Both stock market and cryptocurrency players are worried that AI will repeat the 2000 internet bubble, but in fact, Web3 is the true repetition of the internet bubble.

┈➤Bubble: Supply-side self-indulgence, demand is lackluster

During the internet bubble phase in 2000, funds were self-indulging on the supply side, with many internet listed companies having no profits or cash flow at all, yet stock prices skyrocketed.

On the other hand, there are very few internet applications on the demand side... Before 2000, there was no Douyin or Kuaishou, no Alibaba or JD, and no WeChat.

At that time, the mainstream internet applications were only the prototype of QQ, OICQ, chat software like MSN, download tools like Internet Express and Net Ant, information platforms like Yahoo, NetEase, and Sohu, basic applications like Google search and email, and early-stage e-commerce like Amazon and eBay, which had very few users.

At that time, there was no mobile internet, personal computers were considered luxury items, and the vast majority of families in the country did not have computers; monitors were those big-headed types. Laptops were as thick as bricks, and going online required dialing in with a phone line. Even older were storage media, where the main storage was floppy disks, yes, the A drive. The capacity was only 1.44M, which couldn't even hold a slightly larger image today.

It is worth mentioning that there were single-player games back then, but they were pixelated games.

┈➤AI: Leading infrastructure stocks surge, products are growing

Looking at the AI industry, although stock prices have surged, Nvidia, AMD, SK Hynix, Samsung, Micron... are mainly leading AI companies and are infrastructure types, because AI requires a lot of training before it can be put to use. On the supply side, AI does not have the exaggerated bubble like in 2000. At least these leading AI companies do have considerable profits.

On the demand side, we can at least see various UGC applications like Gemini, Claude, GPT, and Doubao... Also, the recently popular lobster, just launched Perplexity Personal Computer... the eye-catching AI robots from the Spring Festival Gala... Although the breadth of AI products cannot yet compare to those of the 2000 internet, this is because the development of AI requires high infrastructure standards; AI needs to develop infrastructure first before integrating more types of applications.

┈➤Web3: Technology as a gimmick, applications are few and far between

╰┈✦Circulating market value and profitability

Now, looking at the Web3 industry, various technical narratives are emerging, but how many applications truly have users? Besides a handful of leading Defi, perhaps only the MEME platform, prediction markets, and Perp dex, with much of the activity in the latter two still coming from interactions driven by airdrop expectations.

Corresponding to the scarcity of products on the demand side is the self-indulgence on the supply side.

⏵Example of ZK track: Daily income of $458 for ZKsyn with a circulating market value of $176 million, equivalent to a PE ratio of 1052.

⏵Example of L2 track: Daily income of $2,427 for Optimism with a circulating market value of $253 million, equivalent to a PE ratio of 285.

⏵Example of L1 track: Daily income of $3,564 for Sei with a circulating market value of $424 million, equivalent to a PE ratio of 327.

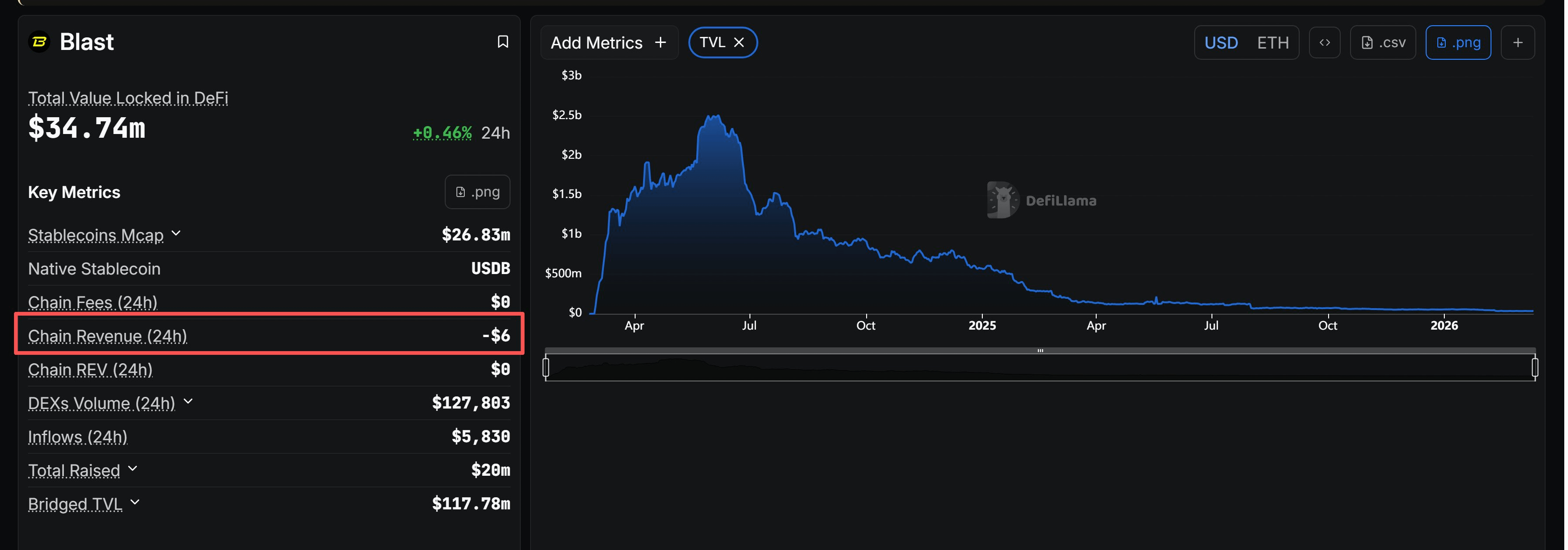

And the daily income of -$6 for Blast...

If we follow the logic of the stock market, the shareholders of the first three projects would have to wait 1052 years, 285 years, and 327 years to break even, not accounting for the infrastructure and operational costs needed to maintain these chains.

Although these ecosystems are not profitable and recouping costs through on-chain earnings, for shareholders, i.e., token holders, this is a nightmare...

╰┈✦What Web3 applications are there?

Let's look at what applications Web3 has?

Once-popular applications like the metaverse, chain games, inscriptions, and social... maybe some others we can't recall are now hardly mentioned.

Currently, besides defi and RWA, there are almost only meme, prediction markets, and perp DEX left. Among them, meme is a PvP for existing funds, while part of the interaction in prediction markets and Perp DEX still comes from the expectations of airdrops.

Compared to the internet applications mentioned in 2000, Web3 applications are truly scarce...

┈┈➤Written at the end

Therefore, the real issue lies not with AI on the supply side, but with Web3 lacking achievements on the demand side.

US stock players overlap with 26 years ago; investors and Wall Street are deliberately avoiding a repeat of history. AI has a bubble, but it is different from the internet bubble of 2000.

On the contrary, in the youthful field of Web3, capital is speculating on technology on the supply side, while there are not many truly practical products on the demand side, which is exactly the reappearance of the internet bubble of 2000.

Based on the moderate bubble in AI and the high bubble in Web3, reasoning:

First, the US stock market will correct, but the likelihood of a crash like in 2000 is low.

Second, BTC, which is related to the US stock market, is moderately affected.

Third, just like the internet bubble of 2000, altcoins will continue to be washed out, forming a painful process of distinguishing the genuine from the false, which may take longer than I imagined.

Currently, altcoins have fallen by about 15 months since the end of 2024, but this is not the end.

Do not believe the claims that altcoins have hit rock bottom; some altcoins have, while others have not.