Recently, Openrouter released an AI research report (State of AI), which superficially reviews the AI market of 2025, but is actually more like a 'behavioral data record'. It does not discuss model architecture, but rather presents the real usage records of over 100 trillion tokens (fragments generated by AI models when processing language), laying bare how developers and users actually utilize AI in the real world.

AI User Behavior Shift: Reasoning, Tools, and Long Contexts Become the New Normal

In 2025, the AI world will experience a 'structural shift in user behavior'. Over the past two years, most people viewed large language models (LLMs) as enhanced search engines or writing tools; however, the (State of AI) research report written by OpenRouter, based on real usage data of over 100 trillion tokens, indicates that the positioning of LLMs is rapidly transforming from single-step generation tools to 'Agentic systems' capable of integrating tools, planning steps, and analyzing large contexts.

This transformation is not a one-off event but was triggered by OpenAI's launch of the 'o1 reasoning model' at the end of 2024. The report indicates that starting in 2025, the average prompt length submitted to LLMs by users increased from 1,500 tokens to over 6,000 tokens, no longer just short commands like 'help me write a piece of text', but more like a complete document, code repository, or multi-turn dialogue history. Expectations for the model have also shifted from 'give me an answer' to 'analyze this pile of information', 'plan a multi-stage action plan', and 'select appropriate tools and execute'.

Data from OpenRouter shows that in 2025, the token traffic of reasoning models will exceed half of the total, marking the official establishment of reasoning models as mainstream. In other words, AI is no longer just a content generator but is gradually becoming a process collaborator and decision assistant.

Open-source models are astonishingly fast, with Chinese models becoming an important force in the overall market.

It is worth noting that the driving force behind this wave of change is not only Western tech giants like OpenAI, Anthropic, or Google. The report reveals an underestimated fact through a wealth of data: open-source models (OSS) are rapidly catching up with closed models, especially the growth rate of Chinese open-source models is beyond expectations.

Statistics from OpenRouter indicate that by 2025, the total usage share of open-source models will approach one-third, with models from Chinese teams such as DeepSeek, Qwen, and Kimi occupying a very high proportion, with some months even approaching 30% of the overall traffic. This shows that Chinese models are no longer just targeting the Chinese language context but are attracting global developers through English optimization, cost strategies, and high update frequency.

These Chinese models are not just cheap alternatives. Data shows that they can now compete head-on with Western closed-source models in certain technical fields, including program generation, technical documentation, and data analysis. In particular, the DeepSeek R1 and Qwen Coder series, with their program generation capabilities, have led many developers to prefer their use in enterprise projects, personal projects, or automated workflows.

Rather than saying that open-source models are 'filling in', it is more akin to a movement for technological equity: high-quality AI no longer necessarily requires high costs, and the rapid iteration of Chinese models has redefined the global competition landscape.

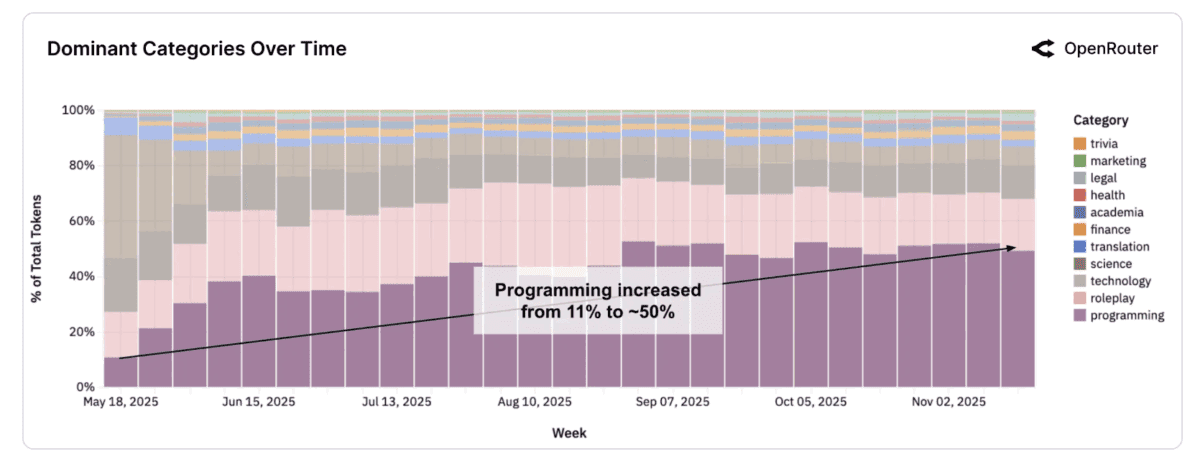

Roleplay and Programming: Two major pillar uses present stark contrasts.

If the model's capabilities and costs determine the supply side, then the true driving force behind market evolution is user demand. The (State of AI) report reveals a long-overlooked phenomenon: role-playing is the most substantial 'consumer' AI demand globally, while programming is the largest and most stable-growing 'productive' demand.

Research shows that in open-source models, over 50% of tokens are used in role-playing scenarios, including fictional character dialogues, novel character simulations, romantic scripts, and custom personality models. Open-source models have fewer content restrictions, can be fine-tuned by users, and maintain long-term character settings, allowing a large number of users to choose to build their own AI companion characters and narrative worlds on OSS, fulfilling users' 'psychological needs'.

At the same time, programming demand is expected to see explosive growth in 2025. AI has fully penetrated software engineering processes, heavily relying on models for debugging, generation, restructuring, and architectural planning. The report indicates that the overall traffic related to Programming on the platform increased from 11% at the beginning of the year to over 50% in Q4, becoming the fastest-growing category.

It is worth noting that different models present completely different positioning in the two major categories:

Claude and the GPT series continue to gain the trust of developers in the programming domain, becoming the backbone of enterprise-level workflows.

DeepSeek and other open-source models hold an overwhelming advantage in role-playing while providing cost-effective yet acceptable programming capabilities in personal development projects.

The usage scenarios of AI thus present a distinct dual-core pattern: on one side is entertainment, companionship, and interactive emotions, while on the other side are highly structured and specialized technical tasks.

The positioning division between open-source and closed-source: not replacement, but complementary coexistence.

The research report also points out that the market is not a one-sided competition but more like a dual-track parallel system. Open-source and closed-source models have formed a clear division of functional labor:

Open-source models emphasize scenarios of 'high volume, low cost, customizable', such as role-playing, creative writing, and lightweight programming development; closed-source models, on the other hand, dominate 'high risk, high value, high reliability' enterprise tasks, such as programming, data reasoning, and system architecture design.

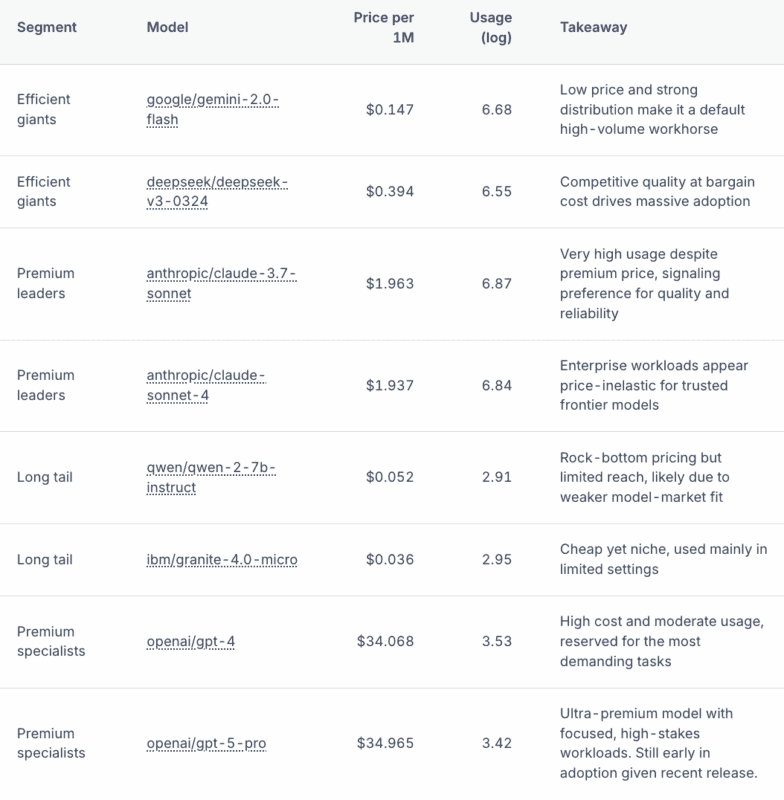

This division of labor also reflects the relationship between cost and usage. The report notes that the overall LLM market shows a 'price insensitive' phenomenon: even though high-priced models charge over $30 per million tokens, users are still willing to pay for their reliability and quality. In contrast, extremely low-cost open-source models may attract high volume traffic, but if their capabilities are insufficient, they still cannot impress enterprise-level applications.

Therefore, open-source and closed-source are not mutually exclusive competitors but different tools naturally chosen by users according to different task values.

Conclusion: AI is moving towards a three-track world of multiple models, multiple uses, and multiple cultures.

From OpenRouter's empirical research spanning hundreds of millions of tokens, it is evident that AI user behavior is not only changing but also reshaping the entire model ecosystem. Reasoning models enable AI to perform increasingly complex tasks; open-source models allow more users to access high-quality AI at lower costs; the two major demands of role-playing and programming support AI's 'entertainment' and 'production' worlds.

From a global market perspective, the rapid rise of Asian, especially Chinese, open-source models has made AI no longer just a single-center industry defined by American tech giants, but a multipolar ecosystem driven by different cultures, cost structures, and audiences.

After 2025, the AI world will no longer be dominated by a single model, but rather a 'multiaxis ecosystem' interwoven with open-source and closed-source, agents and models, entertainment and production. In such an environment, the behavior of each user may reshape the competitive landscape of models, and every breakthrough in models will also give rise to new usage habits and market positions.

The future of AI may not yet be determined, but as this report reveals, the real answers often lie not in the technology itself but in user behavior.

Source