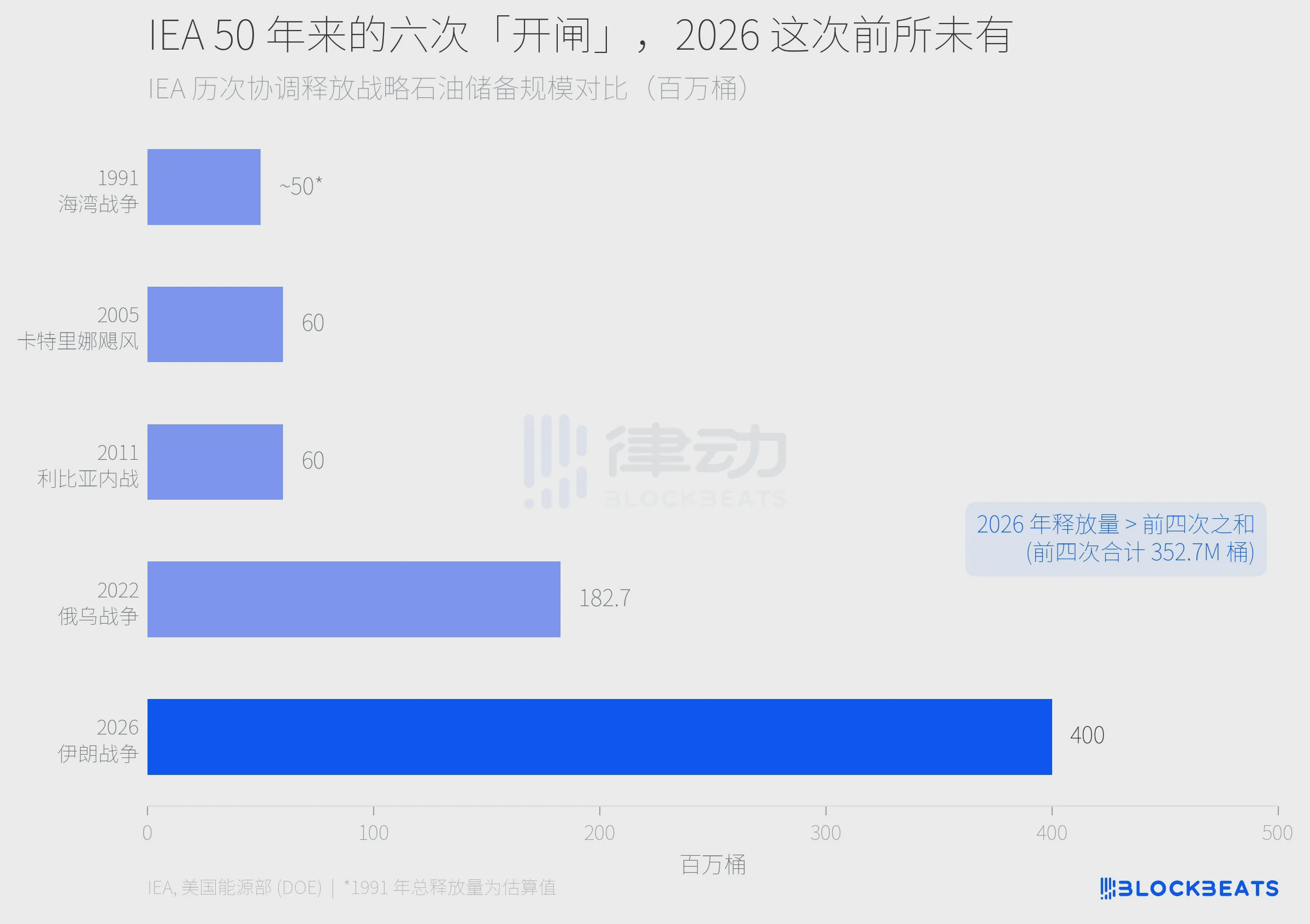

400 million barrels. This is the largest scale strategic oil reserve release by the 32 member countries of the International Energy Agency (IEA) in its 50-year history. On March 11, when the IEA announced this decision, Brent crude oil closed at $90.42 that day. Today, 12 days later, oil prices are above $107.

The story begins on February 28. After the United States and Israel launched a joint strike against Iran, Iran threatened to attack tankers passing through the Strait of Hormuz, nearly paralyzing the world's most important oil transportation chokepoint. According to IEA data, the current actual traffic in the Strait is less than 10% of pre-war levels. Brent crude oil skyrocketed from about $65 before the war, reaching $119.5 during intraday trading on March 9, an increase of nearly 80% in two weeks.

Against this backdrop, the IEA deployed its most powerful weapon. The question is, why did this weapon not work?

The mathematical illusion of 400 million barrels

400 million barrels sounds like a huge number, but when you look at it in the context of the gap in the Strait of Hormuz, the proportion is completely different.

In the 50-year history of the IEA, strategic reserves have been utilized a total of five times, with this being the sixth time. The total quantity released in the first four instances is about 352.7 million barrels (approximately 50 million barrels for the 1991 Gulf War, 60 million barrels for Hurricane Katrina in 2005, 60 million barrels for the Libyan Civil War in 2011, and 182.7 million barrels for the 2022 Russia-Ukraine war). This time, the 400 million barrels is even more than the sum of the first four releases.

But scale does not equal sufficiency.

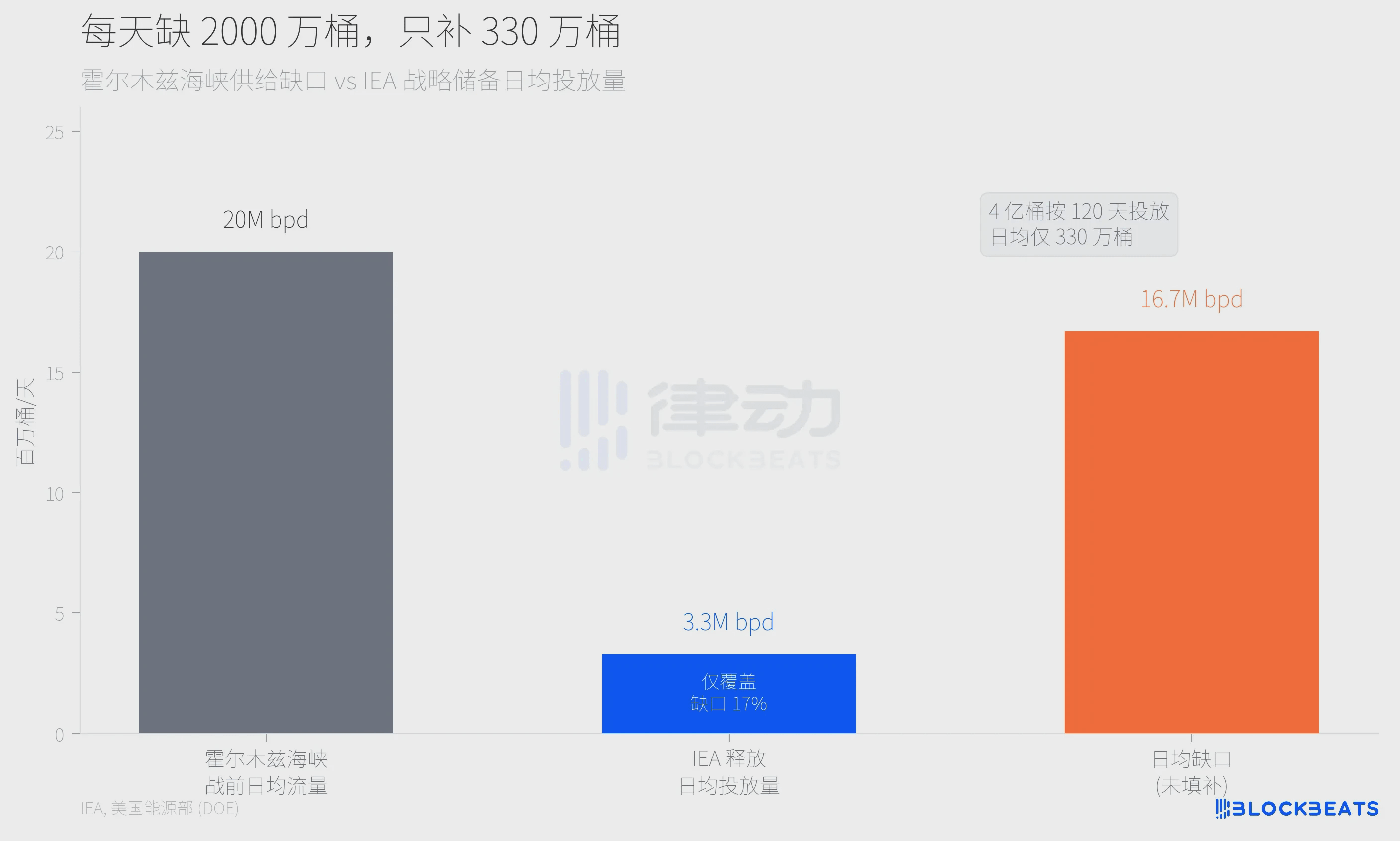

Before the conflict in the Strait of Hormuz, about 20 million barrels of crude oil and refined oil passed through daily, accounting for 25% of global maritime oil trade. According to the U.S. Department of Energy announcement, the 172 million barrels from the U.S. will be released within 120 days. Based on this pace, the IEA's total daily release of 400 million barrels is approximately 3.3 million barrels, covering only 17% of the gap. According to estimates from JPMorgan cited by Al Jazeera, the maximum production capacity of IEA member countries is only 1.2 million barrels per day, which is far from enough to make up the difference.

Using a more intuitive calculation: According to the IEA's March report, global daily oil consumption is approximately 103 million barrels. If all 400 million barrels were dumped into the market at once, it would only last less than 4 days.

Which historical instances of "opening the floodgates" really worked?

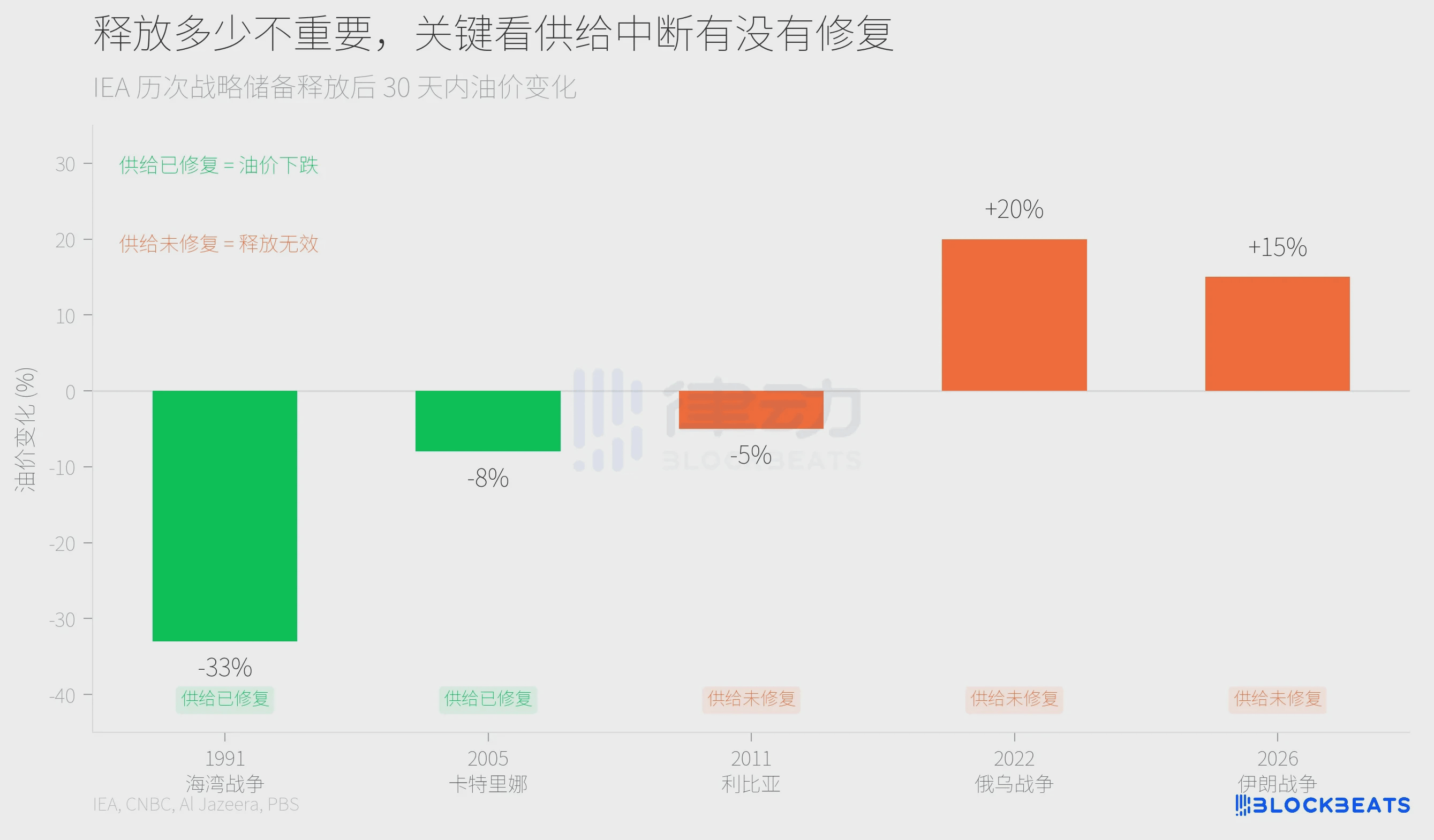

The results of the IEA releasing reserves five times in 50 years are clearly divided into two categories.

In the 1991 Gulf War, on the day the IEA announced the release, oil prices fell by about 20%, and the decline over the following week reached one-third. After Hurricane Katrina in 2005, the market also stabilized quickly. Both instances share a common feature: the source of the supply disruption was being repaired. The start of air strikes in the Gulf War meant that the Kuwaiti oil fields were expected to recover, and Hurricane Katrina had passed, with refineries gradually resuming operations.

The counterexample is the year 2022. After the outbreak of the Russia-Ukraine war, the IEA released 182.7 million barrels, but announced afterwards that Brent crude oil not only did not fall but rose, first surging to $113, and then slowly retreated over several months. The reason is simple: there is no prospect for a quick repair of the supply disruption from Russia.

The situation in 2026 looks more like 2022 rather than 1991. The Strait of Hormuz remains in a semi-blockade state, and Iran shows no signs of a ceasefire. According to an analysis by Stanford University researcher Maksim Sonin quoted by Al Jazeera, "This is not a panacea; the market is trading on expectations, and currently, expectations lean towards worry." Gregor Semieniuk, an economist at the University of Massachusetts Amherst, pointed out more directly, "The release can only buy temporary breathing room; once it's exhausted, the firepower is spent."

What determines the reaction of oil prices is not how many barrels are released, but whether the source of the supply disruption has been eliminated. The release of reserves is essentially not about "supplying oil," but about "buying time," using limited ammunition to negotiate and adjust alternative routes. If time is bought but the source of the disruption is unresolved, oil prices will still rise.

How much is left in the ammunition depot?

This raises a longer-term question: after repeatedly "buying time," is the ammunition depot still sufficient?

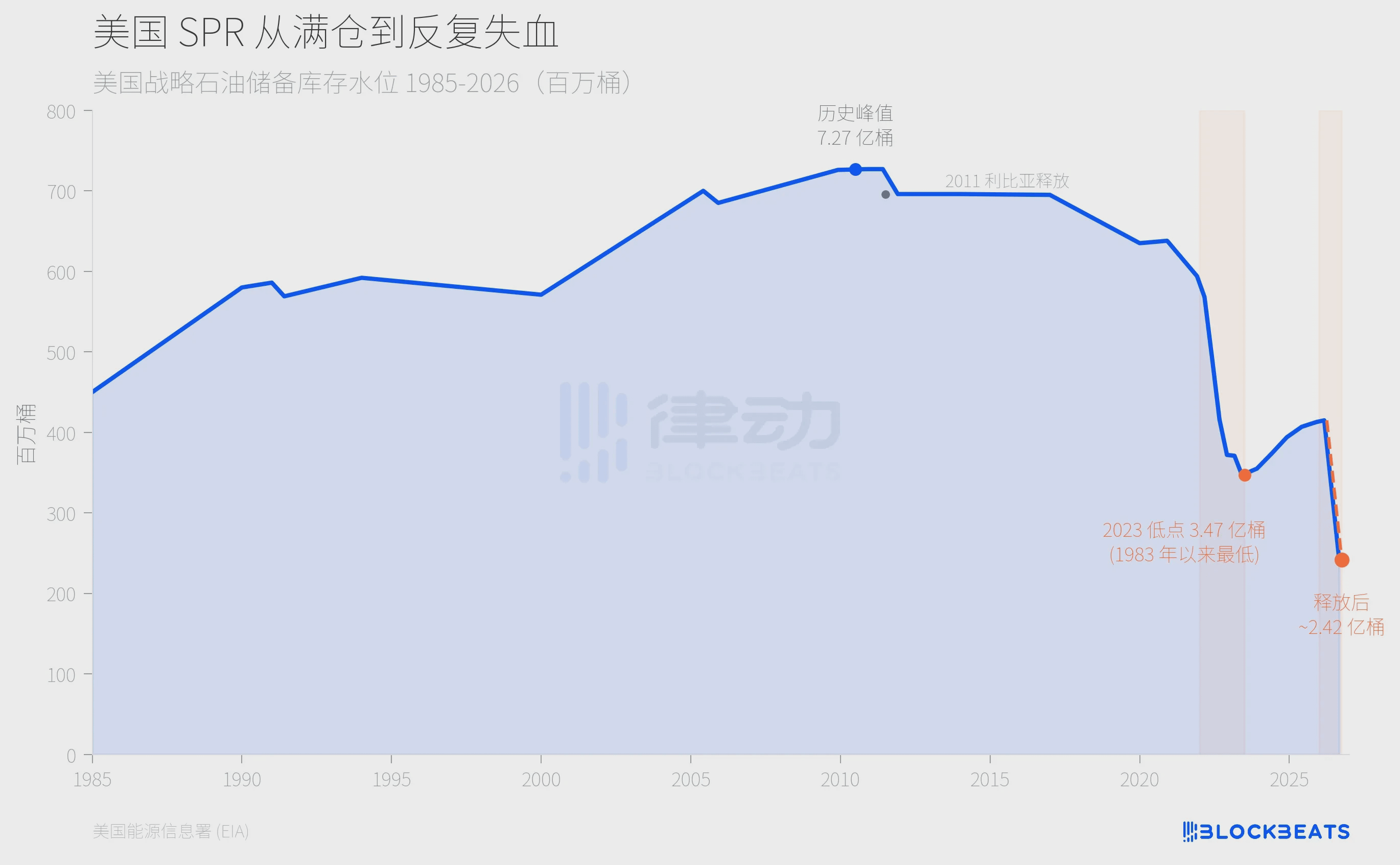

The U.S. Strategic Petroleum Reserve (SPR) is the largest government emergency oil stockpile in the world. According to data from the U.S. Energy Information Administration (EIA), the SPR peaked at 727 million barrels at the end of 2010. In 2022, the Biden administration released about 180 million barrels in response to soaring oil prices due to the Russia-Ukraine war, and the SPR fell to 347 million barrels in June 2023, the lowest level since 1983. After more than two years of replenishment, it is not expected to return to approximately 415 million barrels until March 2026.

Now, 172 million barrels of the 415 million barrels are to be released again. If the plan is carried out, the SPR will drop to about 242 million barrels, returning to the level of the mid-1980s when the stockpile was first established. The U.S. Department of Energy has promised to replenish about 200 million barrels within a year after the release, but the last replenishment took more than two years to climb from 347 million barrels to 415 million barrels, and the replenishment speed is clearly not keeping up with the rate of depletion.

Not just the U.S. The 32 member countries of the IEA held approximately 1.2 billion barrels of public emergency reserves before the release, and this time, the release of 400 million barrels directly cut one-third.

If the next supply crisis arrives before the SPR is replenished, will the global "last ammunition depot" be enough? There is currently no answer to this question. The market is unwilling to let oil prices drop precisely because it sees this problem.