Two key market dates are hitting at 8:30 am ET on Thursday, April 30 carry the combined weight of the Federal Reserve’s rate path through the second half of 2026: Q1 GDP, where consensus is anchored at 1.8% annualized growth, and core PCE inflation, where Barclays economist Pooja Sriram forecasts a month-over-month print of 0.24% to 0.28%, translating to 3.1% year-over-year in the stronger reading.

Both numbers land the morning after Jerome Powell’s final FOMC press conference as Fed Chair, when CME FedWatch assigns a 99.0% probability that the central bank will keep the federal funds rate target range at 3.50% to 3.75%.

March PCE Price Index seen having risin 0.7% in March… due out Thursday morning core +0.3% pic.twitter.com/qpzvt3zpKQ

— Mike Zaccardi, CFA, CMT (@MikeZaccardi) April 26, 2026

If there’s any deviation from the consensus on either release, we’ll reprice that rate path immediately. The sections below examine the Q1 GDP mechanism and what a miss or beat means for rate-cut timing; the role of core PCE as the Fed’s preferred inflation gauge; the scenario framework around Thursday’s print; and the combined market implications for Treasury yields, rate-sensitive equities, and portfolio positioning through 2026.

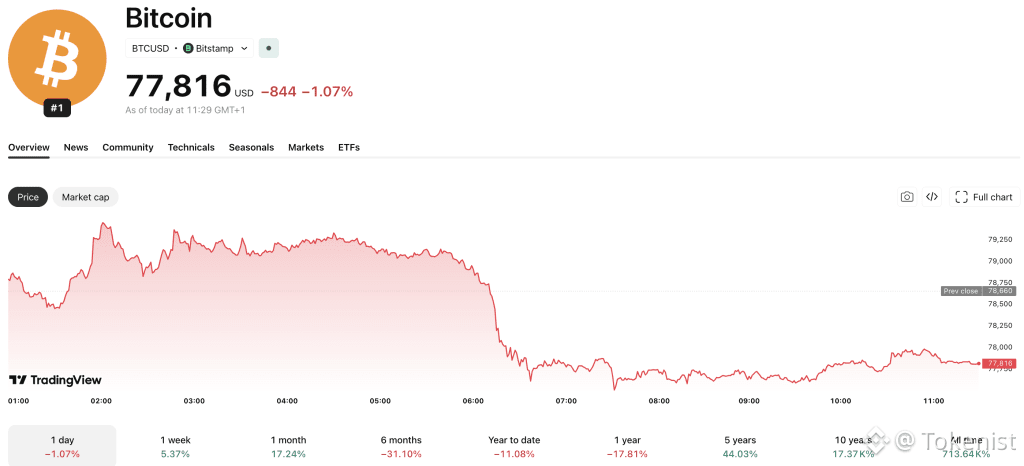

This data is due to drop as the Bitcoin price sits flat over the past 24 hours, dropping just -0.3% to $77,700, with $77,000 needing to hold for any hopes of a continuation of the recent market-wide crypto rally.

SOURCE: TradingView Market Dates: Q1 GDP at 1.8% – What a Miss or Beat Means for Rate Cut Timing

SOURCE: TradingView Market Dates: Q1 GDP at 1.8% – What a Miss or Beat Means for Rate Cut Timing

The consensus estimate for Q1 growth is 1.8%, a significant slowdown from the 3.8% seen in Q2 of the previous year. A reading above 2.0% indicates that the economy is managing the current 3.50% to 3.75% rate environment, potentially pushing any Fed pivot into 2026 and reducing the likelihood of rate cuts in June or July.

Conversely, a figure below 1.5% could intensify concerns about a hard landing and prompt the markets to anticipate 25 to 50 basis points of additional easing later in the year.

This GDP release’s timing is crucial, as it follows Powell’s likely final press conference, leaving the Fed without context for interpreting the data. Capital Economics notes that slowing growth coupled with inflation above 3% could lead to a stagflationary scenario, limiting the Fed’s ability to cut rates without risking further inflation.

The economic backdrop is not neutral, as energy price volatility stemming from geopolitical tensions complicates the inflation landscape. March PPI showed energy prices surging 8.5% month over month, which may affect core goods and services. If Q1 GDP confirms a slowdown while energy-driven costs persist, the Fed’s options will be significantly constrained, regardless of core PCE results.

Core PCE: Why the Fed’s Preferred Inflation Gauge Is the More Consequential Print

Key Economic Events This Week: Tuesday – April Consumer Confidence Data Wednesday – FOMC Decision and Powell's Press Conference Wednesday – Microsoft, Amazon, Meta, Google Report Earnings Thursday – Apple Earnings, US Q1 2026 GDP & March PCE Inflation Data ~20% of S&P… pic.twitter.com/5l1y7i6zvD

— Cointelegraph (@Cointelegraph) April 27, 2026

Core PCE, the Federal Reserve’s preferred inflation gauge, is expected to show a month-over-month increase of 0.28% or 0.24% in March, influenced by a Bureau of Economic Analysis methodological decision.

Pooja Sriram from Barclays highlighted that the divergence depends on the legal services deflator, with a weaker CPI pulling the core PCE closer to 0.24%. Year over year, it could reach 3.1%, exceeding the Fed’s 2% target.

The implications of the data are significant: a print above 0.30% would reinforce the Fed’s hawkish stance, dampen rate-cut expectations, and push up the 10-year Treasury yield.

An in-line figure at 0.28% would confirm persistent services-sector inflation, while a cooler reading below 0.24% would signal a return to core disinflation, potentially leading to rate cut pricing by July.

The services-ex-energy-and-housing PCE component has kept inflation elevated, with a 0.88% quarterly gain noted in Q4 2025. Despite softer March PPI data, increasing transportation service costs could affect the final PCE print, making it sensitive to how the BEA processes that data. Treasury yields will react promptly to the final figure within Sriram’s range.

What GDP and PCE Together Mean for Rate Expectations and Portfolio Positioning Through 2026

FRED.org

FRED.org

The combined readings of GDP and core PCE will influence the Fed’s decisions before year-end. A weak GDP alongside a high core PCE (e.g., GDP slowing toward 1.5% while inflation stays at 3.1% year-over-year) may put the Fed in a dilemma, leading to market volatility, especially affecting the 10-year Treasury yield.

Sensitive market sectors, including utilities, real estate, and tech, as well as the dollar index, will react based on these data releases. Major market participants seem to be hedging against stagflation rather than betting on a soft landing.

With Powell’s press conference before the data releases, there’s no buffer for the market, which expects no policy change. Moreover, these upcoming market dates and macro data will determine if the market adjusts significantly or just temporarily.

Kevin Warsh’s confirmation could also add uncertainty regarding the Fed’s inflation measures. The April 30 data release, especially concerning Q1 GDP and core PCE, will be crucial for the current tightening cycle.

The author does not hold or have a position in any securities discussed in the article. All stock prices were quoted at the time of writing.

The post Upcoming Market Dates: PCE Inflation & Q1 GDP Determining the Fed’s Next Move appeared first on Tokenist.