Before dropping another post about liquidity aggregators, it's crucial to grasp why the problem they aim to tackle even exists.

Many people think a token's price should be uniform everywhere. In practice, that's not the case.

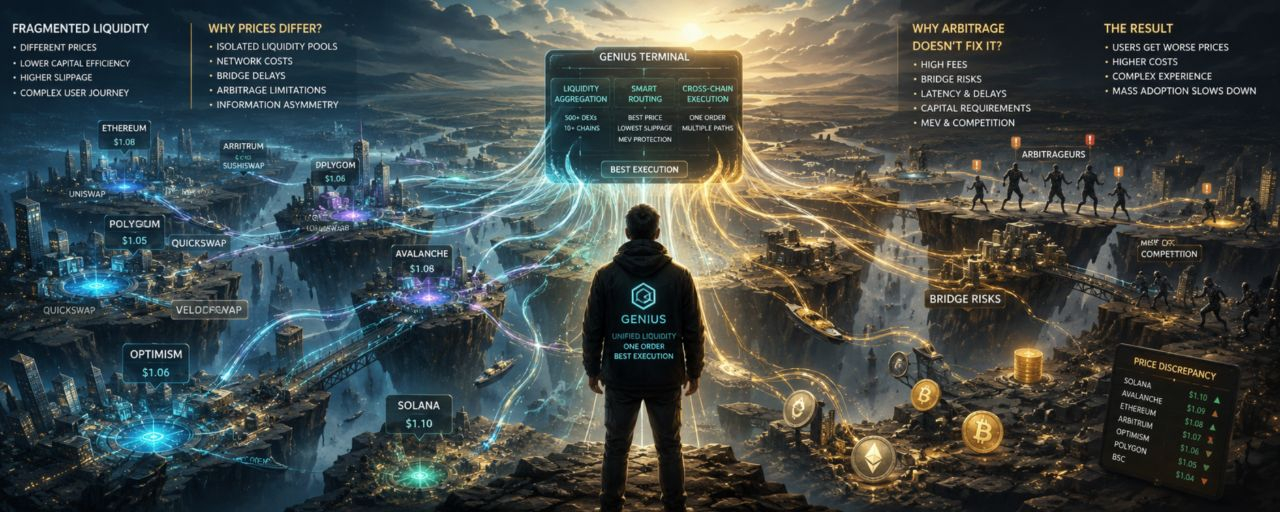

The same asset can trade at different prices across various DEXs simultaneously. The reason is that each exchange has its own liquidity pool. When someone buys or sells a token, the price shifts only within that specific pool, not across the entire ecosystem at once.

The situation gets complicated with the emergence of multiple blockchains. The liquidity of the same asset is spread across Ethereum, BNB Chain, Solana, and other networks. Each new blockchain creates another set of trading venues, pools, and swap routes.

Theoretically, arbitrageurs should be solving this issue. If a token is priced higher on one exchange and lower on another, they buy where it's cheaper and sell where it's more expensive. That's why many believe the market quickly levels out prices.

But in practice, arbitrage faces challenges such as fees, network delays, bridge limitations, execution risks, and competition from automated trading systems. By the time an arbitrage trade hops through several blockchains, the market situation may have already changed.

As a result, users often see only a small fragment of the overall market liquidity. The price on their chosen DEX might not be the best among all available options.

This is where the idea behind m-35 comes into play.

Instead of making the user hunt for platforms, compare prices, and build swap routes, the terminal tries to gather liquidity from various DEXs and networks into a single execution system.

Looking at the bigger picture, the issue with DeFi today isn't a lack of liquidity. There's already plenty of liquidity out there.

The problem is that it's scattered across hundreds of platforms and dozens of blockchains.

Much of the development of projects like c-24 is tied to the attempt to turn this fragmented market into a unified trading environment.