Just as the entire market eagerly awaits this week's Federal Reserve interest rate meeting, a ghost that no one wants to face once again hovers over Jackson Hole — the flames of war in the Middle East have once again pushed global central banks to the edge of stagflation.

For the fifth consecutive year, whenever Federal Reserve officials are convinced that inflation is about to return to the "gentle countryside" of 2%, reality always delivers a harsh slap in the face. From the aftershocks of the pandemic to the Russia-Ukraine conflict, from the comprehensive tariff plan of the year before last to the current turmoil in the Persian Gulf, the battle against inflation seems trapped in an endless cycle.

Today, tensions are high over the Strait of Hormuz, international oil prices have surged past the $100 per barrel mark, and gasoline prices in the United States have risen by 18%-25% since late February. The Federal Reserve is no longer faced with the easy question of "when to cut interest rates," as it did a few months ago, but a fundamental question that could rewrite the history of monetary policy: Is it even possible to cut interest rates this year?

I. From "When to Lower Prices" to "Can Prices Be Lowered": A Life-or-Death Battle of Expectation Management

I. From "When to Lower Prices" to "Can Prices Be Lowered": A Life-or-Death Battle of Expectation Management

● Timiraos points out that the core issue for officials at this week's meeting has fundamentally changed. The question now is not when the next interest rate cut will occur, but whether these policymakers, who control the global cost of capital, can still confidently instill expectations of interest rate cuts in the market.

● This battle will almost certainly reinforce the consensus among officials to "keep interest rates unchanged." But more difficult than holding back is what signals they should send in the coming months. The market is like a crying baby; if fed the wrong milk, it could trigger a violent vomiting of global risk assets.

● If you think this is just another tired "boy who cried wolf," you're sorely mistaken. This time, the script is compounded by four factors: high oil prices, high inflation, cracks in the labor market, and a change in the Federal Reserve chairmanship.

II. Three key indicators that could trigger a market meltdown tonight.

Based on guidance from "megaphones" and data from global forecasting platforms, tonight's interest rate meeting is far from a mere formality; it features three bombshell-level developments, each potentially triggering a new round of global asset pricing rebalancing:

● Signal 1: Should the word "interest rate cut" be deleted from the policy statement or not?

At the January meeting, a few hawkish officials attempted to remove wording from the statement that hinted at an "next step would be an interest rate cut," but failed. Timiraos analyzed that if this meeting ultimately makes this change, it will be the first time that officials have explicitly acknowledged that "the easing cycle may have ended." This is not merely a word game; it is an "obituary" for a shift in monetary policy.

● Signal 2: The "blood-red face" of the dot matrix image.

This is the most brutal and direct point of interest. Last December, 12 out of 19 officials predicted at least one interest rate cut this year. But now, circumstances are against them; if just three of them change their minds, the much-anticipated median expectation of an interest rate cut will drop to zero.

The market has already voted with its feet. According to options pricing calculated by the Atlanta Fed, traders believed by the end of last week that the probability of at least one rate cut by December had plummeted to 47%, compared to a high of 74% before the outbreak of the Iran-Iraq conflict last month. Even more alarming, the probability of a rate hike before the end of the year surged from 8% to 35% during the same period.

● Signal Three: Powell's "Last Dance".

This may be Powell's most conflicted press conference as his term nears its end. His term as chairman ends this May, meaning any policies formulated this week will become the foundation his successor must inherit. Will he take a hard line against inflation at the press conference, leaving a "hawkish" legacy for his successor? Or will he be vague, passing the buck to his successor? Every word he utters will be scrutinized by the market.

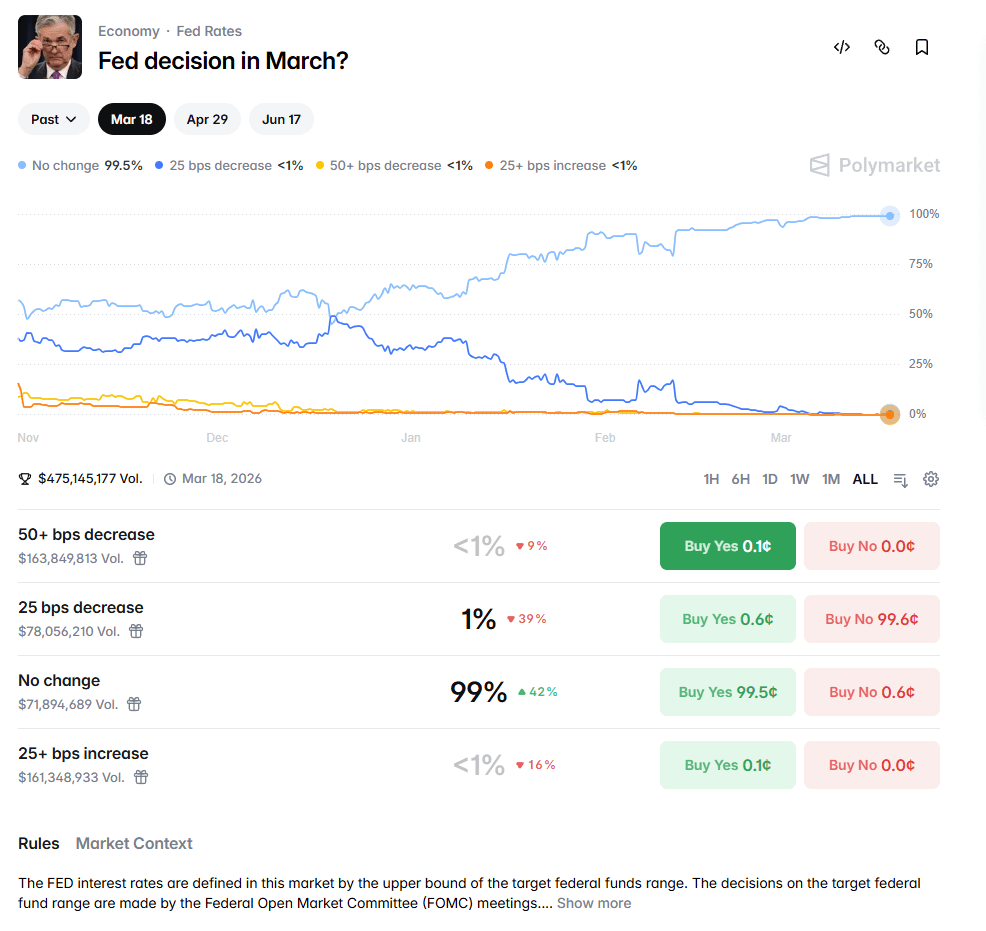

III. Polymarket's "Prediction": Traders Bet Real Money on "No Interest Rate Cut"

● On the decentralized prediction platform Polymarket, the trading of contracts related to this Federal Reserve decision has already become fiercely competitive. As an "alternative data source" outside of traditional financial markets, Polymarket's pricing often sensitively captures the true thoughts of smart money.

● Data shows that as of March 18, traders were betting that the Federal Reserve would maintain interest rates unchanged at this meeting by as much as 99%, while the probability of a 25 basis point rate cut was only about 1%, and the probability of a rate hike was almost negligible.

● Even more interesting are the full-year forecasts. A Polymarket contract regarding "the number of Fed rate cuts in 2026" shows that the probability of no rate cuts this year has risen to 23%, while the probability of at least three rate cuts has fallen from its pre-conflict peak to just 12%. This data starkly reveals a harsh reality: global traders are rapidly pricing in expectations of "higher interest rates in the long term."

IV. The Nightmare Cycle of Inflation: Is This Time Really Different?

● In the face of the oil shock, traditional central bank textbooks would tell you to "take a long-term view," because the impact of rising oil prices on economic growth and the push up inflation would roughly offset each other. But times have changed, and this advice now rests on the premise that the public believes inflation will eventually come down.

● The reality is that after five consecutive years of inflation exceeding the target, coupled with a series of shocks constantly reminding people of rising prices, this kind of "trust" has long become a luxury. Minneapolis Fed President Kashkari questioned in an interview this month: "Do we really want to have another 'temporary inflation 2.0'?"

● The core PCE price index, favored by the Federal Reserve, accelerated to 3.1% in January, after falling to 2.6% in April last year. Inflation is not only not dead, but is also being revived by geopolitical conflicts.

● Former St. Louis Fed President James Bullard was even more direct: if it were the end of last year, he would have included a rate cut in his plans, but now he would have crossed that off the table. With core inflation exceeding 3% and trending upward, "you certainly don't want to commit to a rate cut at this critical juncture."

V. Who can reopen the Strait of Hormuz?

Deloitte's head of economic research, Pradeep Philip, aptly pointed out: "Central banks can set interest rates, but they cannot reopen the Strait of Hormuz."

Tonight, regardless of Powell's wording or the fluctuations of the dot plot, one undeniable fact is on the table: the risk of stagflation in the global economy is being repriced due to the conflict in the Middle East. For investors, the narrative of "buying on dips" in interest rate cuts has failed; what awaits us may be a "purgatory mode" of struggling to survive between inflation and recession.

The only certainty is that history has never repeated itself so closely, and this time, the Federal Reserve is in a much worse position than ever before.