The tokenization of assets (Stocks, funds, deposits, debt, gold, cocoa, real estate...), is so broad that projections for the coming years reach trillion-dollar figures.

Experts consulted value that tokenization is "a natural evolution" and more efficient in asset management, which is experiencing a key moment, the transition from pilot projects to large scale.

As of today, it already moves billions of euros. "It has ceased to be an experiment and now operates in Europe as a real operational model to represent and trade financial assets on blockchain."

The tokenization of assets is nothing more than transforming and representing a physical, financial, or intellectual asset in a digital file.

It allows, thanks to blockchain technology, to break down assets of both low and high value and distribute them among multiple participants.

The multiple possibilities offered by this conversion, such as fragmentation, traceability, flexibility, or efficiency, cause it to increasingly gain prominence in the financial field.

The future is digital, and the rise of tokenization emerges even as an evolution of money.

The greatest current potential lies in the tokenization of money, through stablecoins (EMTs under MiCA), tokenized deposits, and wholesale CBDCs, capable of enabling payments and settlements.

The financial sector has taken action. Tokenization has ceased to be an emerging trend to become one of the most relevant vectors of modernization in the financial industry.

This convergence between the traditional and the digital in the financial sector already points to a quiet revolution, in which tokenization represents a natural evolution in the asset management industry.

The market is accelerating and integrating into traditional wealth management models.

Currently, the market is moving from proof of concepts and pilot cases to large-scale implementations.

The process is consolidating in various fields. Currently, we observe significant liquidity and a greater institutional participation in multiple asset classes, from stocks and credit to real assets like commodities and funds.

The results of pilot projects provide an extra boost to its expansion. The Pilot Regime has demonstrated that this technology is safe, functional, and useful for issuers, investors, and supervisors. Hence, we will soon see how tokenization scales from specific pilots to truly liquid markets.

The projected growth is based on foundations that are already reaching billion-dollar figures. The asset tokenization platform of Boerse Stuttgart Group puts numbers to the present of tokenization.

As of today, there are approximately 20,000 million US dollars worth of tokenized assets in circulation, representing an exponential growth of over 800% in the last two years.

Although adoption is still nascent, there is already a sustained growth in institutional interest and the emergence of regulated vehicles managing billions in digital assets. This movement shows that the market is entering a phase of maturity, driven by higher levels of liquidity, division of ownership, and more operational efficiency.

2026 will be a turning point: the first complete licenses in Spain and Europe will open the door to a new generation of more efficient, more global, and more competitive markets.

The potential is so high, and the areas of growth so diverse, that one of the questions that emerges is where the limits of asset tokenization lie.

The main limitations are legal and regulatory (when there is no clear framework), interoperability with current systems, and the need for a real business case in efficiency and/or costs.

Tokenization offers unprecedented legal and operational efficiency, but it does not make all elements of our day tokenizable; its main limit is twofold: on one hand, it depends on the legal nature of the underlying asset. Not everything can be fragmented, transferred, or digitally represented with legal effects.

The applicable regulatory framework and traditional financial regulations clearly delineate which assets can be represented by tokens with full legal effects and under what requirements.

The ability to tokenize money forces financial entities to respond to its rise. More efficient infrastructures will be enabled for the execution of payments and settlements.

Major crypto players bet on this path to expand their growth.

An open infrastructure for tokenized shares is being built: an interoperable framework that will extend to other real-world assets over time.

The ability of tokenization to fractionalize assets extends its appeal to high-value assets beyond physical gold. Prices reach significantly higher figures in the real estate market. Hence the rise, and potential, of real estate tokenization.

Real estate tokenization is among the 'areas with the greatest growth potential,' as it 'will democratize access to traditionally illiquid assets.'

These assets have greater liquidity, as they can be traded on organized markets, facilitating the buying and selling of shares.

How does it work?

The process involves several key steps:

Identification and evaluation: An asset (e.g., a property, a work of art, shares) is selected and its value is assessed.

Legal structure: The legal and regulatory framework for the issuance and ownership of tokens is defined, ensuring they represent the same rights as the original asset.

Token creation: Using smart contracts on a blockchain, tokens are 'minted.' Each token contains information about ownership and associated rights.

Issuance and trading: Tokens are issued and can be bought, sold, or exchanged on platforms or secondary markets, often globally.

Examples of tokenized assets

Practically any asset of value can be tokenized:

Real estate: The ownership of a property can be divided into hundreds or thousands of tokens, allowing small investors to own a fraction of a building.

Works of art: Valuable paintings, which would otherwise be inaccessible, can be fractionalized, allowing co-ownership of high-value art.

Stocks and bonds: Traditional financial securities are represented on the blockchain for more efficient management.

Commodities: Gold, silver, or other raw materials can be represented by tokens backed by the physical asset.

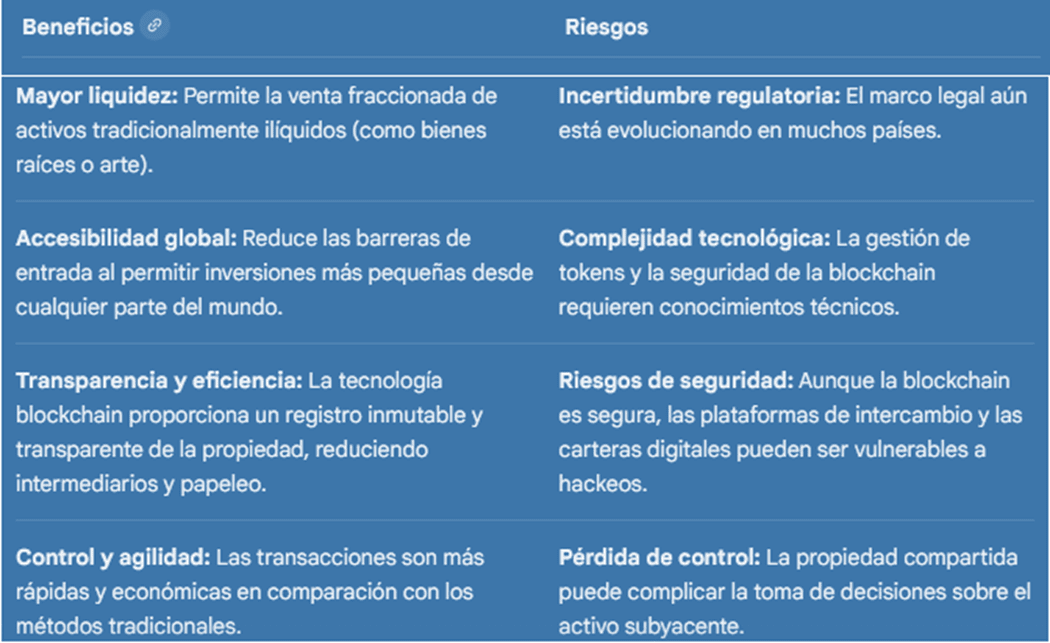

Benefits and risks

Tokenization is seen by financial leaders like BlackRock as a potential breakthrough to revolutionize the future of finance, bringing value and transformation to the sector.

In conclusion, the tokenization of assets is shaping up to be a fundamental pillar of the future financial system, with the potential to revolutionize the way ownership is accessed and managed.

The key points are:

Democratization and liquidity: Tokenization breaks down entry barriers by allowing fractional ownership of traditionally illiquid assets (such as real estate or works of art), opening markets to a broader base of investors and providing a level of liquidity that was previously inaccessible.

Efficiency and transparency: By leveraging blockchain technology, it eliminates intermediaries, reduces friction in transactions, and provides a transparent and immutable property record through smart contracts.

Potential growth: Although it is in an early stage, industry projections are optimistic, estimating that tokenized assets could reach significant value in the coming years, driven by private markets and institutional instruments.

Regulatory and technological challenges: Its mass adoption depends on the evolution of clear regulatory frameworks and addressing technological complexity and associated security risks, crucial issues for compliance and investor protection.

In summary, tokenization is not just a trend, but a transformative financial innovation that, as regulation and technology mature, will redefine the relationship between institutions, investors, and assets, making the financial system more agile, accessible, and personalized.