Charlie Munger: After turning 40, you must do these three things!

——Investment Master—Charlie Munger.

If you are currently in your 40s, it might be a good idea to stop what you're doing and listen to me carefully. The decisions you make in the next 12 months will determine whether your life in your 60s is stable and smooth or chaotic.

[Streamlined Version]

[Detailed Version] If you hope for changes in your life, I suggest reading this in detail. You can like, save, and share it first.

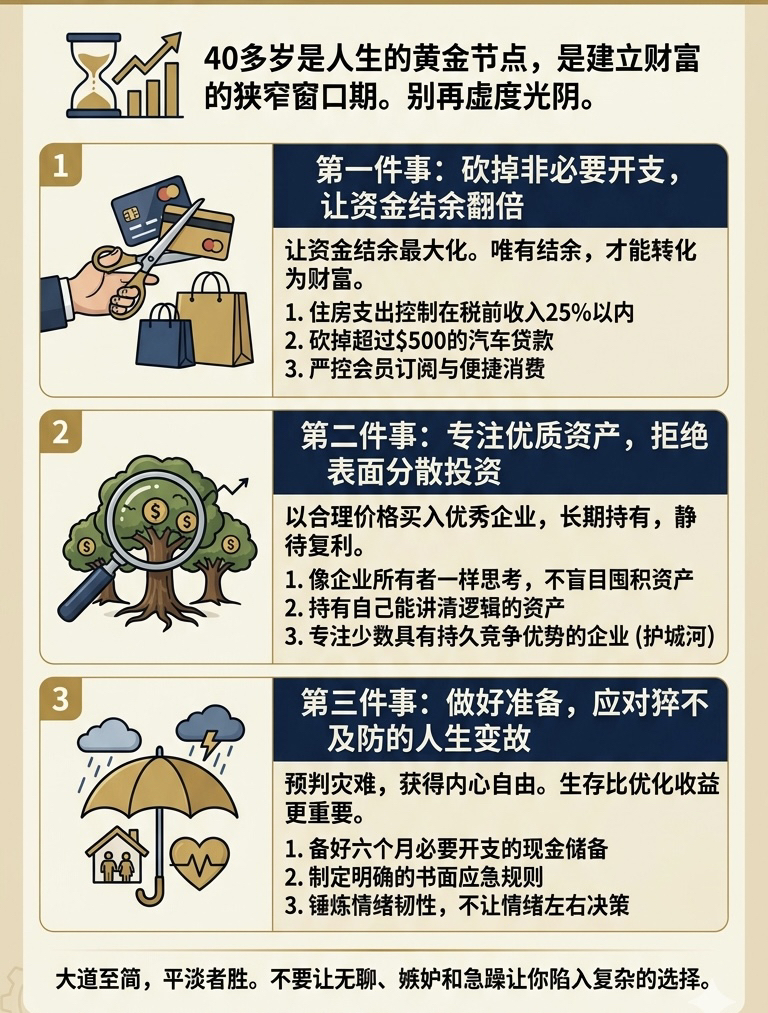

At 40, it is neither a warm-up for life nor a celebration after success. This is a precious and narrow window period where you still hold time, energy, and the ability to make money, but this window closes much faster than you think. Most people will waste these 10 years, chase the wrong goals, get entangled in trivial matters, and always hope that retirement life will improve naturally, but reality never works that way.@币安中文社区

I've spent my entire life studying why intelligent people often make foolish decisions. And for those around 40, my advice is straightforward and painfully honest: Stop deceiving yourself into thinking you have unlimited time, and stop treating your investment portfolio as a hobby to be managed carelessly. You need to learn to make decisions like someone who truly understands investing. Understand that the effects of compound interest require time to accumulate, and you no longer have decades to waste.

If you're over 40 and constantly feel like you're falling behind in terms of wealth, that's actually a good thing. This anxiety and unease is the beginning of facing reality. But if you're complacent, it's time to be alarmed. The comfort of being 40 often doesn't come from real wealth, but rather from being blinded by debt and an overly extravagant lifestyle.

Today I'll break it down for you: if I were 40 years old right now, with 20 years of golden money-making opportunities at my disposal, and I still had the chance to make a wealth plan before it's too late, what three key actions would I take?

Life at 40 is fundamentally different from life at 30 or 50. At 30, you have plenty of time, but not necessarily a stable income; at 50, you may have a considerable income, but your time and energy are far less than before. 40, however, is the golden age of life. You can still work hard to earn money, you still have the ability to recover from investment mistakes, and there's still enough time for compound interest to grow a decent principal into substantial wealth.

First, you must give up three things that cause most 40-year-olds to fall into financial trouble.

First, they always felt that their income would continue to rise, so they lived extravagantly.

Second, understand diversified investment as holding 15 assets that you know nothing about.

Third, they insist on waiting until everything is absolutely certain before taking any action.

These are three things I've always abhorred. I'll tell you to learn to live frugally during your peak earning years, to only hold assets whose logic you can explain, and to view uncertainty as an entry fee for investment, not an excuse for procrastination. This isn't some motivational platitude; it's the most practical survival rule for those who hesitate to take wealth seriously.

1. Cut non-essential spending in half

The first thing to do is cut unnecessary expenses in half, doubling your savings. This might sound uncomfortable, but that's exactly the effect I want. A comfortable life always comes at a high price, and at 40, you simply can't afford it.

As people approach 40, their lifestyles inevitably tend to expand. Every raise, bonus, and windfall will be consumed by this inflated lifestyle. You might think you're just living comfortably, not extravagantly, but behind this comfort lies a high-cost lifestyle you've designed for yourself, requiring you to maintain your current income level indefinitely, or else you'll face hardship. Such a life is far too fragile.

I always advocate for stability. True stability means that even if your income suddenly drops by 30% tomorrow, your life can still function normally. If this idea terrifies you, it only means that your lifestyle has already exceeded your capabilities. To solve this problem, don't wallow in guilt, but rather drastically streamline your budget, distinguishing between what you truly value and those expenses you have to pay due to inertia, saving face, or laziness.

Most people in their 40s are actually paying for three different lifestyles simultaneously: the lifestyle they are currently living, the lifestyle they feel they should be living, and the lifestyle they're too lazy to reflect on and just drift through. Give up the latter two, hold onto the lifestyle that allows you to sleep soundly at night, and then save the money you save.

Here's a simple yet brutal test: Subtract your actual cost of living from your after-tax income—that is, how comfortably you could manage for 18 months if unforeseen circumstances occurred. The difference between these two figures is your actual cash surplus. If this surplus is less than 20% of your income, then your problem isn't low income, but rather an excessively high cost of living.

I've said before that this is essentially you pouring yourself a drink every month, and treating this consumption as life itself. At 40, your goal shouldn't be maximizing income—of course, the more income the better—but more importantly, maximizing your savings. Because only savings can truly be transformed into wealth.

The income that turns into bills, membership fees, and convenient spending will never generate compound interest; it will simply evaporate silently. This is precisely why most 40-year-olds are constantly bleeding money from their finances without even realizing it. They have six-figure incomes, but their savings are only four figures, and they wonder why their account balances never seem to grow. The answer is simple: you don't actually have any real savings.

Once the surplus problem is solved, all financial difficulties will be resolved. To achieve this, you need to make three decisions, and once made, you must stick to them for life.

1. Keep housing expenses below 25% of your pre-tax income. If you exceed this, either find a way to increase your income or decisively reduce housing costs, no matter how much you love your current neighborhood. Remember, your neighborhood won't pay for your retirement.

2. Completely cut out car loan payments exceeding $500 per month. If a car is straining your finances, you've never bought a means of transportation; you've bought a status symbol. Sell it decisively, drive a regular car for three years, and the money saved will open up more options for the next ten years of your life.

3. Strictly control membership subscriptions and convenient spending. If you spend more than $300 a month on entertainment, food delivery, and various memberships, you're merely consuming yourself with rented pleasure, not truly accumulating happiness. Review every recurring charge; if you forget a subscription, cancel it immediately. If you're offered a new subscription now and wouldn't choose it, cancel it immediately. Even if it's only $10 a month, cutting five such expenses will give you an extra $600 in investment funds each year. Persist for ten years, and this accumulation will give you a whole year of freedom at age 55.

But I want to emphasize that this is absolutely not about pretending to be poor, nor is it about deliberately living a hard life when you're actually wealthy. It's about choosing to be someone who values future freedom more than outward appearances. I've lived in the same house for decades, and Buffett drives an old car. We're not stingy; we just never see spending money as a victory. You're not cutting away life itself, but rather excess fat. Only in this way can the muscles of wealth truly grow. And the muscles of wealth at 40 are your savings rate, your investable surplus funds, and your ability to weather adversity without having to sell future assets at a discount.

2. Focus on high-quality assets

The second point is to focus on high-quality assets and reject superficial diversification. By your 40s, you've probably heard the term "diversification" countless times. People around you are always telling you to spread risk, buy a little of everything, and never put all your eggs in one basket. For those who don't understand investing, this advice seems reasonable. But if you've spent time studying the true operating logic of businesses, I'll tell you that excessive diversification is merely an escape from your own ignorance, and ignorance can be changed.

At 40, you simply don't have time to research and hold fifty assets you know nothing about. However, you have ample time to deeply understand five, six, or even seven or eight high-quality companies, then patiently hold them and wait for the compounding effect. This is what I call a focused strategy, and it's the core method by which Warren Buffett and I accumulated enormous wealth. $BTC $ETH

We never buy index funds and leave it to chance. Instead, we buy excellent companies at reasonable prices, ignore all headlines, market crashes, and our own doubts, and hold them for the long term. This isn't gambling; it's patience built on deep understanding.

As you approach forty, you need to undergo this mindset shift: stop blindly hoarding assets like a collector and start thinking like a true owner. True asset owners ask entirely different questions. They don't ask what assets are hot right now; instead, they ask, "If the market closes tomorrow, would I be willing to hold this company for ten years?" They don't ask what everyone is buying; instead, they ask if the company has pricing power, low capital requirements, honest management, and products that people will still need ten years from now.

If the answer to these questions is no, no matter how cheap it seems or how much it's touted online, don't touch it.

If the answer is yes, then buy at a reasonable price and do the hardest thing in investing: do nothing and let your assets grow naturally while you focus on living your life. Don't check the market every day, don't trade frequently out of boredom, and don't easily sell just because your brother-in-law says a certain asset is more profitable. You choose to hold only because you truly understand it, and only because time is the core factor that transforms high-quality companies into exceptionally high returns.

Here I want to clarify that "high-quality" does not refer to stocks with high prices, but rather to companies with a sustainable competitive advantage—what I call a moat. This moat can be a brand trusted by consumers, a network effect where the advantage becomes more pronounced with scale, a cost structure that competitors cannot match, or an industry regulatory advantage that deters new entrants.

If you can't explain a company's competitive advantage in just two sentences, it means your understanding of it isn't deep enough, and you're not qualified to hold its shares. That's my selection criterion. And once you honestly apply this criterion, the number of viable investment targets you have will rapidly decrease, which is a good thing. A small group of truly well-understood high-quality companies is far more valuable than a long string of mediocre assets bought simply to follow the trend.

I'm always very decisive about my list of challenging targets, and most investment ideas end up on this list. I'm never embarrassed by it; on the contrary, I'm proud of it. Because in investing, avoiding bad ideas is far more valuable than finding good ones.

Of course, this doesn't mean you should completely abandon diversification. Rather, it means spreading risk among a few high-quality assets, rather than blindly diversifying among fifty stock codes you can't even name. Five, six, or even seven or eight high-quality companies held long-term are likely to yield returns far exceeding those of thirty assets you know nothing about, especially after deducting taxes and fees.

For someone in their forties, taxes and transaction fees are not trivial details; they directly determine whether you retire comfortably at sixty or work until seventy. Every frequent transaction is a tax event, and every mutual fund with an annual fee rate of two percent is your hidden partner, taking away twenty percent of your returns over ten years. I've always disliked paying for mediocre operations, but I'm willing to pay for patience, and you should do the same.

Here's what you can do next: Open your current portfolio, write down each holding, and next to it, write a sentence explaining why you hold it and how that business truly makes money. If you can't write that, then you're not investing, you're just guessing. Either sell it, or spend a weekend researching until you can write that sentence.

Then, for each remaining asset, ask yourself: if I didn't already own it, would I buy it at the current price? If the answer is no, sell it decisively; if the answer is yes, hold on, set a calendar reminder, and check back in six months. Six months, not six days—this is the rhythm of an asset owner, not a trader. Traders constantly pay fees and taxes, while owners quietly reap the rewards of compound interest.

One more point to clarify: if you find stock picking too difficult and time-consuming, and prefer to hold low-cost index funds that provide access to hundreds of high-quality companies without needing to be an analyst, that's perfectly fine, and I endorse that choice. The key is to understand what you're holding, why you're holding it, and not to pay exorbitant fees to have others guess for you.

Holding a low-cost broad-based index fund for twenty years will outperform most actively managed funds, far surpassing the returns of indecisiveness and stagnation. At forty, the worst choice you can make is not investing in the wrong assets, but rather doing nothing while waiting for certainty. Remember, there is no absolute certainty in this world, and doing nothing exposes you to the greatest risk: uncertainty.

3. Be prepared to deal with unexpected life changes.

As people reach their forties, life often throws out a variety of costly surprises: elderly parents needing care, children needing proper tutors or going to university, layoffs lasting longer than three months, sudden health problems, leaky roofs, broken gearboxes, and even friendships broken by money.

If you're not prepared for these unexpected events, it's not planning at all; it's just wishful thinking, and wishful thinking is never a life strategy for a forty-year-old. I often say you need to learn to anticipate disasters. This may sound negative, but it can actually bring inner freedom. When you've prepared for the worst, you won't be caught off guard by unexpected events; instead, you can handle them calmly. This calmness depends on three things: having cash on hand, clear rules, and cultivating emotional resilience.

First, prepare cash. You need to keep enough cash in a regular savings account for six months of essential expenses, even if the interest is low. This money cannot be used for investment or withdrawn through a credit line; it is real liquid capital, cash you can access within 72 hours should your life change.

Why six months? Because the plight of layoffs won't be resolved in four weeks, the cost of caring for parents won't magically decrease, and roof and gearbox repair costs won't be negotiable. If your current cash reserves are less than six months' worth, start accumulating now, even if it means halting investment for two quarters.

I know this idea sounds heretical in an environment where everyone is urging others to invest every penny immediately, but I'll tell you that survival is far more important than optimizing returns on the path to wealth accumulation. If you're forced to sell assets during the worst market conditions because you lack a cash buffer, there's no possibility of compound growth. Cash is never a drag on returns; rather, it's the foundation that allows you to protect your investment returns when storms come.

Secondly, establish clear rules. By forty, you need to write a simple plan outlining how you will respond to unforeseen circumstances. What should you do first, second, and third if you lose your job? How much can you afford if your parents need financial assistance? What are the absolute boundaries that cannot be crossed? If your child wants an expensive item, how do you determine if it's a necessity or just a desire?

These conversations may not be easy, but if you don't make these agreements before an emergency occurs, unforeseen circumstances will make the decision for you, and the cost of that decision is often shockingly high. I have always believed in the power of prior commitment. By setting your principles in advance, you can simply execute them when unforeseen circumstances arise, rather than making hasty decisions under pressure.

Write down your rules: never take on new debt unless absolutely necessary. Never liquidate your retirement account unless absolutely necessary. Never act as a loan guarantor for anyone, not even family members. Whatever your rules are, write them down and review them annually. This piece of paper is your emotional firewall, allowing you to protect your financial bottom line in times of panic.

Finally, there's the cultivation of emotional resilience. This is also the most easily overlooked point. Life at forty is inherently filled with emotional turmoil. You're mature enough to clearly see the gap between your past life goals and your current reality. You watch your friends; some become rich overnight, while others suffer utter ruin. You suddenly realize that parents aren't immortal, and children won't always need your care. You feel a weariness you never felt at thirty, and even the courage to start over feels incredibly heavy. And all of this is the most real aspect of life.

I won't tell you to ignore these feelings; I'll tell you to accept them and then act decisively. Emotional resilience isn't about pretending everything is fine, but about deciding not to let your emotions control your financial decisions. Act according to plan whether you're anxious or excited. This isn't indifference; it's maturity. And this maturity is precisely the advantage you, at forty, possess that young people can't match.

A harsh reality is that if you're over forty and not prepared for these life-changing events, you'll soon pay a heavy price. Those who easily navigate their forties are either extremely lucky or already wealthy. Most of us need to live with sufficient clarity and planning. This planning is reflected in every aspect of life:

• Keep housing and car expenses within a reasonable range to prevent unemployment from becoming a crisis.

• Continuing to hone your professional skills will ensure you find a new job within ninety days.

• Cultivate good interpersonal relationships so that you can ask for help without feeling ashamed when you need it.

• Take good care of your health and don't let yourself become a ticking time bomb of medical bills.

• Keep your finances simple enough to be explained on a single page.

• Lower your pride so that you can frankly admit your mistakes and quickly adjust your course.

Similarly, at forty, you also need to know what things you absolutely must not do; this is just as important as doing these three things well:

• Don't try to time the market. You have neither the ability nor the mindset to do so, and even if you did, the effort would be far from worthwhile.

• Don't take on new debt to maintain your lifestyle; if you can't afford to pay in cash, it means you can't afford it at all.

• Do not act as a loan guarantor for anyone, not even family members. Show your love in other ways; do not tie your credit to someone else's choices.

• Don't neglect your health in pursuit of extra income; the cost of an emergency room visit is far more expensive than the time you save.

• Don’t outsource your financial decisions to people who earn commissions from your choices. You can seek advice, but the final decision must be made by yourself.

• Don't wait for so-called absolute certainty or the perfect timing. The best time was ten years ago, and the second best time is now.

• And one more crucial point: don't treat your house like an ATM. I know your home equity is what it is, I know the temptation to refinance cash is tempting, and I know current interest rates may be relatively favorable, but don't do it. Your home equity is neither your emergency fund nor your investment capital; it's the stable foundation of your life. Once you start cashing out your house to cover other expenses, you're leveraging your life. And leveraging your life at forty is never a good deal. Keep your house simple: pay off the mortgage as soon as possible, and if not, make payments on time. Don't touch it lightly.

Second, we will now create a detailed 90-day action plan for you so that you can take immediate action:

• Week 1: Calculate your actual cash balance, which is income minus essential expenses. If the balance is less than 20%, immediately identify your three biggest financial leaks and address one of them immediately.

• Week 2: Conduct a comprehensive review of your investment portfolio. Write a one-sentence explanation of your reasons for holding each stock and the company's profit logic. If you can't write one, either conduct in-depth research or sell it decisively.

• Week 3: Check your cash reserves. If they are less than three months' worth of essential expenses, suspend new investments and focus on accumulating reserves until you have enough for six months.

• Week 4: Write down your emergency rules on a piece of paper, clearly outlining how to deal with unexpected events such as unemployment, needing to care for parents, or vehicle breakdowns, and place this paper in a prominent place.

Week 6: Proactively negotiate a fixed expense by calling insurance companies, internet service providers, and phone operators to negotiate better prices or switch service providers. Add the savings directly to your automatic investment plan. If possible, even if you're short on cash, increase your automatic investment amount by 5%.

Week 7: If you have a partner, have a deep financial conversation with them, lay all the numbers out on the table, and reach an agreement on financial bottom lines, cash reserves, and rules of conduct. If you are single, write these thoughts down and make a commitment to yourself.

Week 8: Update your beneficiary, will, and insurance information. If someone depends on your income and you don't yet have term life insurance, be sure to purchase it this week. Cut one major discretionary expense for the quarter, such as a membership or a spending habit, and put the savings into an emergency reserve or investment account.

Week 9: Examine your career and consider whether your skills are still competitive in the market. If you lost your job tomorrow, could you find a comparable job within 90 days? If the answer is no, spend 10 hours this month making up for the deficiencies: take a course, update your LinkedIn profile, and chat with people in your industry over coffee.

• Week 10: Conduct a disaster drill, pretending you've just been laid off, review the budget, write down the expenses to be cut on day one, prepare in advance, and avoid last-minute panic.

• Week 11: Review the execution of this 90-day plan. Has your cash surplus increased? Have your cash reserves grown? Have you adhered to the rules you set for yourself? If the answer is yes, quietly celebrate for yourself; if not, find the problem and adjust your living environment instead of lowering your goals.

Week 12: Write a one-page letter to your 50-year-old self. Write down the goals you hope to achieve in ten years, the efforts you are grateful for in your 40-year-old self, and the things you regret not starting sooner. Keep this letter safe and read it once a quarter to constantly remind yourself why you started.

I want to tell you that when you actually start implementing this plan, you may feel poor for the first sixty days, but that's normal. You're not really poor; you're just shifting resources from trivial things to things that are truly important. And the human brain naturally resists change, so just get through it.

• By the fourth month, you will emerge from this feeling of poverty and your mind will become incredibly clear.

• By the eighth month, you will find that your account balance begins to grow like never before. At this point, you will realize that your financial problem has never been that your income is too low, but that there is a problem with the structure of your life.

• By the second year, people around you will start asking what has changed, and you may not know how to explain it, afraid of sounding preachy. That's okay, just let them guess.

• By the fifth year, you'll see the numbers in your account that make you stop and think, "Wow, I really can live a good life," and that moment is worth all the mundane and boring days you've spent working towards.

If I were sitting across from you at forty, I would say this: You've never fallen behind; you're at the right point in time, provided you stop pretending you have plenty of time. I would say the next ten years are more important than the past twenty, because these are the ten years you can still firmly control. I would also say that the goal of life is never to get rich quickly, but to become rich slowly, then preserve that wealth, and ultimately leave this world with the freedom to choose.

The method to achieve this goal is actually extremely simple: live within your means, hold quality assets, avoid foolish decisions, and remain patient when everyone else is panicking. This method is neither fancy nor complicated.

This method won't make you a genius in the eyes of everyone at a dinner party by speaking eloquently, but it is undeniably effective. It led me to financial freedom and helped Buffett achieve his life's dream. If you're willing to follow it, it can also give you the life you desire.

Turning forty is never a second chance in life, but rather your last and most precious opportunity to build lasting wealth before variables like time, energy, and health start to turn against you. At this moment, time, energy, health, and compound interest are still on your side; it's just that the clock is ticking faster and faster.

If you can hear this bell, that's good; use it as motivation. Cut unnecessary expenses, focus on your investment portfolio, prepare for all eventualities, and then quietly wait for your plan to take effect. Don't let boredom, envy, and impatience drag you into complicated choices. Simplicity is the ultimate sophistication; the ordinary triumphs. When you're in your sixties, and your friends are scrambling to make ends meet while you remain calm and composed, you'll be incredibly grateful to the version of yourself that made countless ordinary yet correct decisions in your forties.