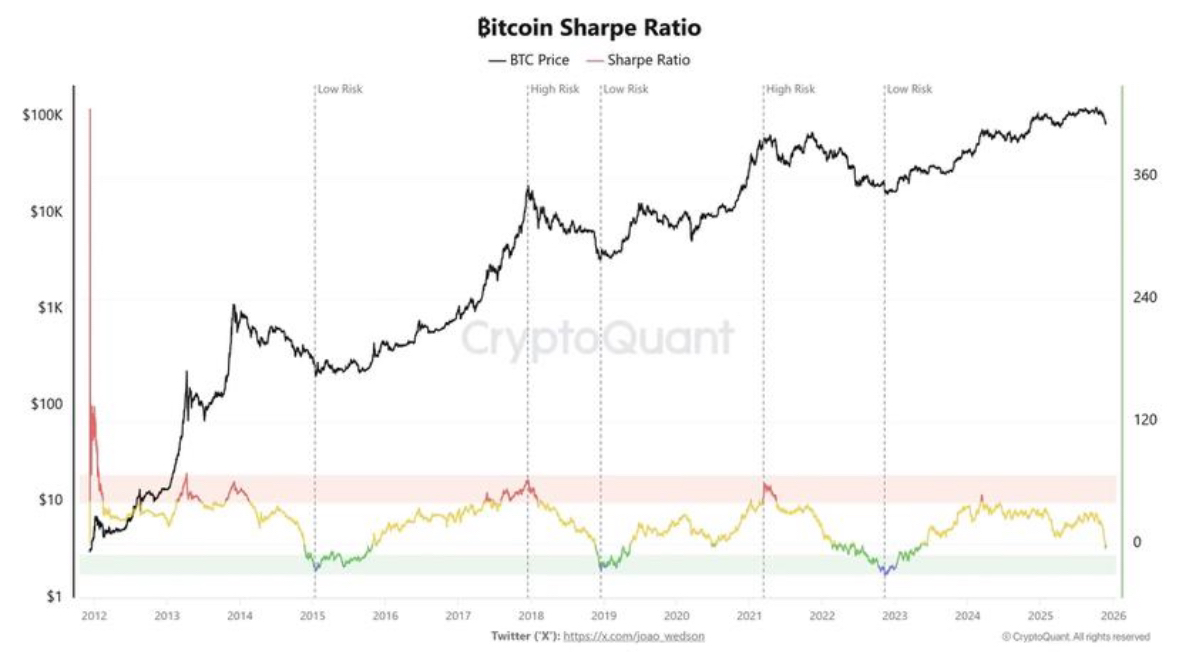

A key indicator—the Sharpe ratio—has quietly turned negative recently. From a traditional financial perspective, this indicates that the attractiveness of the asset has dropped to a freezing point. However, in the world of Bitcoin, historical data tells us that this often serves as a strong signal for the arrival of a medium to long-term bottom.

A key indicator—the Sharpe ratio—has quietly turned negative recently. From a traditional financial perspective, this indicates that the attractiveness of the asset has dropped to a freezing point. However, in the world of Bitcoin, historical data tells us that this often serves as a strong signal for the arrival of a medium to long-term bottom.

1. What is the Sharpe ratio? Why is it critical when it turns negative?

In simple terms, the Sharpe ratio measures the excess return you can achieve for each unit of risk you take. When it turns negative, it means that recently, the returns from holding Bitcoin cannot even compensate for its volatility risk, and market sentiment has dropped to a low point.

However, the market consensus is often wrong. When everyone believes an asset is 'not worth holding,' its price is usually at or near a long-term bottom.

Two, historical testimony: Violent reversals after three 'turn negative' events

1. 2019: The reversal at the end of the bear market

After the Sharpe ratio bottomed out, Bitcoin rose approximately 35% in the subsequent 6 months, quietly starting a reversal at the end of the bear market.

2. March 2020: The golden pit amid pandemic panic

The Sharpe ratio turned negative during the global asset panic sell-off, marking the most classic 'golden pit' in history. Bitcoin surged 130% in the following 6 months, boldly entering a magnificent bull market rally.

3. November 2022: Structural bottom after the FTX collapse

In the industry's own crisis (FTX explosion), the Sharpe ratio fell below 0 again. The market was in despair, but Bitcoin rebounded strongly by about 87% in the following 6 months, successfully establishing a solid structural bottom.

Three, core insight: Not the top, but the eve of the reversal

Based on these three historical patterns, we can draw a crucial conclusion:

The Sharpe ratio falling below 0 does not signify the continuation of a collapse in Bitcoin's cycle; rather, it frequently corresponds to the eve of medium- to long-term strong reversal trends ranging from 20% to 120%.

It is like a 'spring' of market sentiment; the lower it is compressed, the stronger the rebound potential. When the most pessimistic investors also choose to exit, the selling power is exhausted, and any bit of buying pressure is enough to significantly push prices up.

Conclusion:

For investors, when the Sharpe ratio turns negative, one should not be swept away by panic. On the contrary, this is precisely a moment to be extremely vigilant and consider phased positioning. History does not repeat itself simply, but it often resonates with similar rhymes.