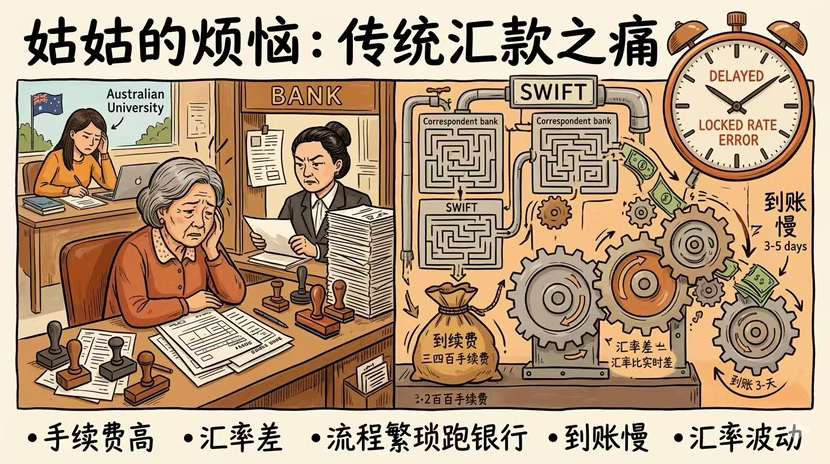

Last week, my aunt suddenly contacted me on WeChat.

Her niece is studying in Australia and is about to pay the tuition for the next semester. She asked me to help her check which bank has lower fees and faster transfer times for sending Australian dollars from China. I asked her which bank she usually uses, and she said she has always used ICBC, but every time the fees plus communication fees add up to three or four hundred, and the exchange rate is worse than the real-time rate. The most annoying thing is that she has to go to the bank every time to fill out the form, and if she makes a mistake, she has to start over.

The most frustrating thing is that when filling out the form there was one exchange rate, but when the money arrived a few days later, it was another exchange rate. The difference was enough to buy a cup of milk tea. I asked her if she had heard of MoneyGram? She said she knew, it's like Western Union, she had used it once before and felt it was similar. I told her that she might not know, but MoneyGram has recently joined a project called @MidnightNetwork . I sent her the link to the article I wrote and added a few more explanations.

Aunt's worry is actually a long-standing issue in cross-border payments. Traditional remittances go through the SWIFT system; a sum of money starts from a domestic bank, possibly passing through three or four intermediary banks, each taking two days to process, and then deducting a fee. By the time it arrives, the amount is less, and it has taken three or four days. Moreover, the entire process is opaque; you can only wait, not knowing where the money is or why it was deducted. MoneyGram, as a professional remittance agency, is a bit faster than traditional banks, but it cannot avoid the intermediary links. It needs to cooperate with local agents in various countries, each having its own systems and processes. Speed and cost have improved, but there is no fundamental change.

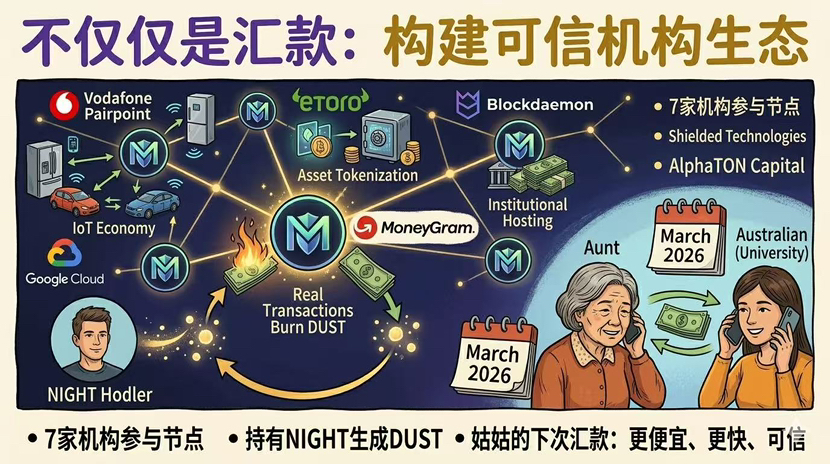

This is why MoneyGram joined as a Midnight node operator. MoneyGram operates in over 200 countries, with nearly 400,000 agent locations. If it wants to improve efficiency using blockchain, it could easily use stablecoins on existing public chains—fast, cheap, and with good liquidity. But it chose Midnight and even runs nodes personally. Why?

Chief Product Officer Luke Tuttle's exact words were: 'Ensuring privacy, compliance, and reliability from day one.' Note this word—'ensuring.' Not 'exploring,' but 'ensuring.' The biggest pain point in traditional remittance is: it needs to protect customer privacy while meeting the compliance requirements of various countries. If you use a transparent chain, customer information is fully exposed; if you use an absolutely anonymous chain, regulators won't recognize it.

@MidnightNetwork 's 'rational privacy' design fits right in the middle. It implements selective disclosure through zero-knowledge proofs—transactions themselves are confidential, but when an audit is needed, a gap can be opened to prove that the money is legitimate. What does this mean for MoneyGram? It means it can move its remittance business onto the chain, making the customer experience 'just a tap on the phone, a few minutes to arrive,' while still proving to regulators that every transaction is compliant.

Vodafone's Pairpoint has also joined, and it focuses on the 'Internet of Things economy'—allowing devices to trade autonomously. For example, your car pays for parking by itself, and your refrigerator orders milk on its own. These transactions require privacy protection, so the world can't see where you parked or what you bought. The zero-knowledge architecture of @MidnightNetwork is precisely what provides devices with credible identities. eToro has also joined, stating that 'all assets will eventually go on-chain,' but the prerequisite for going on-chain is the ability to protect business secrets and customer privacy. Blockdaemon has also joined; it serves over 400 institutions, managing $110 billion in assets. Its participation in Midnight running nodes signals to institutional clients: this chain is usable, not a makeshift operation. Along with previously announced Google Cloud, Shielded Technologies, and AlphaTON Capital, a total of seven institutions.

After Aunt finished listening, she asked a very direct question: 'So can it be used now? I need to remit next month.' I told her that the mainnet is set to launch at the end of March, so she might miss this time. But if MoneyGram really starts testing, it could indeed be possible in the future. Traditional SWIFT remittances take an average of 3-5 days, costing about 6% to 8%; whereas blockchain can theoretically achieve arrival in a few minutes, with costs reduced to 1% to 2%. By then, when the money arrives at your niece's side, the notification will come, and there will be no need to check the balance every day.

From the data perspective, $NIGHT price is around 0.047, with 57,079 holding addresses. Technically, 0.045-0.047 is the support zone. However, these short-term matters are not useful to Aunt. She cares about whether future remittances can be cheaper and faster. I said theoretically it can. If using the Midnight chain, with fewer intermediaries, the fees should decrease; 7x24 hours real-time arrival, no need to wait for banking business days; exchange rates can also be locked, without worrying about fluctuations. Unlike now, the price when filling out the form and the price when arriving are often two different things. After listening, she said, 'Alright, I'll keep an eye on it. I'll ask you before the next remittance.'

Aunt asked again, 'So can it be used or not?' I said it can't be used now, but the direction is right. MoneyGram chose @MidnightNetwork not because it wants to speculate on coins, but because it wants to use this chain for work. Working means: hundreds of thousands of real remittances daily, each requiring DUST to be burned, and DUST can only be generated by holding NIGHT. This is the true logic behind institutional participation. Aunt said, 'Then let me know when it can be used.' I said okay.

While hanging up the phone, I glanced at $NIGHT again, still at 0.047. But I thought maybe next time Aunt remits, she really won't need to go to the bank. #night