On March 3, 2026, a thrilling 'roller coaster' market event unfolded in the global capital markets. Yesterday, due to the joint attack by the US and Israel on targets in Iran, along with a surge in geopolitical risk, safe-haven assets soared across the board. However, today, as the situation enters a 'news vacuum,' the market has shown significant divergence: #贵金属跳水 crude oil has demonstrated strong resilience amid supply concerns. This intense volatility of 'good news fully priced in, high-level distribution' is an excellent material for reviewing the war-driven asset pricing.

This article will systematically outline the background logic, historical patterns, derivative tracks of this event, and the long-term procurement dimensions of the government behind it. Friends who are interested, please give a thumbs up~

1. Background Review: Why does 'surge' immediately follow 'plunge'?

This round of market activity is a standard process of geopolitical risk premium transitioning from 'expected speculation' to 'rapid realization.'

Outbreak Period (March 2): After the attack occurred, traders immediately priced in the 'Hormuz Strait blockade' scenario. Spot gold once broke through $3,500 per ounce, and silver surged over 10%. This is a typical instant safe-haven demand.

Retracement Period (March 3): As Iran officially released signals of 'no further escalation,' the worst short-term scenario was disproven. Spot silver saw a deep drop of 8% today (falling back to around $48), and gold also retraced about 3% (dropping to the $3,200 range).

The independent trend of crude oil: Unlike the corrections of gold and silver, Brent crude oil today stood firm above $120 per barrel. The logic is: gold and silver trade on 'emotions,' while crude oil trades on the actual risks of 'physical supply disruptions' and soaring shipping premiums.

Core investment logic: The drive of war on commodities follows a three-act structure: 'warming expectations → price peak → favorable return.' Today's sharp decline in precious metals is not a fundamental reversal, but a typical risk premium 'mean reversion after a pulse.'

Two, Historical Backtesting: The 'Echo' of Precious Metals, Crude Oil, and Crypto During Wars

This round of volatility highly corroborates historical patterns: the 'war premium' of precious metals and crude oil is often released in a one-time concentrated manner, while cryptocurrencies reflect high β risk attributes.

1. The 2022 Russia-Ukraine War

In the first week of war, Brent crude oil soared from $90 to above $130 (+40%), while gold briefly spiked before entering a long-term downward channel lasting six months, ultimately accumulating only +8% for the year.

Silver resembles a 'pulled back after a pulse.' The pattern is clear: unless it evolves into a global all-out war, the wartime boost for precious metals is mostly 'one-time distributions,' and the most intense conflict nodes are the peak phases. Crude oil, however, maintains a high level for a longer time due to concerns over European energy supply disruptions.

2. The 2001 '9/11' and the Afghanistan War

Gold has transformed from a simple safe-haven tool into an 'anti-deficit/anti-inflation' tool. As the U.S. became entrenched in long-term wars leading to soaring fiscal deficits, gold prices embarked on a structural bull market lasting a decade.

The pattern is clear: long-term consumption wars will reshape the long-term pricing space of precious metals by undermining the credit of sovereign currencies (like the U.S. dollar), switching the logic from 'panic hedging' to 'credit hedging.'

3. The Gulf War of 1991

Initially, gold prices surged due to Iraq's invasion of Kuwait, but on January 17, 1991, the day of the official start of Operation Desert Storm, prices recorded a historic single-day crash due to the transparency of the war situation and the elimination of uncertainties.

The pattern is clear: the market fears the 'unknown' most. Once war enters the 'open card' stage and expectations are fully priced in, safe-haven funds will quickly withdraw, leading to a mean reversion of asset prices on the day of the outbreak.

4. The 1973 Yom Kippur War

Crude oil soared from $3 to $12 within a year, triggering global severe inflation (stagflation), while gold entered an epic long-term bull market driven by inflation.

The pattern is clear: when war affects core energy supply chains (such as embargoes or blockades), the price logic will switch from financial attributes to physical survival attributes, resulting in a structural re-evaluation far beyond emotional levels.

5. The real performance comparison of BTC in several key conflicts in recent years

In this round and past conflicts, BTC often drops first due to liquidity squeezes when the situation is most tense, and only later reflects its 'anti-censorship' properties during rebounds. Currently, BTC is still not the first choice of safe-haven tool; its volatility is more anchored to global liquidity expectations (Federal Reserve policy) rather than mere geopolitical risks, and essentially remains a high beta risk asset.

2022 Russia-Ukraine War: At the beginning of the war, BTC plummeted sharply (-10% level) along with the U.S. stock market, mainly because institutional investors viewed it as a high-risk asset for liquidity hedging. Subsequently, due to the demand for 'anti-censorship cross-border payments' from both sides of the conflict, a pulse rebound occurred.

2024 Iran-Israel First Conflict: During the weekend when the conflict broke out, while traditional markets were closed, BTC acted as an 'all-weather pressure gauge,' plummeting nearly 15% instantly, releasing global market panic in advance.

2026 This Middle Eastern Conflict: At the most tense moment, BTC fell first due to liquidity squeezes along with stock indexes, and only later reflected its 'decentralized asset' safe-haven properties during rebounds. The pattern is clear: BTC is not the first choice of safe-haven tool. In extreme panic phases, it more resembles a '24/7 liquidity gateway,' with its volatility more anchored to global financial market liquidity expectations rather than mere geopolitical risks.

Three, Investment Products under War Conditions: Which Ones Still Deserve Attention

Modern warfare has shifted from traditional ground conflicts to mixed warfare forms (proxy conflicts + cyber attacks + space confrontation + drone consumption wars), which has completely decoupled some investment products from the short-term pulse fluctuations of precious metals, instead binding them to 'government order rigidity + strategic security needs.' Even with today’s significant retracement of gold and silver, these products still possess strong resilience and medium to long-term allocation value, mainly because their core logic is no longer 'risk premium,' but rather 'the certainty expansion of national security budgets.'

The following are four major categories of investment products worth focusing on (mainly based on currently tradable entities):

Core Defense and Military Stocks

Directly benefiting from the accelerated increase in national defense budgets and emergency replenishment demands.

For example: Mitsubishi Heavy, Kawasaki Heavy; in the fiscal year 2026, Japan's defense budget reached a record high, and these companies have transformed from 'pure domestic demand' to core suppliers in the global defense supply chain; traditional giants like Lockheed Martin, RTX, and Northrop Grumman have seen significant visibility in missile and air defense system orders. Even with precious metals retreating, these military stocks remain relatively resistant to declines today, showing obvious alpha.Space and Low Earth Orbit Satellite Infrastructure Products

Modern warfare has become highly reliant on 'one-way transparency' and real-time communication, with low Earth constellations becoming a battlefield necessity.

For example: Planet Labs (Earth observation satellites), AST SpaceMobile (space mobile communications), and related publicly traded/ tradable entities of the Starlink concept. The Russia-Ukraine conflict and this Middle Eastern event have confirmed that the demand for low Earth satellite deployment is growing exponentially, and valuations have shifted to 'government strategic investment scale' anchoring, rather than traditional technology growth logic.Products related to Drones and Electronic Warfare Systems

The drone consumption war + electromagnetic power struggle is the core of the current conflict, with inventory depletion rates far exceeding those in peacetime.

For example: AeroVironment (drone systems), Anduril Industries (emerging defense technology, if already listed or indirectly allocated through related ETFs), gallium nitride (GaN) semiconductor-related companies. These products directly correspond to the real-time supply needs of the battlefield, with the highest order certainty.Strategic Minerals and Key Materials ETFs/Individual Stocks

Government strategic reserves and accelerated procurement under the Defense Production Act belong to the 'long-term material' category.

For example: ETFs or upstream mining companies related to rare earths, tungsten, antimony, and high-performance carbon fiber (such as key mineral localization theme stocks). These products have dual attributes under mixed warfare conditions: they are both defense raw materials and beneficiaries of supply chain security restructuring.

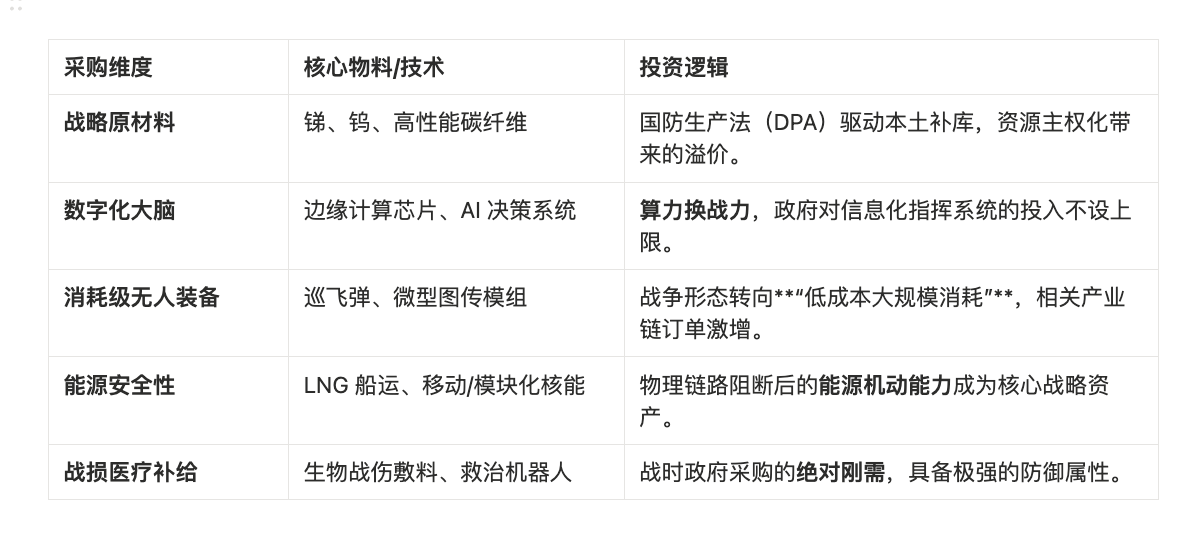

Four, Future Trends: Government Procurement Logic and 'Long-term Material' Reserves

Future wars have clearly shifted from 'explosive shocks' to 'sustained consumptive + mixed warfare' forms (proxy conflicts, cyber attacks, space domain confrontation, high-intensity drone consumption wars).

Against this backdrop, governments around the world will systematically accelerate the restructuring of strategic supply chains, the expansion of defense industrial capacity, and long-term material reserves, which will become the main line of long-term investment from 2026 to 2030, rather than solely relying on geopolitical pulse premiums. The following are core government procurement dimensions and corresponding asset logic:

////////

Finally, anchoring 'certainty' in uncertainty

The 'gold plunge, oil high' on March 3, 2026, again sounded the alarm for the market.

Historical backtesting tells us that war premiums are often short-lived and cruel, and the greed of 'earning the last penny' can often vanish in the trampling of mean reversion. However, after the smoke clears, the sovereign credit logic, resource allocation paths, and the redefinition of security boundaries by governments that have been completely rewritten by war are the truly long-lasting and robust investment lines.

For professional investors, rather than fighting in the rapidly changing safe-haven sentiments, it is better to focus on those strategic pivots that possess essential attributes in the 'post-globalization fragmented era'—whether it is the supply chains deepening critical minerals or dominating satellite links.

In this turbulent era, the most scarce asset is not gold, but the ability to see through the emotional fog and grasp structural transformations. The smoke will eventually clear, and the reconstruction of the global value chain has only just begun.

This article is based on publicly available information and is for reference only and not investment advice. Investing in crypto assets involves high risks; please evaluate yourself and consult a professional advisor.