After the ceasefire, the Strait of Hormuz has not opened, leading to severe supply disruptions, but oil prices have not fully rebounded, and even long-term contracts are still declining, which may indicate the most core and unsettling truth of the current market.

Futures down ≈ recession ≈ stock market crash: the only coherent logic in the current market, and also the most dangerous truth.

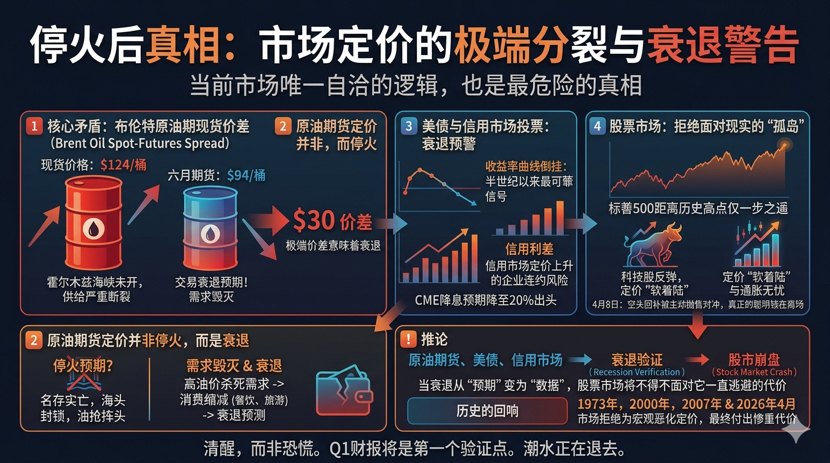

The current global financial market is exhibiting an extremely fragmented pricing structure: Brent crude oil spot prices have reached as high as $124 per barrel, while June futures contracts are only about $94, resulting in an extreme price difference of up to $30.

Meanwhile, the S&P 500 index is just one step away from its historical high, and the Nasdaq has basically recovered all losses since the outbreak of war.

The war is still ongoing, the Strait of Hormuz is still blocked, and the Bughaig oil field is still smoking, but the stock market seems to be oblivious to it all. This division has left countless investors confused.

But amidst this chaos, there exists a single coherent logic chain—and its conclusion may be more unsettling than you think.

1. What are crude oil futures pricing in?

On the surface, the continued decline in crude oil futures seems to be trading on 'ceasefire expectations'—the market believes that the war will soon end, the Strait will reopen, and supply will return to normal.

But this explanation does not hold up. On the first day the ceasefire agreement took effect, Israel launched its largest airstrike against Lebanon, and Iran immediately closed the Strait again, forcing tankers to turn back. The fatal loophole in the agreement regarding Lebanon rendered the so-called 'ceasefire' illusory from the very beginning.

A more reasonable explanation is: the crude oil futures market is not trading ‘ceasefire’, but trading ‘recession’. High oil prices are killing demand. Gasoline prices have surged from $3 per gallon before the war to $4.12, costing American consumers an additional $150 billion per year. This $150 billion would have been spent on dining, travel, entertainment, electronics, but is now entirely burned in gas tanks.

Meanwhile, the uncertainties of war have led companies to pause investments, postpone hiring, and accumulate cash. Consumers are delaying home purchases, car purchases, and large expenditures. There is no need for oil prices to rise further; just a sustained high oil price for long enough will naturally lead to a collapse in demand. And the collapse of demand itself is the definition of a recession. The continued decline in crude oil futures contracts is not saying 'supply will recover', but rather 'demand will be destroyed'. The futures spot spread of up to $30 is not saying 'no worries about inflation', but rather 'a recession is certain, and it will be severe'. Only a severe recession can shrink oil demand enough to cause oil prices to drop from $124 to $94.

2. The U.S. Treasury and credit markets have already voted.

Crude oil futures are not the only market pricing in a recession. The U.S. Treasury yield curve continues to be inverted—short-term yields are higher than long-term yields—which is the most reliable recession warning signal in the past half-century. Credit spreads are gradually widening, indicating that the market is pricing in increased corporate default risks.

The CME FedWatch Tool shows that market bets on interest rate cuts within the year have plummeted from 43% after the ceasefire news to just over 20%, and even began pricing in the probability of rate hikes.

The crude oil futures market has already voted.

The U.S. Treasury market has already voted.

The credit market is voting.

They all point to one judgment: high oil prices and war uncertainties are pushing the economy toward recession.

3. Stock Market: The Last 'Island' Refusing to Face Reality.

However, the stock market is telling a completely different story.

The S&P 500 index has basically recovered all the declines since the outbreak of war, only about 3% away from the historical high.

The VIX fear index has plummeted from over 30 at the beginning of the war to a six-week low of just above 20, with the market completely withdrawing from risk-averse positions.

Tech stocks—the sector most sensitive to interest rates and economic growth—have become the leaders in the rebound.

What is the stock market pricing in? It is pricing in a 'soft landing': oil prices will drop back, inflation will come down, the Federal Reserve will cut interest rates, and the AI revolution will continue to drive high growth in profits.

All these assumptions are diametrically opposed to the pricing of the crude oil futures market, the U.S. Treasury market, and the credit market.

But more fatal is the internal contradiction of the stock market itself: the epic short squeeze on April 8—an extreme short position of 7.6 to 1, the catalyst of ceasefire news, and the triple forces of market maker Gamma squeeze—only resulted in a 2.5% increase in the S&P 500, with net capital outflows throughout the day.

This means that the buying pressure from short covering has been completely offset by stronger active selling forces. Institutions are selling, retail traders are selling, and individual investors are selling.

The real 'smart money' has not chosen to increase positions, but has chosen to exit the market.

The drop in war-related stocks has been recovered, but not due to strong buying, rather because short sellers are bleeding. When the fuel for short covering runs out, the market will be completely exposed to a vacuum state without buying support.

4. A terrifying inference.

Putting all the clues together, a disturbing inference emerges: crude oil futures are trading in a recession, U.S. Treasuries are trading in a recession, and the credit market is trading in a recession—only the stock market is still refusing to face it.

If crude oil futures are correct, then the recession will shift from 'expectation' to 'data', and corporate profits will be forced to downgrade, with overvalued tech stocks facing a 'Davis double whammy' of earnings and valuation.

At that time, the stock market will be forced to pay the price it has been evading. This is not a prediction; it is the logical endpoint pointed to by multiple major markets.

You do not need to 'believe' that a recession will definitely come; you only need to observe one fact: almost all major markets, except the stock market, have already voted for a recession. The stock market cannot remain isolated forever.

5. Echoes of history.

History has repeatedly proven: when the market refuses to price in macro deterioration, the ultimate cost paid is always far heavier than what it tries to evade.

In the summer of 1973, inflation soared, the Federal Reserve raised interest rates, and oil prices were about to surge, but the S&P 500 fluctuated near historical highs, refusing to drop. It subsequently halved.

In early 2000, the profitability of internet companies was debunked, the Federal Reserve raised interest rates, but the Nasdaq refused to believe that 'the story would break' at historical highs. It then fell 78%.

In the summer of 2007, subprime defaults surged, and Bear Stearns funds went bust, but the S&P 500 refused to believe that the crisis would spread at historical highs. It subsequently halved.

In April 2026, the Strait was blocked, Bughaig was attacked, there was a supply gap of tens of millions of barrels, inflation was sticky, and the Federal Reserve had no hope of cutting rates—but the S&P 500, near historical highs, refused to price in any deterioration.

6. Be clear-headed, not panicked.

"Futures down equals recession equals stock market crash"—this logic chain sounds terrifying, but it is not alarmism; rather, it is the only coherent explanation for the current multi-market pricing contradictions.

See it clearly, not to panic, but to prepare.

The Q1 earnings season will be the first verification point. When corporate profit guidance first reflects the impact of high oil prices and war uncertainties, the recession will shift from 'expectation' in the futures market to 'numbers' in earnings reports. At that time, the stock market will have to confront the reality it has been trying to evade.

When the tide goes out, we will know who has been swimming naked. And the tide is going out.