Access Binance OTC desk on the VIP Portal

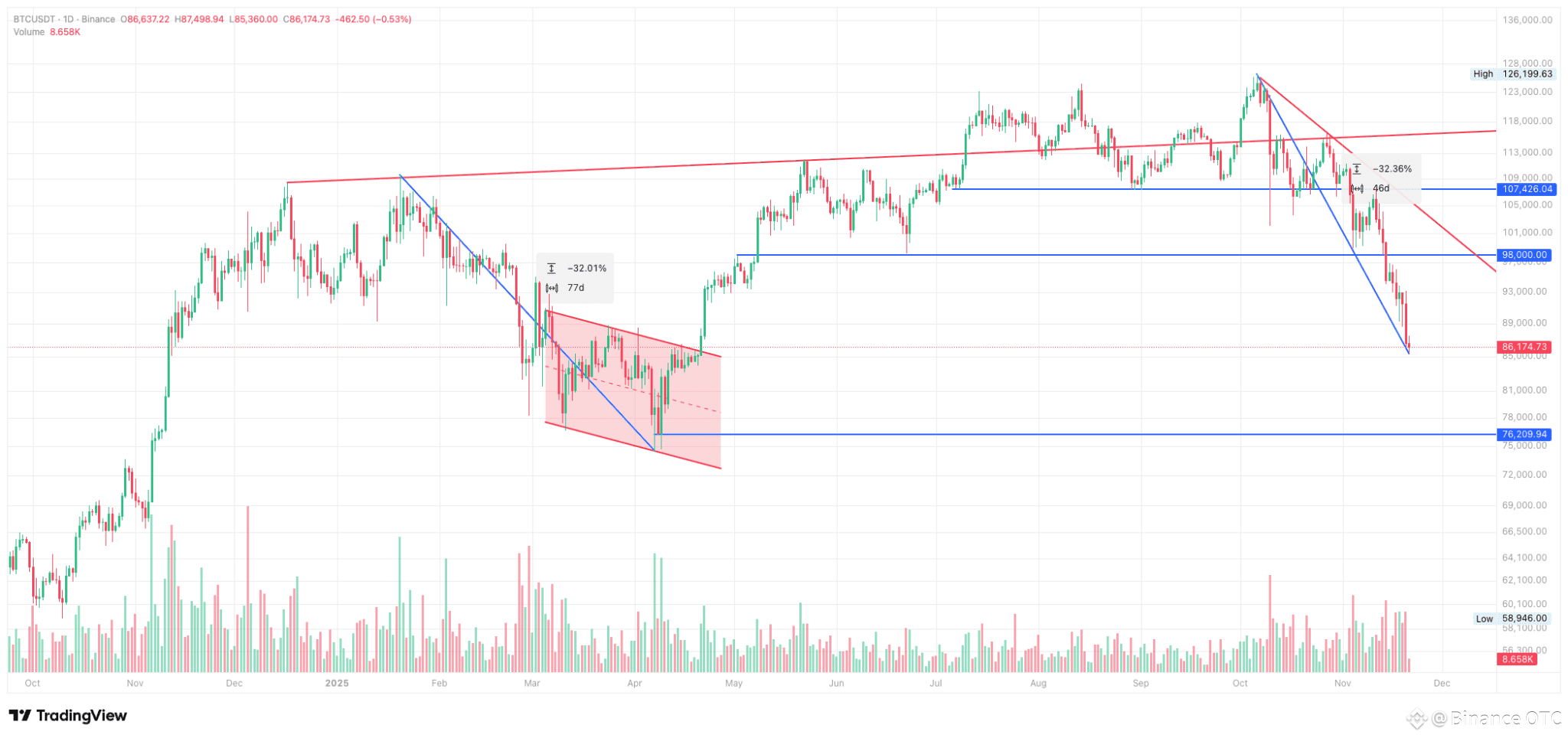

Overall Market

Data source: TradingView

In our previous report, we highlighted key observations from the options market and expressed optimism for potential support at the $98,000 level for Bitcoin ($BTC). This level provided temporary support around November 4, driving a rebound to approximately $107,000. However, market dynamics took a divergent path, with BTC swiftly breaching the $98,000 threshold and accelerating downward momentum. The selloff occurred despite initial optimism surrounding the U.S. government's reopening on November 13 following a 43-day shutdown—the longest on record. As of today, BTC is trading near $86,700, reflecting a broader pullback from its November highs above $110,000.

Global liquidity conditions remain under pressure, influenced by shifts in sovereign bond yields. The Japanese 10-year Treasury yield eased to approximately 1.78% as of November 21, following a peak near 1.82% earlier in the week. This movement has drawn capital inflows back to Japan, contributing to tighter liquidity worldwide. In the U.S., the delayed September labor market data, which was originally slated for October but postponed due to the government shutdown, was released on November 20, revealing 119,000 jobs added and an unemployment rate rising to 4.4%. While interpretations vary, the report underscores a resilient labor market, reducing the likelihood of a 25-basis-point Federal Reserve rate cut in December. Meanwhile, the U.S. 10-year Treasury yield is hovering between 4.09% and 4.13%, signaling investor caution amid persistent inflation concerns.

Liquidity dynamics have dominated market movements this week. Despite NVIDIA's robust third-quarter earnings reported on November 19—featuring $57.0 billion in revenue (up 22% sequentially) and $1.30 adjusted earnings per share, the broader market erased initial gains and resumed its downward trajectory during U.S. trading sessions. Our analysis indicates that selling pressure intensified during U.S. hours, exacerbated by significant capital outflows from Bitcoin and Ethereum ETFs. November has seen net outflows exceeding $3 billion for BTC ETFs alone, including a record $523 million single-day redemption from BlackRock's IBIT on November 18, dragging the cryptocurrency sector lower.

As noted in our prior analysis, the correlation between BTC and the Nasdaq Composite remains elevated, reaching approximately 0.80 on a 30-day basis, the highest since 2022. This linkage heightens BTC's vulnerability to downside risks in a liquidity-constrained environment. Under current conditions, crypto assets exhibit heightened sensitivity to liquidity shifts, as investors prioritize de-risking by divesting from high-volatility assets amid changing risk appetites.

Technical analysis suggests that the next strong support for BTC is around the $74,000 level over the coming months, a level that provided resilience during the U.S.-China tariff escalations in April 2025. In the near term, we maintain a cautiously optimistic stance on a potential BTC rebound over the next few weeks, contingent on positive ripple effects from the U.S. government reopening, such as stabilized economic data releases and reduced policy uncertainty. Investors should monitor upcoming indicators, including the delayed November jobs report on December 16, for further insights into Fed trajectory and liquidity trends.

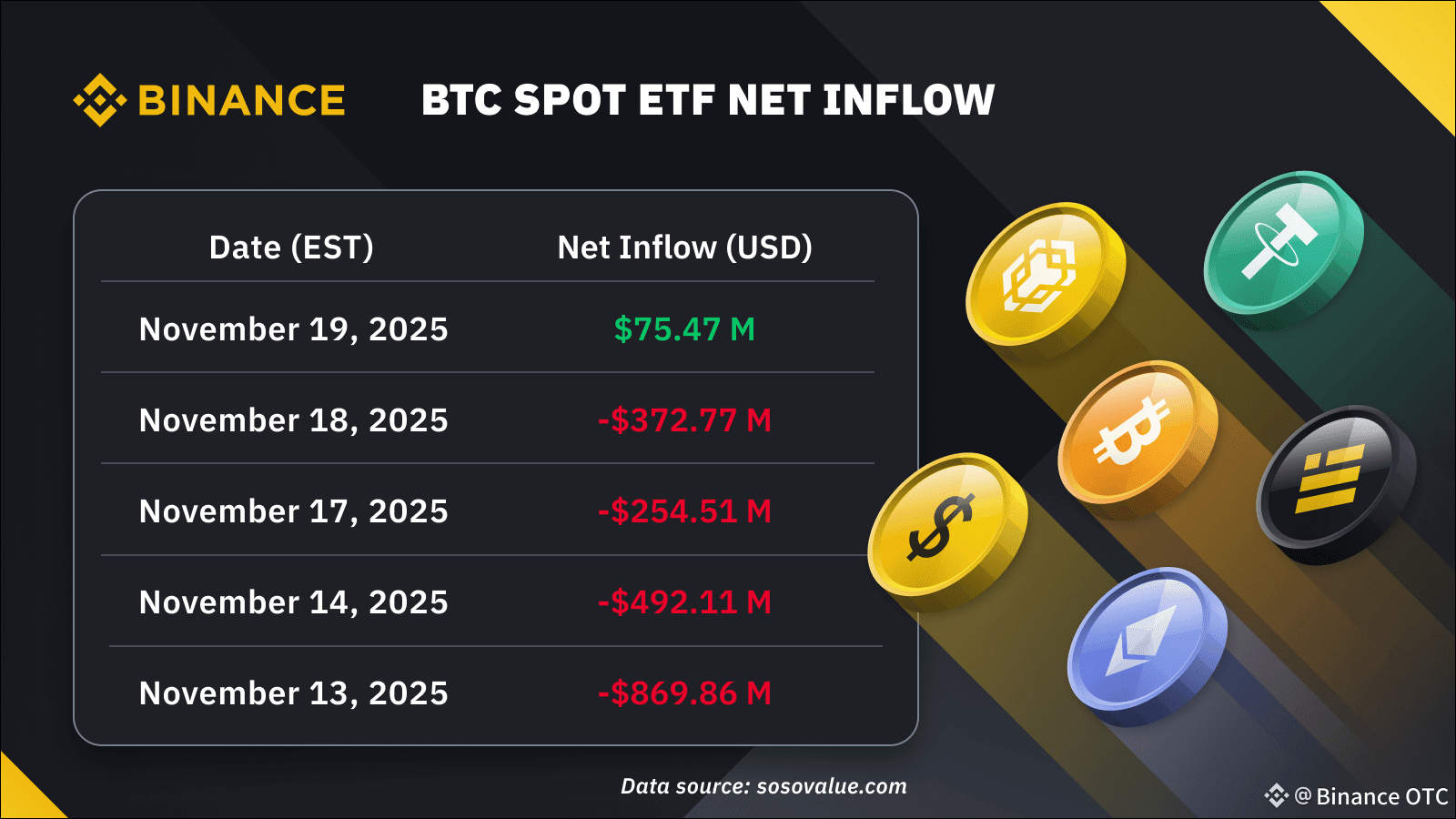

Bitcoin ETF Tracker

The above table shows the daily BTC spot ETF net inflow data for the past five trading sessions.

As outlined in our "Overall Market" section, tightening liquidity conditions were a pivotal factor in this week's broad sell-off across cryptocurrency markets. Investors accelerated capital withdrawals from crypto-related assets, resulting in net outflows about $2 billion from U.S. spot Bitcoin ETFs over the five-day streak ending November 19. This trend reversed modestly on November 19 with $75.47 million in net inflows, led by BlackRock and Grayscale.

Given Bitcoin's inherent sensitivity to liquidity fluctuations as a high-risk investment asset, its performance this week lagged significantly behind other asset classes. Initial optimism around global liquidity has been tempered by movements in the Japanese 10-year Treasury yield, which hovered around 1.78%–1.82% as of November 21 after a brief uptick earlier in the week. Coupled with a sharp decline in the probability of a 25-basis-point Federal Reserve rate cut in December, this has heightened uncertainty. The minutes from the FOMC October 28–29 meeting, released on November 19, revealed deep divisions among officials regarding the pace of rate adjustments, with debates centering on balancing labor market risks against persistent inflation pressures. These factors suggest a broader market shift toward risk-off sentiment, even as NVIDIA delivered exceptional third-quarter earnings on November 19..

Macro at a glance

Thursday, Nov 13,

Australia's employment increased by 42,200 jobs in October, exceeding the market forecast of 20,000. The unemployment rate declined from 4.5% to 4.3%. This robust labor market performance signals resilient domestic demand amid global uncertainties, reducing the urgency for the Reserve Bank of Australia (RBA) to cut interest rates. It strengthens the case for maintaining the current policy rate through 2025, potentially supporting AUD appreciation and bolstering consumer confidence, though persistent wage pressures could fuel inflationary risks.

Friday, Nov 14,

French CPI consumer prices rose 0.1% month-over-month in October, aligning with preliminary estimates after a 1.0% decline in September. Year-over-year inflation eased to 1.0%.

Eurozone GDP preliminary estimates for Q3 2025 confirmed a 0.2% quarter-over-quarter growth, with year-over-year growth revised upward to 1.4% from the initial 1.3% flash estimate.

Monday Nov 17,

Japan projects to have a 1.8% annual GDP contraction, better than the previous forecast of a 2.5% contraction in Q3. The GDP decrease is primarily driven by U.S. tariffs impacting exports and sluggish global demand.

Tuesday, Nov 18,

U.S. Initial Jobless Claims for the Week Ending October 18, 2025 was reported at 232,000, marking the first labor market data release following the U.S. federal government shutdown. This figure remains above recent averages, reflecting lingering disruptions. The Federal Reserve's October 29 rate cut to 4.00% has sparked debate on its necessity, contributing to reduced market expectations for a December cut amid mixed economic signals.

Wednesday, Nov 19,

UK saw a 0.4% monthly increase in CPI reading in October, translating to a 3.6% annual growth, higher than the forecasted 3.5%. This elevated reading supports the Bank of England's decision to hold its policy rate at 4.00% in early November, maintaining a restrictive stance.

FOMC meeting minutes highlighted divisions among Fed officials on the timing and necessity of further rate cuts, introducing greater uncertainty into future policy decisions.

Why trade OTC?

Binance offers our clients various ways to access OTC trading, including chat communication channels and the Binance OTC platform (https://www.binance.com/en/otc) for manual price quotations and execution services.

Email: trading@binance.com for more information.

Join our Telegram Channel @BinanceOTCTrading (https://t.me/+0mkJQnbQiOdlZjk0) to stay up to date with the markets!

You can also reach out to us on Telegram (@Binance_OTC_Desk) to connect directly with our experienced traders for your OTC trading needs. We look forward to assisting you and providing exceptional service for all your OTC transactions.