A few weeks ago, Standard Chartered Bank released a report, downgrading the year-end price target for #ETH from $10,000 to $4,000, making headlines. The report指出, the L2 roadmap is the main catalyst for Ethereum's troubles and claims that L2 is 'taking away Ethereum's GDP.' The conclusion is that Ethereum's future value needs to be adjusted accordingly.

We will conduct our own analysis on this topic and share our findings with you.

But before that, we believe it is wise to analyze Ethereum's economic trends from scratch. This will lay the groundwork for future analysis and clarify the necessity of Ethereum's development and expansion of 'blobs' (i.e., Ethereum's data availability network).

The actual economic value of Ethereum (\u003ct-140/\u003e)

Defining Real Economic Activity (REV)

REV = value from user activity, directly attributable to Ethereum service providers and ETH holders. It does not include token incentives or fees paid to block builders (which we will introduce later in the report).

Four main components:

1. Base fee: This is the minimum amount of ETH that users must pay to process transactions on Ethereum L1. The base fee is dynamically adjusted based on network congestion to achieve a specific block utilization level (50%). In terms of value accumulation, the base fee is 'burned', meaning it is deducted from the circulating ETH. Within the offset of ETH issuance, 'burned ETH' can lead to a deflationary supply of ETH, providing value accumulation for ETH holders—similar to stock buybacks in traditional companies.

Base fees: Key Points

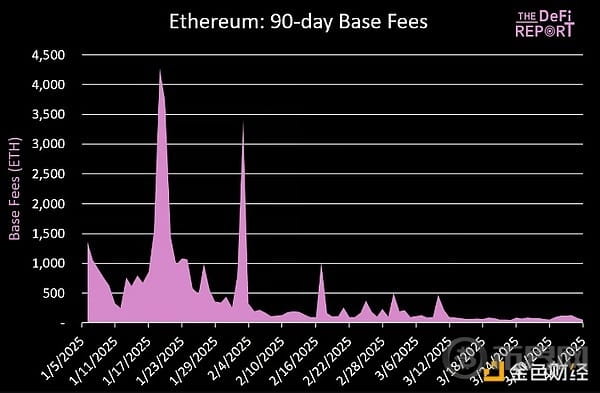

In the past 90 days, the base fees of Ethereum accounted for 50% of the total actual economic value generated by Ethereum validators.

A total of 48,007 ETH has been burned and removed from circulation (valued at $94 million at current ETH prices). Of this, 3.7% comes from L2, with Base leading. This offsets an issuance of 239,492 ETH during the same period (paid to validators as token incentives), resulting in an annualized inflation rate of 0.6% over the past 90 days.

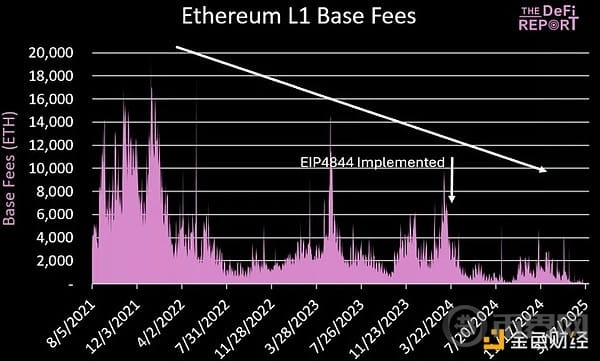

When we zoom in below, we can see the destruction of Ethereum's base fees over the past four years. In March, Ethereum's average base fee was only 102.7 ETH/day. For reference, this is less than 1% of the network's transaction volume in November 2021 (with a base fee of 11,809 ETH/day), and only 8% of the lowest base fee for Ethereum during the 2022 bear market.

The decline in base fees highlights the impact of EIP4844—a technical upgrade that allows for cheaper L2 transactions, implemented in March of last year. This is a key decision by the Ethereum Foundation to scale Ethereum through the 'L2 roadmap', which has led to Standard Chartered lowering its price target for ETH. We will delve into this more in future analyses.

2. Priority fees: Priority fees are paid by Ethereum users above the base fee to ensure time-sensitive (e.g., arbitrage, sandwich attacks, liquidations) transactions are moved from Ethereum's mempool to verified blocks. These fees belong to Ethereum validators (shared with passive stakers). In the past 90 days, Ethereum validators earned 25,169 ETH in priority fees (valued at $46.7 million at current prices). This accounts for 26% of validators' REV.

Priority fees: Key Points

While Ethereum's priority fees are at a four-year low, we can see that the extent of destruction is not as severe as that of the base fee decline. Why? Priority fees only apply to L1 transactions, while a large portion of Ethereum's base fees has shifted to L2 over the past year. In March, the network's priority fees averaged 218 ETH/day—down 88% from the peak in late 2021. Compared to the lows of the bear market in 2022, priority fees have currently decreased by 55%.

As more Ethereum execution activity shifts to L2 (such as Base), we should expect priority fees on Ethereum L1 to continue decreasing.

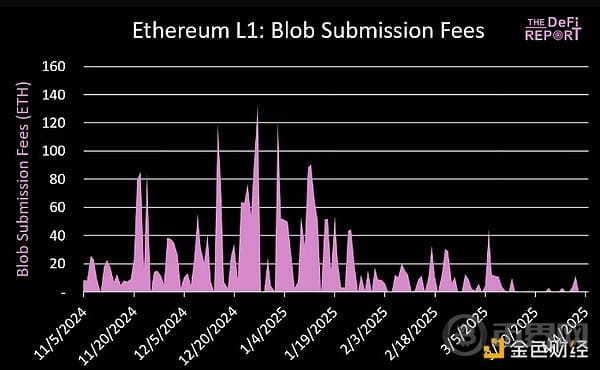

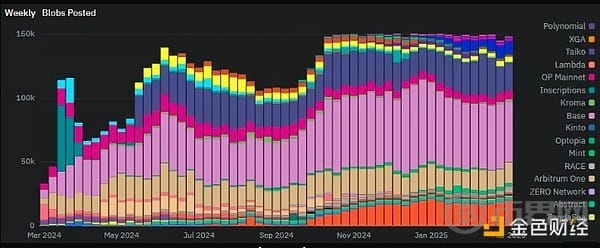

3. Blob fees: 'Blob fees' are the fees paid by L2 for data availability to Ethereum. These are new fees introduced by EIP4844. Similar to base fees, blob fees are 'burned' and removed from circulation.

Blob submission fees: Key Points

In the past 90 days, L2 in the ecosystem has paid Ethereum L1 1,605 ETH ($3.5 million) (which accounts for 2% of the total REV). Base made up 39% of these fees, followed by Taiko (18%), Worldchain (15%), Arbitrum (14%), and OP (4%). Overall, the top five L2s currently account for about 80% of blob submission fees.

Given that Ethereum intends to scale through L2, we believe it is reasonable to predict that the vast majority (over 95%) of transaction executions will occur on L2 in the future. Therefore, as L2 scales, blob submission fees (for data availability) should account for the vast majority of what Ethereum L1 validators pay.

If Ethereum were to replace its current REV solely through current DA fees, it would need 1.4 billion transactions per day from L2 (16,303 transactions per second). Currently, this is 92 times the total daily transaction volume for L2. That said, blob fee pricing is dynamic, so fees will increase non-linearly with demand (similar to L1 fees).

We conducted some analysis using the Blob simulator assembled by Tim Robinson. The results are somewhat concerning. Why? A mere 2.5 times increase in L2 transactions per second would lead to congestion on Ethereum L1. In this case, L2 fees would soar to $0.40. This is not a good thing. That said, protocol updates aimed at blob targets (Pectra, PeerDAS expected mid-2025) are on the horizon. If L2 scales 2.5 times, the target blob/block must be doubled (planned to be implemented on May 7 through the Pectra upgrade) to reduce the cost per transaction to $0.01. That said, we will see how future upgrades support further expansion at the L2 level.

Essentially, there are 3-4 L2s consistently meeting the target blob/block (3). This accounts for about 70% of the demand for blob space. Therefore, this means that other L2s need to compete for blob space, driving up fees. This is essentially the same scalability issue Ethereum faces at the L1 level.

We expect Ethereum to expand its blob size through protocol updates (such as PeerDAS, Fasaka upgrades, etc.) and aim for blob/block. But this is not an easy task. It takes time. And Ethereum doesn't have much time left.

How long will L2 endure scaling barriers before seeking alternatives?

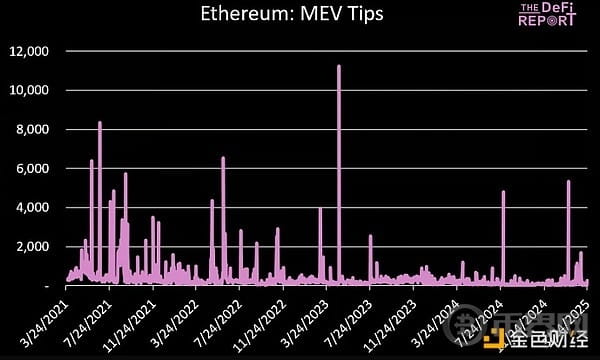

4. MEV: MEV is paid by users (bots) commonly referred to as 'seekers'. Essentially, you have trained bots that look for arbitrage opportunities, liquidations, and chances to 'sandwich' other users in Ethereum's 'Mempool' (where transactions pass before being packaged into blocks for validators). When they identify a transaction they want to execute (based on the mempool), they will submit it to 'block builders'—paying priority fees + an additional 'tip'. These fees (paid by users/bots) are collected by block builders, who then use these funds to bribe validators to verify blocks. Block builders retain about 30% (these are 'off-protocol' fees, which we will discuss later in the report), while validators take about 60% of the MEV (shared with stakers through MEV boost). Seeker bots retain about 10% of the MEV generated by the transactions they submit.

MEV: Key Points

In the past 90 days, Ethereum validators have received 21,159 ETH ($39 million) in MEV tips (accounting for 22% of total REV). Similarly, these fees are paid to block builders (who receive funding from bots/'seekers' needing to perform time-sensitive transactions).

We analyzed 'seeker' transaction activity over the past 30 days to determine which transactions drove the most MEV. Here are our findings:

Arbitrage transaction volume: $3.6 billion (seeker profit $1.9 million)

Sandwich transaction volume: $6.3 billion (seeker profit $135,000)

Liquidation transaction volume: $86.4 million (seeker profit $176,000)

Generally, seekers will retain around 10% of the value extracted from the MEV generated by their transactions. Builders will keep about 30%, while validators (and passive stakers) will receive about 60%.

At the end of 2021, when on-chain activity was most active, validators earned approximately 1,619 ETH daily from MEV. In the past 90 days, this number has dropped to 230 ETH per day (an 86% decrease).

From the chart, we can see that MEV rewards are inconsistent and can spike significantly during congested/time-sensitive transactions. The most profitable MEV day for validators occurred on May 3, 2023 (earning 11,228 ETH of MEV). This is related to the launch of the Pepe memecoin.

MEV applies only to transactions conducted at the L1 level. Therefore, as transaction activity shifts to L2, we should continue to see a decrease in MEV earned by Ethereum validators.

Token incentives

As noted in the introduction, actual economic value includes only the value paid to Ethereum validators through user transactions (shared with ETH stakers).

But this is not the only way validators are compensated.

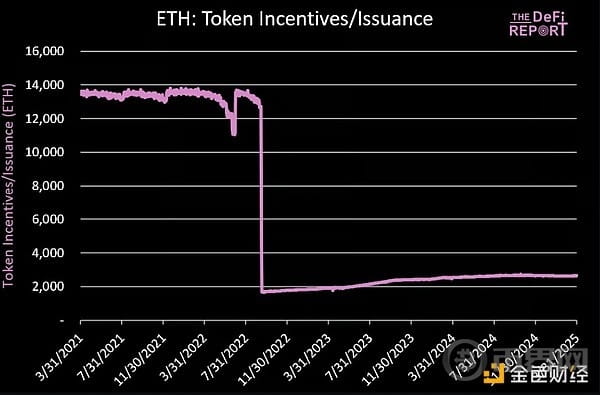

Finally, there are token incentives/network issuance. This is ETH paid to Ethereum validators as a consensus reward for securing the network.

We can see below that when Ethereum transitioned from proof of work to proof of stake through the merge, token incentives dropped by about 80%.

Token incentives are used to initially bootstrap the decentralized validator set of blockchain networks. However, over time, we should see them decline as user fees compensate for the security of the supply side.

This is what we have seen historically with Ethereum, but now we can observe that due to reduced user fees associated with EIP4844, token incentives are again on the rise.

Data: Token Terminal, DeFi Reports

Token incentives: Key Points

In the past 90 days, Ethereum has paid an average of 2,631 ETH ($4.7 million) in new issuance tokens to validators daily.

During the same period, Ethereum validators earned 515 ETH/day ($926,000) from MEV and priority fees.

This means that currently only 16% of Ethereum validators' income comes from user activity. The rest comes from token incentives/network issuance.

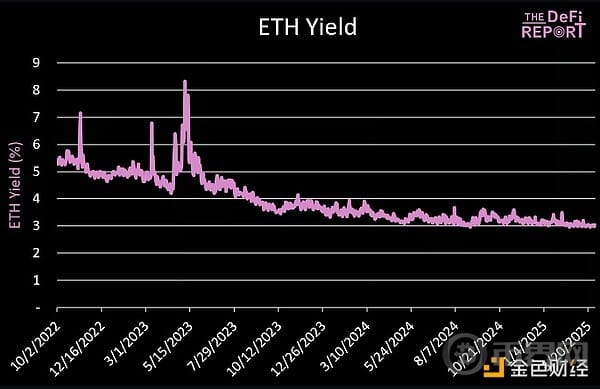

Validator yields

The four components of REV + Ethereum's token incentives constitute Ethereum's dynamic yield, which also fluctuates based on the amount of ETH staked on the network (currently 34.3 million ETH, making up 28% of the supply).

Finally, we can visually see below the relationship between validators' income, the new ETH issuance, and REV (priority fees and MEV). In the past 90 days, the network issued 239,000 ETH to validators, who also received 46,000 ETH from priority fees and MEV (which represents about 16% of the total value received).

Off-protocol revenue (block builders)

In addition to the value Ethereum validators (and passive stakers) derive from user transactions, Ethereum also has 'hidden' value from user transactions that is paid directly to block builders.

Workflow:

User submits transaction —> Ethereum mempool —> 'Seekers' (bots) identify value (arbitrage, sandwich trades, liquidations) —> submit additional transactions to block builders (with tips) —> block builders bundle transactions —> submit to validators (with tips) —> validators approve transactions, retaining most of the tips (block builders and seekers retain a portion).

The portion retained by block builders and seekers is considered 'off-protocol' revenue since it is not shared with validators and passive ETH stakers.

Block builders: Key Points

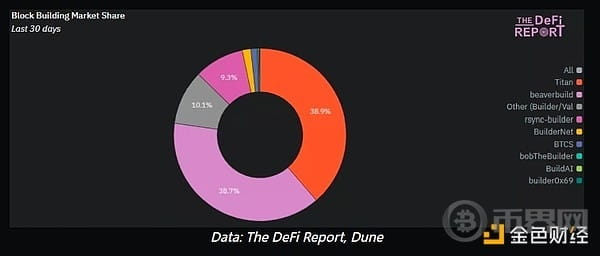

Currently, 90-95% of Ethereum blocks are built by 'block builders' using protocols like MEV-Boost. This outsources block building capabilities to validators (reducing complexity) while allowing them to earn MEV (shared with stakers).

In the past 90 days, block builders have earned 12,524 ETH. This accounts for about 30% of the total MEV during that period.

During the same period, about 20% of block builders' revenue was returned to users through 'rebates' (2,550 ETH). 'Rebates' occur when users allow their transactions to 'roll back'—meaning that 'seekers' submit transactions after the user transactions (without affecting the user transactions) but still generate more profit for the 'seekers' transactions. Users can use protocols like Cowswap to qualify their transactions for rebates, which leverage private RPCs to share some transaction details from the mempool.

In the past 30 days, three block builders have been responsible for building 87% of Ethereum's blocks. They are BeaverBuild, Titan Build, and Rsynch Builder.

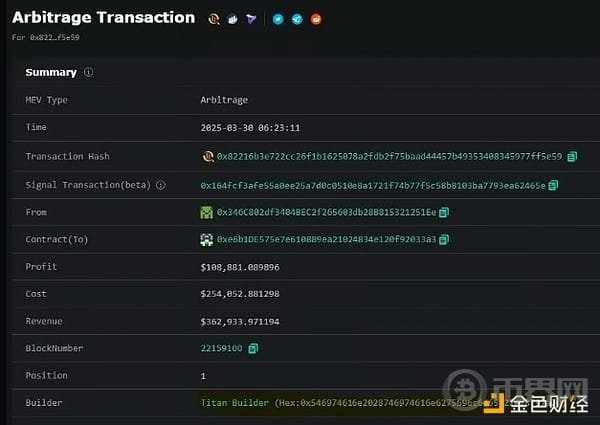

If you're curious, here’s an example of an Ethereum arbitrage trade, where 21 tokens were exchanged across 49 trading venues, ultimately making a profit of $108,881.

Seeker address: 0x346C802df3404BEC2f265603db28B815321251Ee

Contract address: 0xe6b1DE575e7e610889ea21024834e120f92033a3 (handling arbitrage + paying builder fees)

Builder: Titan Builder

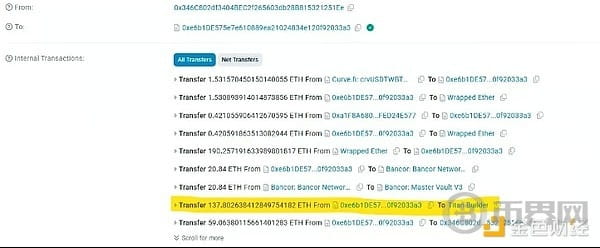

Below, we can see one of the payments made to Titan block builders from a contract address on Etherscan:

I hope this article can lay a solid foundation for our further analysis to assess the feasibility of the Ethereum roadmap and the value accumulation brought to ETH through 'blobs'.

This work has produced some key observations and questions:

Ethereum is disrupting itself through the L2 roadmap. It now needs to rebuild its economy in a more B2B model (L2 as clients) rather than a B2C model (individual users as clients).

As users continue to turn to L2 for better execution, Ethereum's base fees, priority fees, and MEV should continue to decrease.

These fees will need to be replaced by 'blob fees', which are data availability fees. We believe this will require large-scale, substantial L2s, technological upgrades for L2 scaling, and a moat for Ethereum's DA.

We believe that the vast majority of execution activity on Ethereum will shift to L2. This may not be realistic, as L1 may always retain a core group of users. How large this group is and which use cases will remain on L1 is still unclear today.

To make the roadmap work, we believe L2 needs to surge to website scale. Additionally, Ethereum needs to establish a moat in data availability. This may come in the form of 'block fees', but achieving this may take a long time.

Given that currently only three block builders are responsible for building about 85% of Ethereum blocks, we think concerns about centralization and censorship are valid.

As institutions seek to tokenize stocks in the coming years, will they allow MEV to leak to Ethereum validators? Will regulators permit 'sandwich' attacks to persist? For this reason, we believe institutions will seek to launch L2s where they can capture trading fees + MEV. This could be good for Ethereum, but it also requires scaling. The good news is that demand exists. For reference, all TradFi processes approximately 100-200 billion transactions daily across stock and derivatives markets, payments, and other financial instruments.

This cycle's Ethereum L1 fee losses flowed to L2, which is why Standard Chartered adjusted its Ethereum price target. Meanwhile, L2 is also being adopted.

What would this chart look like when every bank and fintech company has stablecoins and stocks are tokenized?

As Charlie Munger (RIP) liked to say, 'Show me the incentives, and I will show you the outcomes.' Given that TradFi firms will be able to control execution and MEV by building L2, we believe they may be incentivized to build on Ethereum rather than Solana. The key question is whether Ethereum can scale 'blob' quickly enough to serve them.

In summary, we believe that the future of Ethereum depends entirely on 'blob fees' (data availability) and its ability to generate network effects between L2s. Our future work in this area will focus on predicting the scalability of 'blobs' and the value accumulation of ETH through dynamic pricing mechanisms and scenario analyses.