growth engine of crypto platforms.

Second, strangulate RWA and the tokenization of U.S. stocks.

The Senate version explicitly excludes RWA from digital commodities and sets extremely complex registration thresholds for the tokenization of traditional financial assets (such as stocks and bonds) on public chains, effectively equivalent to a ban. This directly blocks the path for crypto platforms to penetrate the traditional financial asset trading field, breaking the vision for ordinary investors to purchase fractional shares on-chain.

Third, regulatory 'banking' of DeFi.

The bill requires almost all DeFi protocols to register according to standards similar to banks or traditional brokers, granting regulatory authorities extremely high access to decentralized trading data. This provision is not only difficult to implement technically but also fundamentally undermines the core values of DeFi related to anti-censorship and permissionlessness.

If we step out of the perspective of the crypto industry and examine the Senate amendment's various harsh terms from the macro-financial structure dimension, they actually reflect a concentrated embodiment of the will of traditional banking lobbying groups on Wall Street. The difficult birth of the CLARITY Act is essentially a battle to defend 'net interest margins.'

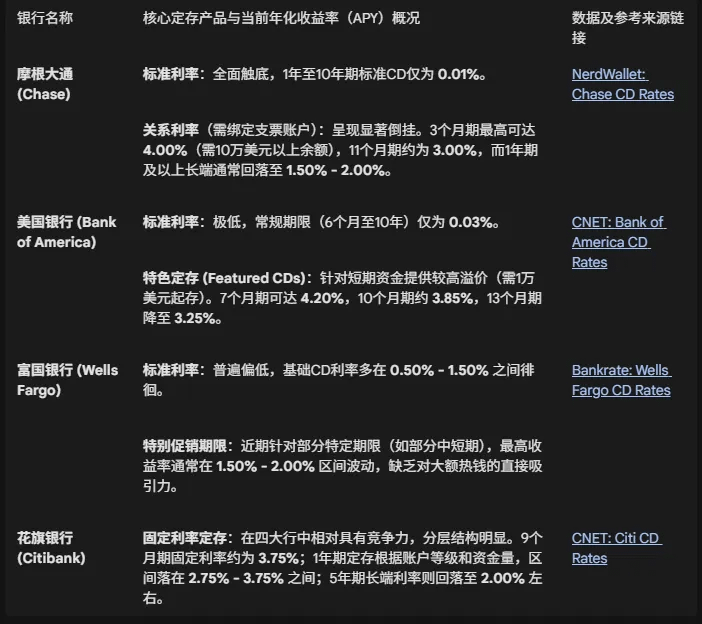

The profit cornerstone of traditional commercial banks lies in the interest spread between low-cost liabilities (public deposits) and high-yield assets (loans or bond allocations). Currently, ordinary depositors in the U.S. banking system can generally obtain interest rates on demand deposits ranging from 0.01% to 0.11%. In the crypto market, compliant stablecoins (like USDC) can easily provide users with 3% to 5% risk-free annual returns, relying on the interest generated from underlying government bonds and efficient on-chain settlement.

This dozens of times yield difference, combined with the stablecoin's dimensional reduction impact on the SWIFT system in cross-border payments in terms of efficiency and cost, causes stablecoins to evolve from merely being 'transaction mediums' in the crypto circle to becoming 'super savings accounts' with a powerful siphoning effect on the foundation of traditional bank deposits.

Banking interest groups are well aware that if the CLARITY Act passes in its original version, granting the interest-bearing model of stablecoins complete legality, hundreds of billions of dollars will permanently migrate from traditional bank accounts to on-chain every month.

Therefore, during the critical window for the merging and coordination of the bill, traditional financial capital exerted significant influence through political lobbying, attempting to use legislative means to force cryptocurrencies into the cage of 'high-risk speculative assets,' depriving them of their qualifications as interest-bearing assets and underlying infrastructure for payment and settlement.

Despite the current bill facing bipartisan disagreements and industry pushbacks between the Senate Agriculture Committee (focused on CFTC jurisdiction) and the Banking Committee (focused on SEC jurisdiction), the pressure from the White House and the political demands of the mid-term elections still make the likelihood of the bill passing in mid-2026 (early summer) extremely high. Once all parties reach a compromise on the final version and it is signed into effect by the President, we will see what profound impacts this will have on global capital markets.

First, the compliance gate for institutional funds will be thoroughly opened, and clear regulatory classifications will eliminate the last legal barriers for institutional entry. For assets categorized as 'digital commodities,' wash trading and market manipulation in the spot market will be severely cracked down on by the CFTC, and market volatility will gradually converge towards traditional commodities.

According to institutional analysis and forecasts, after the bill is enacted, banks will be allowed to conduct custody and trading services for digital commodities, and the net inflow of institutional funds into Bitcoin and Ethereum futures and spot markets is expected to surge by 300% in the short term.

Secondly, 'compliance risk premium' will shift towards 'value discovery.' In recent years, many Web3 projects with real fundamentals and strong cash flows (especially in DeFi and infrastructure tracks) have seen their token valuations long suppressed due to the constant threat of SEC unregistered securities charges.

If the bill can provide a clear exemption path for decentralized projects (i.e., as long as the core team does not control the network and there is no improper information asymmetry, it can be regarded as a commodity), these high-quality protocols will usher in systemic valuation recovery.

Finally, the ultimate integration of traditional finance and crypto assets. Although the Senate currently holds a conservative attitude towards RWA, in the long run, the establishment of a compliance framework will force traditional asset management giants to accelerate the issuance of tokenized funds on-chain. This integration does not mean that crypto disrupts Wall Street, but rather that Wall Street internalizes blockchain technology as its own infrastructure.

In this handover ceremony of new and old financial orders, ordinary investors and professional institutions face completely different risk exposures. In the face of the CLARITY Act, which is about to be finalized in 2026, market participants should strategically reallocate their assets.

The postponed hearing will eventually be held on Thursday, and the CLARITY Act will inevitably be born amidst the tug-of-war and compromise of multiple interests. This is not only a 'coming of age' ceremony for the crypto industry but also a key watershed in the historical evolution of human monetary forms and financial settlement networks.

Legislators and Wall Street are attempting to completely tame cryptocurrencies and incorporate them into the traditional system through the bill, while the native forces of crypto are striving to defend the spark of decentralization. For practitioners fighting in this market, shedding the illusion of 'absolute freedom' and deeply understanding the capital will and power dynamics behind the regulatory texts is the only rule for survival and achieving class leaps in the next decade.