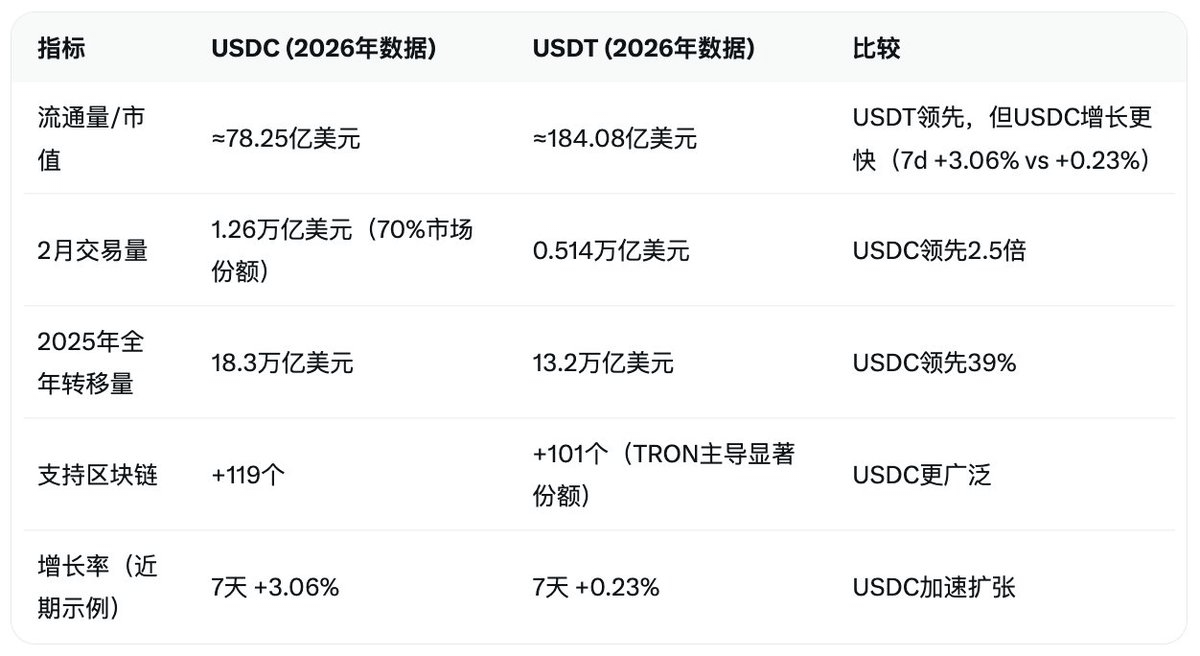

While social media is still flooded with discussions about OpenClaw, #USDC is quietly making its comeback. Looking back, the trading volume of USDC has surpassed USDT for several consecutive months, reaching a record high of 1.26 trillion dollars in February 2026, accounting for about 70% of the total trading volume of stablecoins that month; the stablecoin sector also set a new high of 1.8 trillion dollars in February, marking a historical peak in on-chain dollar liquidity.

This article discusses the far-reaching impact of this 'quiet comeback' on the liquidity and payment landscape of the entire cryptocurrency market by outlining the core data of the stablecoin sector, the structural advantages of USDC in compliance and transparency, and the deep adoption by institutions and the DeFi ecosystem. Remember to like and support it~

From USDT hegemony to a duel of two giants

Stablecoins, as the 'anchor assets' of the crypto ecosystem, have the core function of maintaining a 1:1 exchange rate with the US dollar, providing liquidity and avoiding volatility. Since its launch in 2014, USDT has rapidly expanded due to its first-mover advantage, and by 2024, its circulation had exceeded $110 billion, with market share once reaching over 90%. However, USDT's growth has been accompanied by controversy: its reserve transparency has been insufficient, having been accused of inadequate reserves during the 2019 New York Attorney General investigation, leading to a crisis of trust.

In contrast, USDC was launched in 2018 by #Circle and Coinbase, emphasizing regulatory compliance and transparency from the start. Early USDC circulation was only a fraction of USDT's, but through monthly reserve audits and full cash/Treasury backups, it gradually won favor among institutions.

By the end of 2025, USDC achieved an annual transaction volume of $18.3 trillion, surpassing USDT's $13.2 trillion, with a gap of 39%.

Entering 2026, this trend accelerates: USDC's circulation rises to about $7.8 billion, with reserves corresponding, and the annual growth rate significantly outpacing USDT; although USDT's circulation remains high at about $18.4 billion, it has shown slight contraction since the beginning of the year, with a slowing growth rate. According to @DefiLlama's latest data (March 10, 2026), the total market cap of stablecoins reached $31.4281 billion, with USDT's market share at 58.57%, and USDC around 24.9% (calculated from market cap).

Data sources: Allium, Artemis Analytics, DeFiLlama. From these indicators, USDC's comeback is not merely a scale expansion, but an enhancement in usage efficiency: despite its circulation being only about 42% of USDT's, its trading volume has dominated the market, reflecting higher turnover rates and organic demand.

Quantitative evidence of a reversal in trading volume

By delving into on-chain data, we can see that the rise of USDC stems from an explosion of organic trading.

According to filtered data from Artemis Analytics (excluding MEV bots and internal transfers of exchanges), USDC's 'real' transfer volume significantly led in 2025, benefiting from its deep integration in DeFi and payment scenarios.

For instance, on the #Solana chain, USDC's total transaction volume reached $696 billion, far exceeding USDT's $76 billion. Visa data shows that USDC has accounted for nearly 50% of stablecoin trading volume, especially in the institutional payment sector. In January 2026, USDC processed $8.3 trillion in transfers, while USDT only managed $1.7 trillion, despite USDC having a smaller supply, highlighting its higher efficiency.

Another key metric is active wallets and transaction frequency: USDC's monthly active addresses grew to an all-time high in January 2026, with #Polygon and #Base chains processing 68% of USDC transactions.

In contrast, although USDT has strong liquidity on the TRON chain, the overall growth rate of trading volume has slowed, partly attributed to volatility in emerging markets and regulatory pressures. In terms of user types, data shows that USDC is more favored by institutions: according to relevant reports, USDC has a higher proportion in institutional flows, while USDT dominates retail (especially in emerging markets and retail trades). Institutions such as BlackRock, JPMorgan, and Visa prefer USDC for settlement and treasury operations, while USDT has deeper liquidity in retail trading pairs.

From a reserve perspective, USDC's transparency is at the core of its data advantage: Circle is audited monthly by Deloitte, with 100% reserves in cash and short-term Treasury bonds; USDT, on the other hand, is audited quarterly by BDO Italia, with reserves including commercial paper, etc., which have lower transparency. This difference was highlighted in the 2025 Silicon Valley Bank incident: USDC quickly re-pegged after a brief de-pegging, while USDT's historical controversies continued to affect its institutional adoption rate.

Why was USDC able to achieve a 'comeback'?

The turnaround of USDC can be attributed to three major factors:

1. Transparency and auditing mechanisms

USDC's monthly reserve report provides granular details (such as significant investments in the Circle Reserve Fund), far surpassing USDT's quarterly overview. This has attracted institutional investors like BlackRock and JPMorgan, the latter reporting USDC's leadership in on-chain activities.

2. Regulatory compliance advantages

USDC complies with EU MiCA regulations and the US GENIUS Act, regarded as a 'covered stablecoin' rather than a security; USDT is non-compliant in the EU and faces delisting risks.

Circle holds various licenses including the New York BitLicense, promoting its adoption in B2B payments, such as replacing SWIFT for cross-border settlements.

Specifically regarding licenses: in the US, USDC obtains compliance through the GENIUS Act pathway and state money transmission licenses; in Singapore, it complies with the MAS single currency stablecoin framework; in Hong Kong, under the HKMA stablecoin regulations, USDC issuer Circle is applying for a license (expected to be issued in batches starting in 2026).

In contrast, USDT faces more scrutiny in these regions: in the US, compliance is achieved through the newly launched USA₮ under the GENIUS Act, but the main USDT remains questioned; in Singapore and Hong Kong, specific licenses are required, and USDT's status under the HKMA framework in Hong Kong is unclear, facing potential delisting risks.

3. Ecological integration and institutional inflow

USDC natively supports 119+ chains, especially with low fees and high efficiency on Solana and Base, promoting DeFi TVL growth.

In Q1 2026, Circle's revenue reached $770 million, with EBITDA growth of 412%, thanks to the payment use of USDC. Additionally, the pro-crypto policies of the Trump administration (such as regulatory easing in 2025) further amplified USDC's compliance advantages. In the wave of AI agents, USDC's role as a stable settlement unit is also becoming increasingly prominent, for example, in the OpenClaw-related Hackathon and Moltbook experiments, USDC was used for economic coordination and payments between agents.

Market impact: What signals are released by the new high?

This reversal has profound implications for the crypto ecosystem. First, the total market cap of stablecoins reached $31.4281 billion, with USDT's share at 58.57%, and the rise of USDC enhances market diversity, reducing the risk of a single issuer.

Secondly, in DeFi, USDC dominates significant liquidity pool trading, pushing TVL from $150 billion in 2025 to higher levels. In the global payment space, USDC's real-time settlement is replacing traditional systems, such as emerging market hedging and B2B cross-border transfers.

However, it is noteworthy that the market cap of stablecoins reached a new high of $31.4 billion in March 2026, yet the price of Bitcoin has not yet broken the historical high (currently around $71,680, still far from the 2025 peak of $126,000).

This reflects an increase in market liquidity, but funds have not fully flowed into crypto assets.

Analysis shows that stablecoins are seen as 'dry powder', but since 2026, net inflows of stablecoins into exchanges have been negative (a decrease of $1.4 billion), indicating that funds may be stuck in stablecoins waiting for macro signals or shifting to DeFi, tokenized assets (totaling $23.35 billion, with a monthly increase of 22.9%), and payment applications, rather than directly boosting BTC prices.

This phenomenon may stem from uncertainties in Federal Reserve policy and global liquidity pressures, causing investors to be more cautious. It is also worth mentioning that the Bitcoin network recently mined the 2 millionth BTC, with only about 1 million remaining to be mined (expected to be completed by 2140).

From an investor's perspective, USDC's leading signal indicates a bull market: in February, $66.5 billion flowed into exchanges, suggesting enhanced liquidity. However, it should also be noted that USDT still maintains strong liquidity in retail and emerging markets, and will not fully cede its position in the short term.

//////////////

Finally, although USDC currently leads in trading volume and institutional adoption, centralized risks remain prominent: it is highly dependent on the banking system, and similar short-term de-pegging events triggered by the 2023 Silicon Valley Bank incident may recur. The current regulatory environment is favorable for compliant stablecoins, but if the Federal Reserve tightens policies further or introduces stricter legislation in the future, both reserve yields and issuance costs will be under pressure. Although USDT is large in scale, it continuously faces doubts about reserve transparency and enforcement risks. At the same time, decentralized stablecoins (like DAI) and other emerging players are accelerating the diversion of market share.

Looking ahead to 2027, the total market cap of stablecoins is likely to exceed $3 trillion. With compliance and ecological advantages, USDC is expected to continue to eat into USDT's share, becoming the preferred anchor asset for Web3 payments and institutional fund management. In the long run, the outcome for stablecoins is likely not a single winner, but a gradual integration with various countries' CBDCs, forming a public-private mixed global digital dollar network. In the current frenzy of AI Agents like OpenClaw, USDC's 'low-key comeback' is actually sending a clearer signal: crypto finance has shifted from wild growth to compliance-driven, and this transformation will profoundly reshape the global currency and payment landscape.

Disclaimer: This article is for informational reference only and does not constitute any investment advice. The crypto market is highly volatile, and investments carry risks. Please do your own research and assume responsibility for the consequences.