Observations and personal views from Nothing Research Partner 0x_Todd, the following content does not constitute any investment advice.

In the age of social media, one benefit is being able to see what well-known investors who are 'living in the news' really think in real time. Recently, many media reports have focused on the (big short) prototype Michael Burry, who previously shorted subprime mortgages in 2008, warning again that there is a big bubble in AI.

We examined his arguments one by one and summarized them as follows:

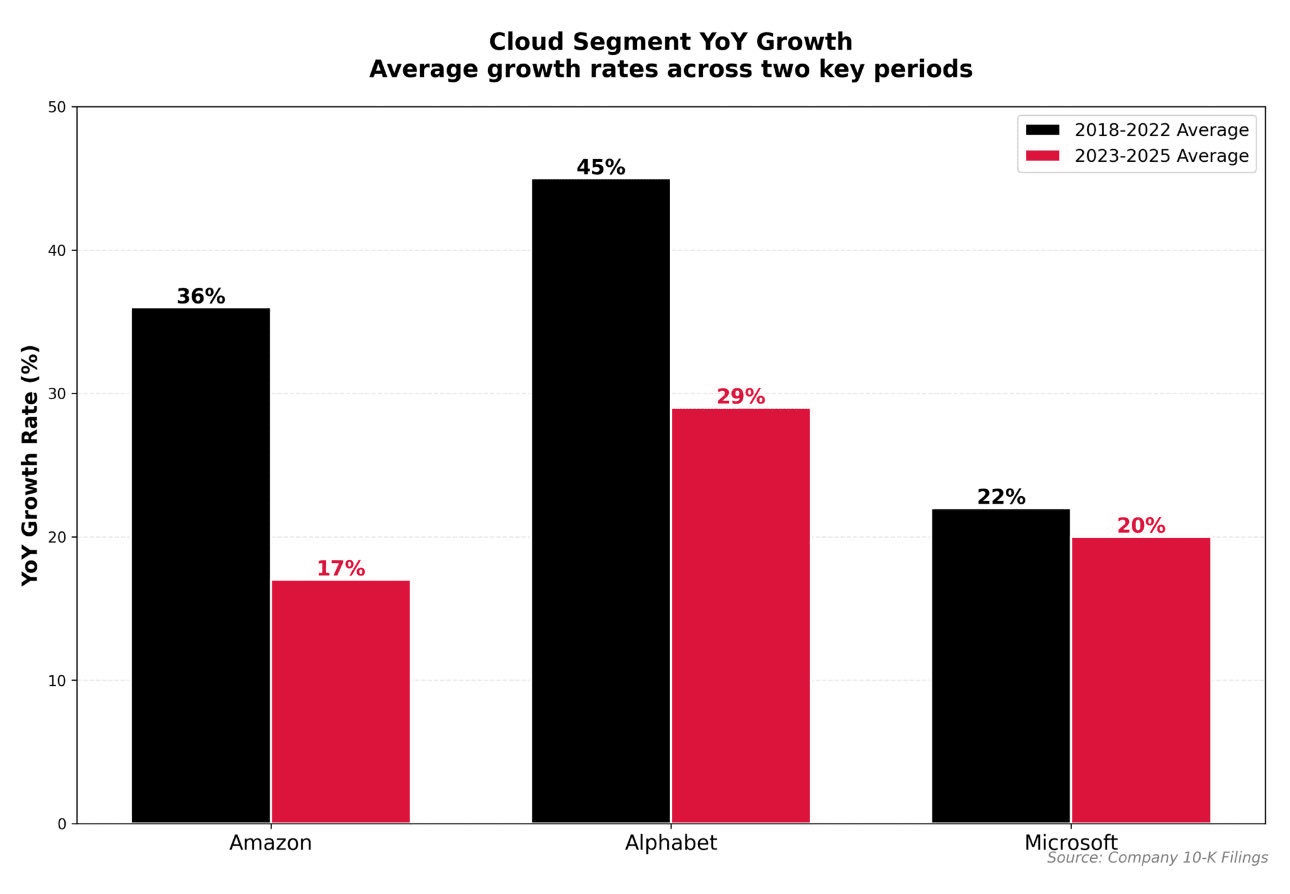

1. The growth of cloud services from Amazon, Google, and Microsoft (2023–2025 vs 2018–2022) is slowing down.

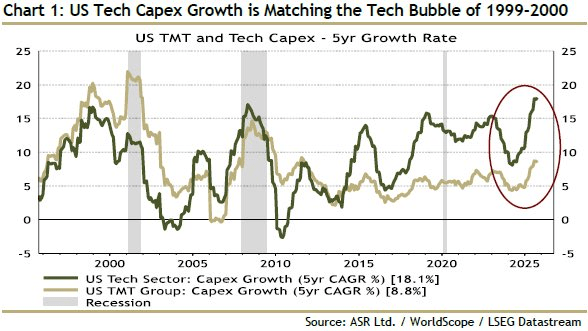

2. Investment in infrastructure by the US tech industry has reached the level of the 2000 internet bubble.

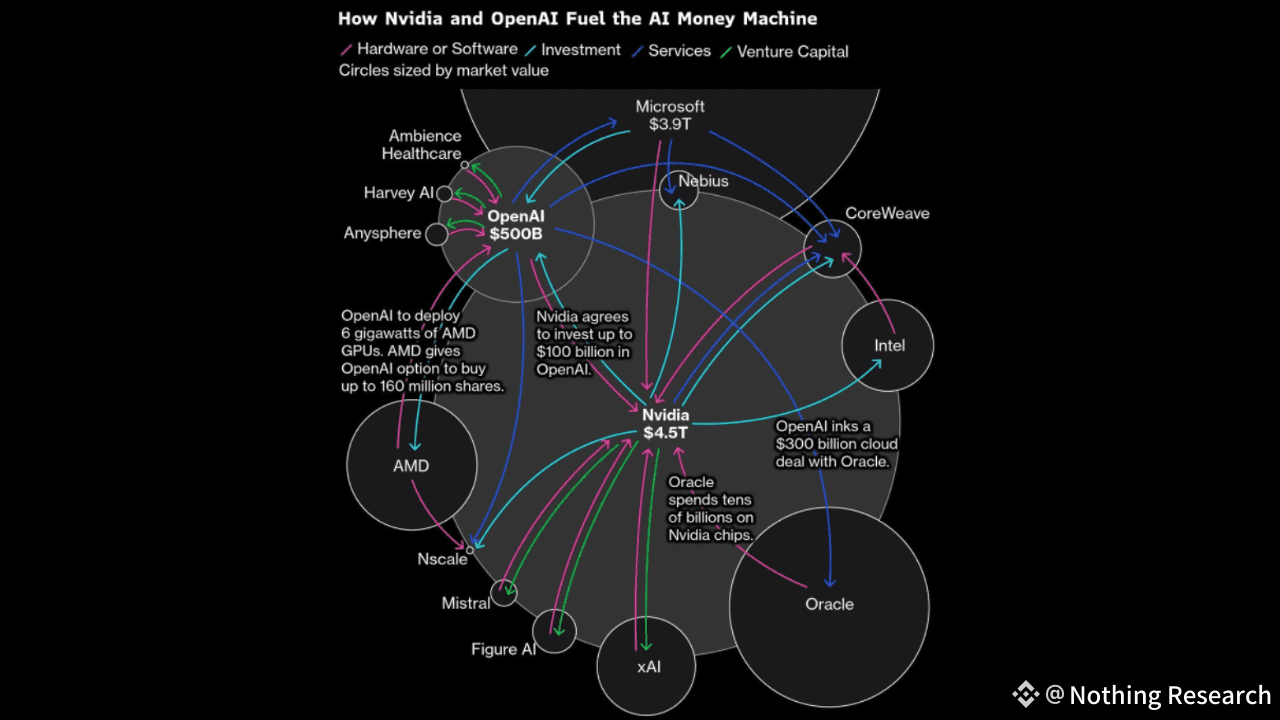

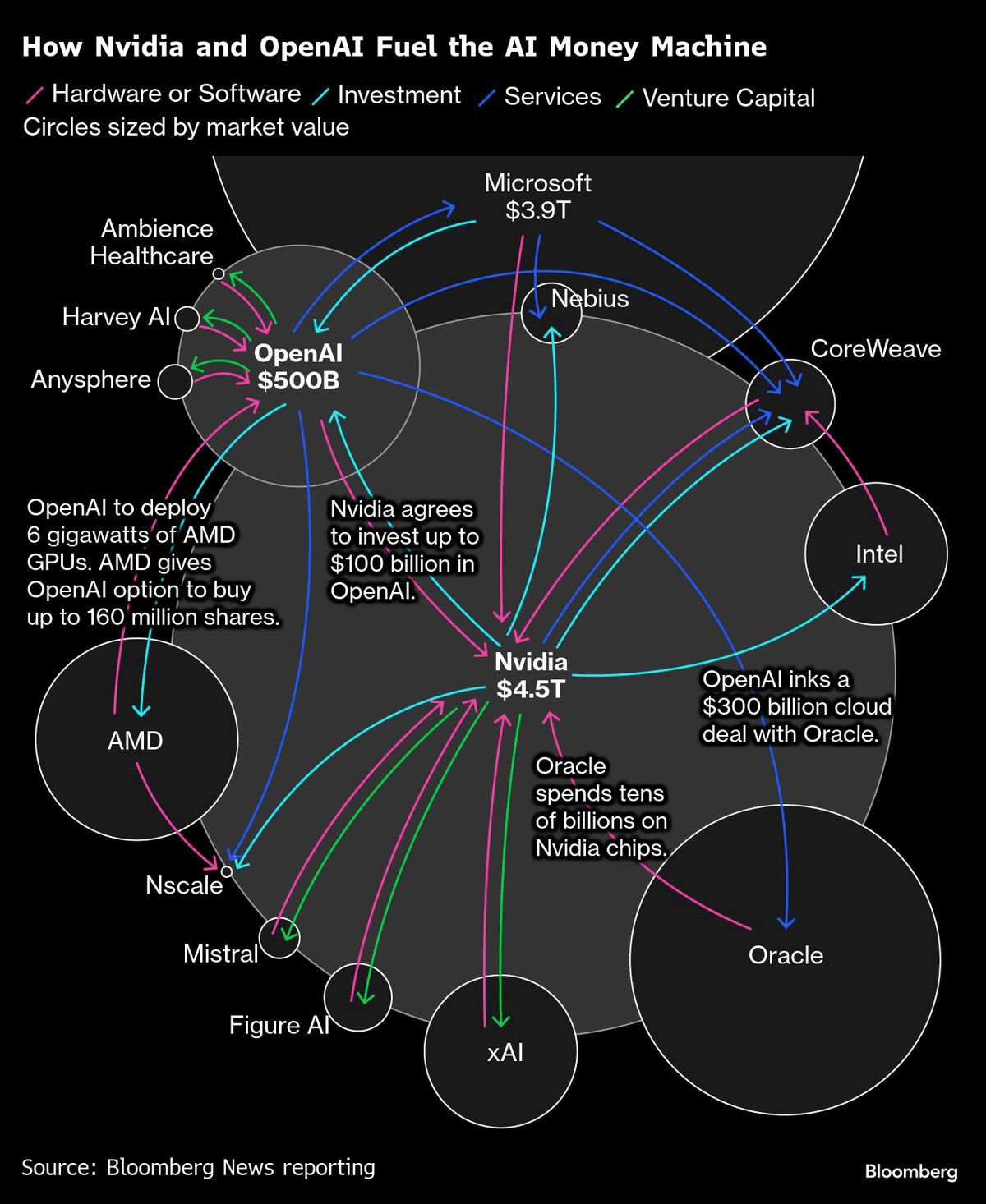

3. Complex cross-investment relationships among Nvidia, OpenAI, Oracle, Intel, etc.

In fact, Chart 1 is not very related to being bearish on AI; the mutual investments among these institutions in Chart 3 are indeed quite messy, but it's also hard to form direct arguments for being bearish.

In fact, a more direct argument is Chart 2, where the Capex growth index measures the speed at which US tech companies are spending money on infrastructure expansion in recent years.

Specifically, it refers to the 'big money' expenditures that companies make for long-term future returns: building data centers, buying machinery, renovating factories, laying networks, purchasing servers, chips, etc., not daily expenses like salaries and rent.

From common sense, people only spend big money when they are floating, engaging in that kind of ethereal infrastructure, so a high value indicates a bubble.

To deepen understanding, Burry also thoughtfully attached a segment:

"By 2002, it was commonly reported that the capacity utilization of US telecommunications was below 5%. Thousands of miles of expensive fiber optic networks remained buried underground, unlit. Fifteen continental telecom networks, each providing essentially indistinguishable services, were struggling for survival."

But the problem is, regarding Chart 2, our views are completely opposite to Burry's. The infrastructure for AI is mainly data centers and GPU computing power, which, at least for now, are certainly not the expensive unlit fiber cables; computation power is currently very scarce.

It can be said that these chips are just barely sufficient for text-based GPT usage. How big is the gap before everyone can use Sora2? Moreover, this gap has not yet been filled, and humanoid robots are coming.

Now everyone is even discussing investing in power plants, because the power consumption of AI can't keep up, do you think this gap is large?

AI definitely has a bubble, but you can't use the old lessons from 20 years ago to seek a solution.

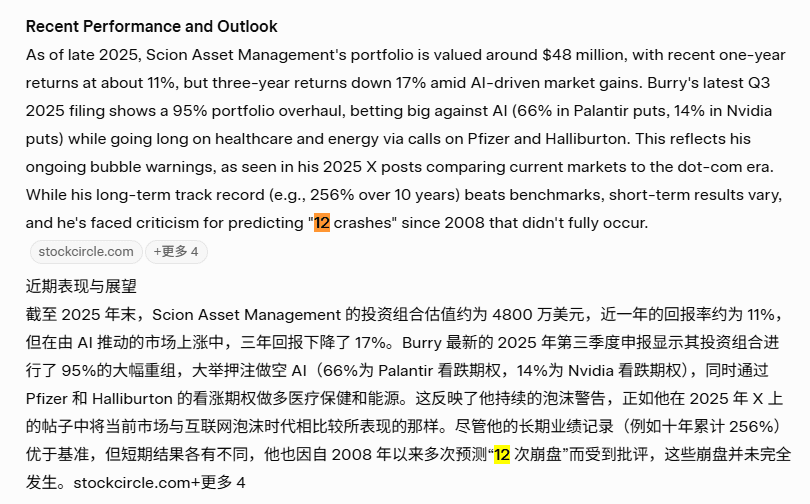

Burry is 53 this year, overall, Burry is definitely a relatively impressive investor. According to GPT's analysis, his fund and personal wealth should have outperformed the US stock market over time.

Unfortunately, after making a big profit in 2008 (about 100 million USD for himself + 700 million USD for clients), over the last twenty years, he has issued 12 warnings of a crash, most of which did not materialize, such as when he shorted Tesla.

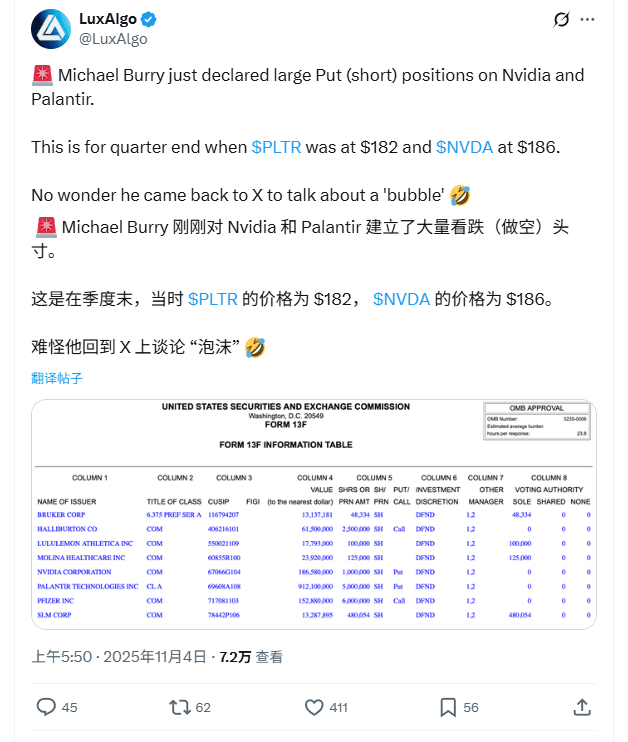

This time, he returned to Twitter (yes, he was out of touch for a while), and someone found that he had built a large position in many Nvda put options. Of course, actions speak louder than words; if you're shorting, you have to promote it, which is very normal.

However, when he has not provided more compelling evidence, we feel that the current logic cannot convince me.

Considering the huge gap in computing power for humanity, which is continuously creating new demands, continue to dollar-cost average in chip ETFs, buy small on small dips, and buy large on large dips.