Regarding the question of whether MicroStrategy will face a crisis, we have also had some discussions.

Personally, I believe the possibility of a crisis is low. The significance of the cryptocurrency market to the world lies in its being a high liquidity area with no regulation. This will inevitably attract those politically disadvantaged to allocate assets in cryptocurrency, especially in the context of UBS no longer being a safe haven.

If you don't understand, let me give you a plain example. Currently, the opposing party to the Republican Party, the Democratic Party, will allocate a considerable amount of cryptocurrency assets (mainly stablecoins and BTC), because cryptocurrency assets have extremely high property transferability and tax-exempt status, unaffected by regulatory agencies. Moreover, they will never easily cooperate with law enforcement agencies.

When the Republican Party steps down and the Democratic Party comes to power, funds in the crypto market can also quickly become compliant, and vice versa. The crypto market is no longer a small game, but a necessity in the great power game.

The above content points to one conclusion: the world needs the crypto market.

————————

So why would MicroStrategy's claim that it might sell coins cause tremendous market volatility?

I would like to use another example to illustrate.

In July 2024, the market fell into panic over Japan's interest rate hike, and BTC dropped more than 30% in a few days. Currently, BTC has also dropped by 30%.

————————

Why?

Before Japan's interest rate hikes, the market had no risk expectations for Carry Trade. Naturally, institutions would not have corresponding tail hedges for Carry Trade, as this is akin to a nearly risk-free arbitrage transaction.

When interest rate hikes affect Carry Trade, the large positions held by institutions have exposed single exposures, leading to the VIX soaring to a level just below 312 on that day.

This means that institutions are willing to spare no expense to hedge their positions in the market. Retail investors can hold positions, but institutions cannot leave their single exposures unprotected.

More similarly, there have been changes in the rating of U.S. Treasury bonds as risk-free collateral by regional banks previously. It seems like a gap of only tens of millions of dollars, but in reality, it poses a fundamental challenge to U.S. Treasuries.

————————

What does this have to do with MSTR's recent pivot?

Since its establishment, MSTR has always claimed that it would never sell BTC, but recently, with the decline of mNAV, this declaration has seen a shift.

In other words, for the market, there is a certain probability that MSTR would never sell coins.

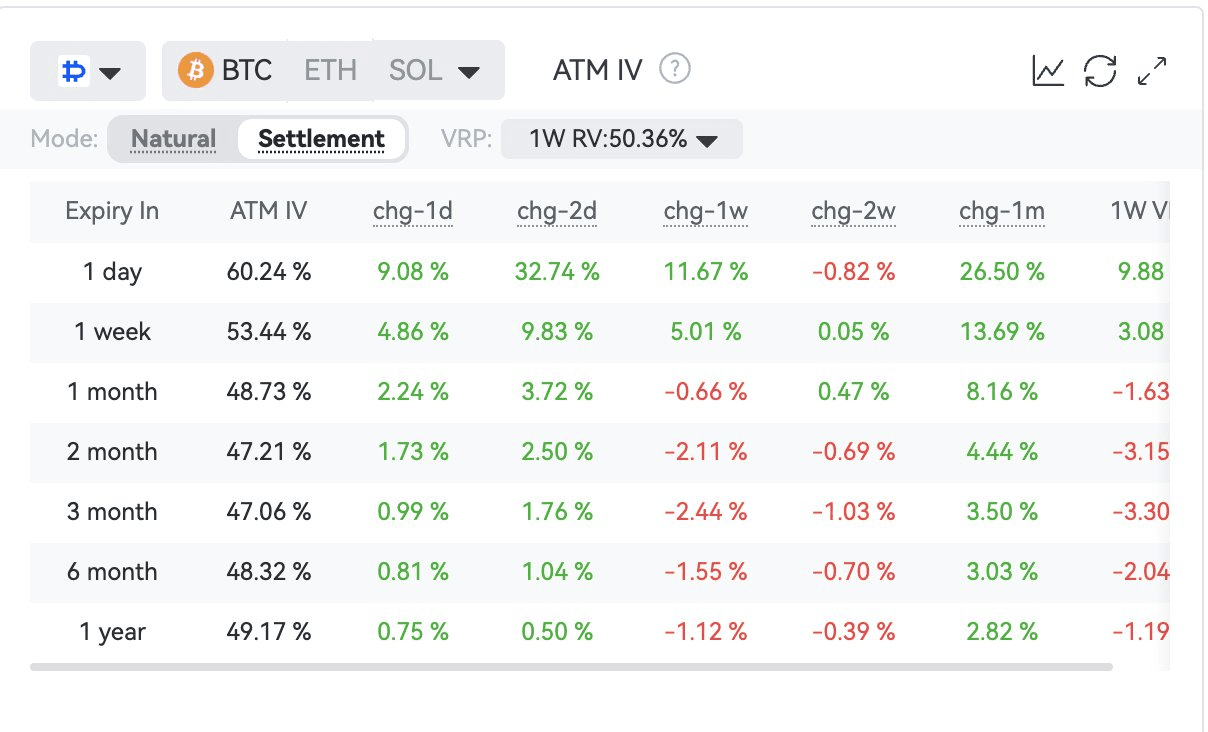

As currently the largest holder of BTC and a believer for many institutions, MSTR selling coins would lead to a chain reaction @Strategy, resulting in a large amount of tail hedging in the market, which manifests as recent IV rising, prompting a large number of BTC holders to hedge against tail risks in response to changes from MSTR.

In other words, MSTR's action of selling coins could be akin to changes in the Satoshi Nakamoto block, leading to market panic. We are currently in this stage.